Decent performance! Good to see very good margins of above 20% (perhaps the highest in the industry). Hopefully the company should be re-starting the production from the expansion done earlier (which was affected by fire earlier this year)

9 Likes

That will reflect on Monday , anyway , short term price movements does not matter much. If one is convinced about the business , any fall will be welcomed. Those speculating on results may be worried.

Does not look so as Margins are really good. In fact best in last 8 Quarters.

As i said above , the profitability got hit due to higher depreciation and other expenses. When base is small , a little higher expenses and a little lower other income can affect profitability. For companies like these , i like to compare on 9M or yearly Basis.

For 9M Basis :

Sales have grown at 36% , Profit at 40%.

The business have ROCEs around 20+ % , No equity Dilutions and improving Cashflows.

6 Likes

is this paid service ? How one can get access to the reports ?

1 Like

Got following response from company on new capacity.

Dear Sir,

Greetings from NGL Fine-Chem Limited

With reference to the trail mail, commissioning is under process and we expect it to complete by end of this month.

6 Likes

Acquiring the stake of Macrotoch Polychem Private Limited

1 Like

Looks like unrelated acquisition, any idea why it was done ?

1 Like

Re Macrotech Polychem

Wouldn’t worry too much because it is a very small company.

Network eroded but now profitable. Fixed asset turnover looks strange.

NGL will be taking over ~Rs 4cr of debt.

Source: VCCEdge, numbers are in Rs million

5 Likes

Per ICRA, Macrotrch Polychem is in to the manufacturing of chemical intermediaries which are key inputs for NGL’s API manufacturing. It also mentions that the acquisition is too small to be materially significant ratings wise. Looks like a good investment.

6 Likes

Material Event

NGL Fine-Chem Limited (NGL) has signed a memorandum of understanding (MOU) with Mr. Nilesh Vipinchandra Mehta,

Mrs. Hetal Nilesh Mehta and Macrotech Polychem Private Limited (MPPL) to acquire a stake in MPPL subject to

completion of the due diligence as per the release on the BSE website dated March 25, 2019.

Impact of the Material Event

ICRA has taken note of the above event and NGL’s ratings remain unchanged at [ICRA]BBB+(Stable)/[ICRA]A2. In ICRA’s

opinion, the size of acquisition is not material enough compared to NGL’s scale and the company has adequate liquidity

in the form of cash and liquid investments to fund it through its internal accruals. Hence, the acquisition in MPPL is not

expected to have any significant impact on NGL’s credit metrics over the medium term.

The acquisition is likely to ease out the sourcing of chemical intermediates to some extent, which are the key inputs

required for manufacturing active pharmaceutical ingredients.

2 Likes

Hi,

I have gone through this thread. I have the following queries. If anyone has pointers that would be helpful.

-

Where do they chose a product from? Is there an inventory bank kind of sorts from which to chose from or there is a sales team identifying or is it always that they wait for a customer to approach them with a requirement?

-

What is the avg. time to market for a production once it is chosen?

-

For how long does a product generate revenue?

Regards,

Roberto el S

Disc: Interested, not invested

2 Likes

Board will consider for dividend too in the coming Meet ! It is after a long time they may declare dividends.

Disc: Invested

5 Likes

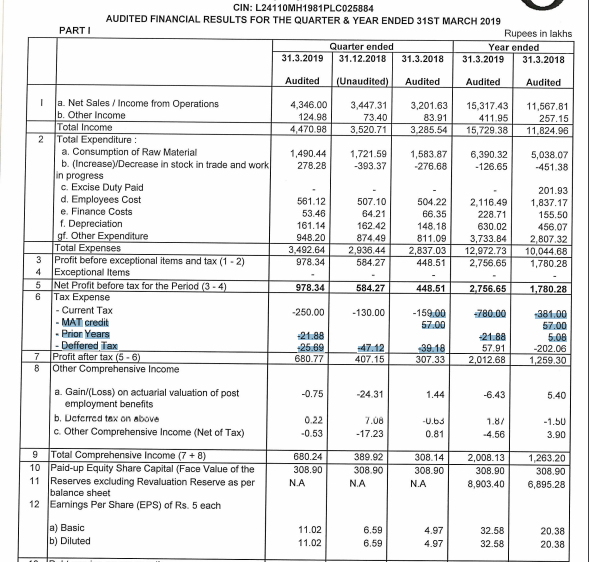

Results looks Outstanding !

33% Rise in Revenues Year on Year ended

60% Rise in Profits Year on Year ended

Dividend : 1.75 Per Equity Share

Retired some Long term Debts though similar increment in Current Borrowings.

Disc: Invested

12 Likes

Hiteshji,

Are you still tracking NGL finechem, there has been an uptick in March numbers. Valuation does not offer a high margin of safety

Any virw

Something I noticed while going through the Annual Report - both the Managing Director and CFO have together drawn Rs 2.6 crores in remuneration (salary + commission) from the company in FY18! That is just about 20% of the entire net profit. The pay out has also been steadily increasing.

The Company’s Act mandates anything above 10% requires special approval. While I’m sure they’ve got this, it is a little off-putting.

Will closely monitor FY19’s disclosures.

1 Like

Appreciate your concern on high salary. While it would be great that management take salary after considering total profits, but in my limited understanding, taking a very high salary is very tax inefficient way to take remuneration from the business. In many small companies, through web of companies as customer/supplier/ equipment provider/ contract manufacture; the management can easily take out money and we minority shareholder would not even get any clue about same.

While I completely agree with you on very high salary of management, what I like is direct way in which management is taking money from business (and also assuming no leakage from business from management side). Also the shareholder do have right on appointment and if we all feel that salary is very high, we can reject the resolution if we are invested.

Thanks for bring out critical point.

Discl: Hold tracking position for last 2 years. No trade in last 90 days. Not a SEBI registered advisor and not recommending company.

5 Likes

In addition to @yogansh’s notes from 2019 AR of NGL Fine.

Totally different AR this year from previous years, very detailed & informative. Company shared a lot of details like their segment breakup, products in different sectors.

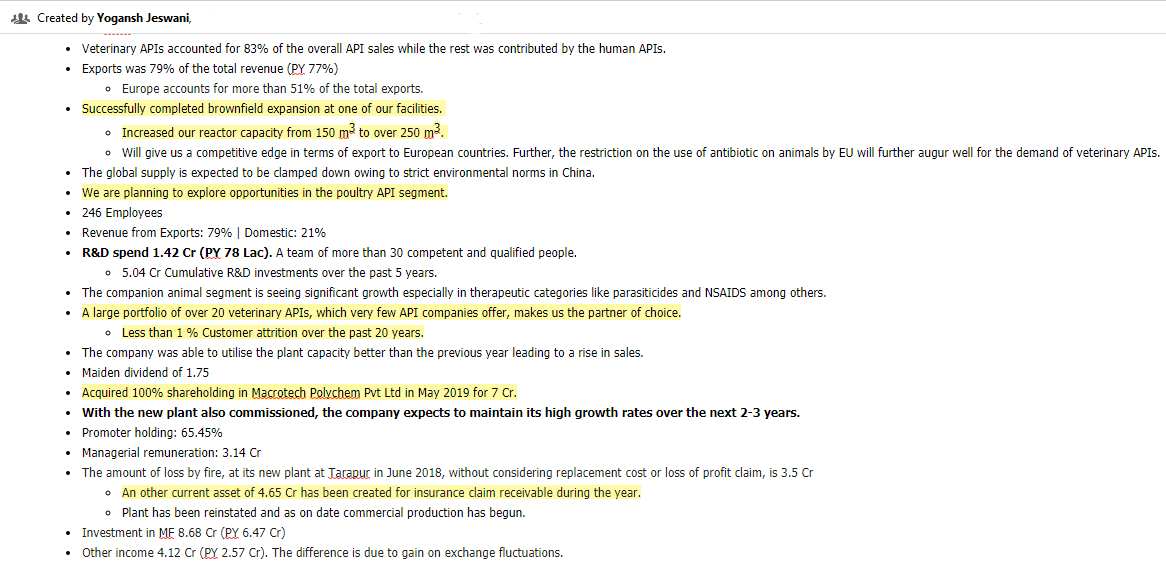

- The company was able to utilise the plant capacity better than the previous year at both the factory locations i.e. at Tarapur and Navi Mumbai, leading to a rise in sales. Costs were controlled better leading to a higher increase in profits.

- The company had a fire at its new plant at Tarapur in June 2018 information of the same was duly conveyed to the stock exchange. The reinstatement of the plant has been completed after taking all the necessary precautions and as on date and commercial production has begun.

- The company has acquired 100% equity shareholding in Macrotech Polychem Private Limited in May 2019 for an inclusive consideration of `700 Lakhs which includes the value of equity shares and loan given to Macrotech to repay its existing liabilities. Macrotech is engaged in manufacture of pharmaceutical intermediates. This will help the company to enlarge the range of its products and also to further backward integrate production of pharma intermediates.

- We have completed a brownͤ eld expansion, which will increase our reactor capacity from 150 m3 to over 250 m3 . This capacity increase will run on a DCS platform that will ensure greater processing controls.

- With the new plant also commissioned, the company expects to maintain its high growth rates over the next 2-3 years.

- Manufacturing facilities: 3

Commercial APIs: 20+

Finished Dosages: 20+

Clientele Base: 400+

Countries Present: 50+

Total Employees: 240 -

Product wise Revenues

Human APIs 2.6%

Veterinary APIs 83.20%

Intermediates 7.8%

Finished Dosages 5.3%

Others 1.1% - Company manufactures over 20 APIs in the veterinary division. These ingredients are used in different therapeutic categories such as ecto paraciticides, anthelmintics, growth nutrients, endo paraciticides among others. It contributes 83% of revenues in 2018-19.

- The Company also manufactures 4 APIs in for human health. These ingredients are used in anti-diarrheal, angina and anti-malarial. It contributes 2.6% of revenues in 2018-19.

- Our consistent collaborations with our customers has resulted in building long-lasting relationships with them. Across the globe, the Company has successfully retained more than 99% of its clients through high quality standards and cost competitiveness.

- Exports comprised 79% of the total revenue as against 77% in the previous year. Europe accounts for more than 51% of the total exports.

Total Foreign Exchange Earned11940.08 Lakhs Total Foreign Exchange Used1249.53 Lakhs - Research and Development cost has increased to

1.42 Crores in 2018-19 from0.79 Crores in 2017-18, at 0.93% of revenues. 30 people stregnth in R&D. - During the year we further made inroads in the non regulated market. We have successfully completed brownͤ eld expansion at one of our facilities. This will offer us a competitive edge in terms of export to European countries.

- The restriction on the use of antibiotic on animals by EU will further augur well for the demand of veterinary APIs. The global supply is expected to be clamped down owing to strict environmental norms in China. This is likely to give a flip to the home-grown manufacturers like us to encash upon the opportunities.

- We are also planning to explore opportunities in the poultry API segment as a part of our market expansion strategy.

- We supply APIs to over 400 customers across 51 countries. The trust we have built that we will always put quality first has helped us achieve a high level of stickiness with our customers. Also having a large portfolio of over 20 veterinary APIs, which very few API companies offer, makes us the partner of choice.

-

Animal Health Market Size

The global Animal Health pharmaceutical market was valued at about US$ 30 billion in 2016 and is expected to grow over US$ 45 billion in 2025 at 5% CAGR. Out of this, 60% accounts for livestock animals and 40% goes in for the companion animal segment (Source: Annual Report of Dechra last year). The global API market for Animal Health is poised to grow to US$ 9 billion by 2025 from US$ 5.3 billion in 2017, at 7.3% CAGR.

Regards

Harshit Goel

11 Likes