Was going through the annual reports.there has been a significant increase in renumeration.Can any of the senior members throw some light on how much is too much.I mean when does an investor need to be alarmed Not invested

Not invested

@reggy

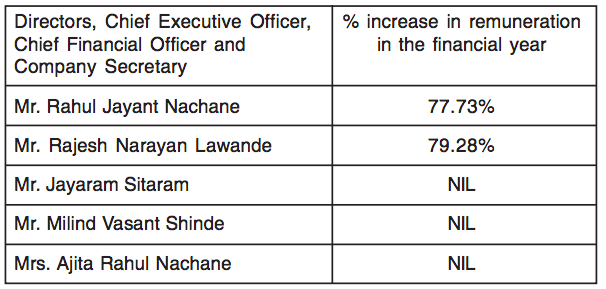

Gross salary remains same for the promoters since last 3 years. But last year they proposed 2.5% of profits to be added as bonus for KMPs from FY17 …so subtract 84 lakhs and remaining is bonus …reason for 70% hike

1 Like

@paresh.sarjani1 thanks for clearing that.I ll be more thorough when going through annual reports next time

Hi All,

I attended the 2017-18 AGM today. Please find my takeaways, would request members who attended the meeting to add or make corrections if required.

- The co. is operating at 115% capacity. The factories are running non-stop, just making do with basic maintenance. The orders taken up for new capacity which got affected by fire are being fulfilled by the current capacities. Current quarterly run rate is expected to continue for ongoing financial year and 130-135 cr revenues look achievable. The co. is actually starved of capacity and can’t meet demand. Operations at 115% are not sustainable for long and the levels will come down in due time as and when new capacities can be commercialised. New capacities were ready for trial runs around Sept-Oct 2017 and after completion of all the required trials and tests commercialisation was to start in June after final approvals. The incident of fire has pushed back the co. by 6-9 months and commercialisation of new capacities will only start in next financial year if not earlier. The total loss is estimated to be around 5-6 crs. An insurance claim will be lodged for the same in due time. The new capacities will manufacture existing and new products both. New capacities will contribute around 75 cr in revenues at peak considering 2.5x churn.

The co. plans to expand capacity further after 50% utilisation levels are achieved for the recently added capacity. The investment required will be 50 cr and this capacity should be ready by the time all the capacity ( old+new) reaches full utilisation, expectedly in 3 year’s time.

-

Consistent margins in the range of 20% over a period of time is a result of continuous improvement in processes and backward integration. Margins over a period of time will trend in 20% ± 4% depending on currency and raw material situation. June quarter margins have been aided a bit by forex gain. Pertaining to fy19, margins will remain under pressure because new capacity added is as good as ready and incurring expenses which are being reflected in the P&L.

-

The top 3 products contribute roughly 50% of the sales. The co. has 60-80% market share in these product markets and the same is expected to grow by 10-12%

-

The co. will introduce 4 new products once the new capacities commercialise, 2 in category of mammals and 2 in category of Poultry. The co. is entering the Poultry market for first time. Poultry market is bigger in size as compared to mammals. The co. is in an advantageous position as existing customers also cater to Poultry segment and have been demanding products from NGL for the same. Domestic market for Poultry is also big and co. hopes of achieving 1/3rd of the sales from the same.

The co. will keep introducing 2-3 products every year. Half of the R&D team is focused on product development and half on process improvement.

-

The customers demand NGL’s products as its lowest in cost, high in quality and service is reliable.

-

Demand scenario is favourable as unregulated markets hold scope for penetration.

-

The co. has plans in back of its minds to foray in regulated markets in distant future through a dedicated plant. Currently, it’s just getting it’s feet wet trying to make sense of it.

-

The co. is not exposed to emerging market currency risks as 99% of sales are dollar denominated.

-

The management mentioned that it’s plants are one of the best catering to unregulated markets. The standard of operations is also notches above competition given focus on processes, the result of which is above normal margin profile even after maintaing cost competitiveness.

Disclosure : Tracking.

P.S. - I’ve tried my best to present a fair picture but there could be some lapse in my understanding and members should be careful about the same.

25 Likes

NGL Fine Chem Ltd 2018 AGM- 24/08/18

I attended the AGM and Compiled mostly from Q&A done by several shareholders. There might be errors on my end in listening so please confirm the data.

New Tarapur plant & other capex

- New plant capex was 30cr. Plant was ready by Sept’17, takes 6 month for trial batches and quality verification. In April, capacity was ready for commercial production and was waiting for authority consent to start commercial production. It will take 3 years for plant to ramp up and reach full utilizations

- Fire completely damaged electrical cables and electricity room of this plant (covered by insurance completely) and it would go online for commercial production from 1 or 2nd Q next FY.

- Currently, working 7 days a week (115% utilization) to fulfill the supply hamper from newer facility. This is not sustainable for long term, can do this only for 6 months or so as plants are usually off a day for maintenance. Did debottlenecking so existing capacities also improved

- Got EC approval for another Tarapur plant- yet another new greenfield plant. Will start building this capacity once the new capacity reaches 40-45% so that by the time co reaches full utilizations, newer capacity will be online. This will take 3-4 years

- Over next 5 year period expect 50cr new capex and 50cr maintenance capex

- Around 70cr sales would be done from new plant. Usually consider 2x capex cost as annual revenue addition from that capex

- Allotment of a land plot on Ambernath MIDC either end of this year or next year

Products Related

-

Currently doing 21 products, 8-10 products in which co is very strong. The top 3 products of the company adiminazene aceturate, buparvaquone and sulphonamides or nitroxynil (thanks @ankitgupta for names)

-

OPM over the years have been fluctuating because of commodity prices, exchange rates, level of competition & life cycle of products

-

Chinese players tie up with RM players (usually also located in china) and they sell RM to API players like NGL at much higher price at which its unviable to develop APIs. Hence, despite the China shut down thing, they’re still competitive enough with us.

-

Not involved in drug discovery, patent products. All products are off-patent, non-innovative drugs. All generic. Their advantage is lowest cost which they are able to provide due to refining the process. They keep on trying to reduce costs even in current products

-

Peers are Sequent, Lasa supergenerics, rakshit drugs, RA chem. But only sequent is focused higher on veterinary, though it caters regulated markets

-

Threat of competition will always be there but lower because of low volume high value products they choose

-

If competition in a product increases, margins need to be lowered a bit depending on the life cycle of that product. If co remain firm on margins, competitor may undercut and client may prefer lower cost supplier

-

Current years plans to develop 2 poultry and 2 veterinary (mammals)

-

R&D- 3 PhDs and 3 MSc. Currently 30 people in R&D from 22 last year. They find newer products and improves process to make older products more cost effective

-

Only 7-8% of key starting material is outsourced, rest is all captive

Financial Related

- On longer term expect operating margins to be 20% +/- 4%. Prefers to not give future sales estimations as its really tough. This FY will do 130cr at least

- Current Q was good because of US $ appreciation. In last 2 Q, from US $ appreciation, kept 70 % margins with our self and passed on 30%

- Top 3 products account for 50% of revenue. Co is largest manufacturer for all these 3 products. Co has 60%+ market share in 2 of this products and 80%+ in 1 product. All these are from unregulated. Top 5 customers’ accounts for 25% of revenue

- Entire business is done in USD. Even business with Europe is done in USD. Hedges 50% of the order value on due date and 50% is uncovered. 20% of sales is done on 6 months contracts, rest all is on spot basis. Usually, able to pass on rise in RM prices most of the time

- Future tax rate around 25%

- 40% sales to Europe and remaining to ROW. Africa only contributes 2%

- PCI fermone chemicals pvt Ltd is co’s founding promoter’s friend. Its holding 8% stake

- This Q margins are lower because every cost related to new plant- incremental labor, testing, trial costs etc is being expensed. Nothing is capitalized

Segment wise

- Veterinary is currently 90% sales and co is also focusing on Poultry which has wider product base. Poultry segment is growing at double digit since 10 years, much bigger market than veterinary.

- In Poultry segment, no Indian firm is currently operating in the products they are developing. Sequent is trying the same but no robust products yet

- Co is currently very competitive on unregulated market. Can’t serve regulated and unregulated from same facilities as higher costs are associated in regulated markets which makes co inefficient in unregulated markets

- India barely produces 5% veterinary API, majorly is done by china still

- Testing market for human APIs until gets something concrete to foray into

- No guidelines for poultry but may constitute good proportion of future revenues. Need to make 4-6 products to make significant revenue from it

36 Likes

Some of the points which I also noted from NGL AGM are given below (some of them may be repetitive):

-

Product selection criteria: We select niche products where the market size of the molecule is less and because of that the bigger players do not enter the market. Furthermore, sometimes our existing customers approaches us manufacture a certain molecule. We also select molecules where we have edge in certain chemistry/reactions. We are present in molecules which are solely used for veterinary APIs (60 – 70% of the veterinary APIs overlap with human APIs). We are not looking for large molecules with market size of Rs.200 crore. We are more focussed on high value, low volume products. For large players, the smaller sized molecules are not attractive.

-

Healthy gross margins and profitability: For many of our products, we are backward integrated upto N – 8 stage. Higher the number of reactions, more the complexity and hence higher the profitability. We also have strength in some of the reactions. In addition, we have taken various initiatives including reducing water, wastage and even liquid discharge to improve our profitability. Over the long term we should be able to maintain 20 +/- 4% PBILDT margins. The profitability margins depend on commodity prices especially crude. However, we are able to largely pass on the increase in raw material prices to our customers. Over the past one year, prices of lot of raw materials and intermediates have increased by 50 – 100% and these have been fully passed onto our customers. Furthermore, one point should be noted that for the new plant, we are incurring fixed costs as well as depreciation and interest while revenue from it is yet to start.

-

Entry to regulated markets and human APIs: Our focus remains on un-regulated markets and there is still room to grow here. The growth rates in these markets are also higher compared to regulated markets. We are building blocks to enter into regulated markets but in a gradual manner. In EU we have registered 2 APIs in 18 countries. However, the molecules are small in size and have been filed in such a way that the same will not trigger inspection by regulatory authorities. However, for full-fledged entry into regulated markets, we will have to keep the plants separate for regulated and non-regulated markets. Human API market is 8 to 10 times larger than veterinary APIs. We are also looking to grow there. We are working on API – Ranolazine (Ranexa by Gillead) and can be a good opportunity for us.

-

Product pipeline & R&D: The company had plans to introduce 4 new products including two for poultry from the new plant but the same has been postponed to next year post commencement of operations of new plant. Poultry API is a bigger market than mammal API markets we serve. Top 3 products constitute 50% of our sales. In these molecules we have 60 – 80% market share in the unregulated market. These molecules are pretty old and growing at a steady rate of 8 – 10%. We plan to introduce 3 – 4 new products every year. Our R&D team consists of 30 employees including 3 PhDs and 11 MSc. One of the PhD scientist has experience of drug discovery while the other one has done PhD from abroad. We pay them pretty well. 50% of time of the R&D team goes for optimising the reactions for current molecules being manufactured by the company while the remaining goes on working for new molecules.

-

High employee cost and repairs cost of plant: Even after excluding the salaries paid to the promoters, the employee cost is high as we pay well to our employees. There is a lot of corrosion which happens in an API plant and since we have regular inspection from our clients, we have to keep our plant in good shape requiring regular repairs.

-

Fire at the new plant: The fire at the new plant occurred due to short circuit. Our new plant is state of the art and because of the sprinkling machines installed at the plant, the fire was restricted to only electrical room. The total loss due to the fire is Rs.5 – 6 crore. We will recover the claim later on reinstatement basis as the historical costs for the plant will be less. The plant should be ready by February, 2019. Now we are taking even more precaution and installing fire resistant cables. Post full ramp up of the new plant we can generate Rs.70 – 75 crore turnover from it (asset turnover of 2 – 2.5 times). We will take 2 years to achieve that.

-

Impact of China on our business: There hasn’t been any impact of China issue on our operations and Chinese continue to be as competitive as they were earlier. The prices of intermediates and other raw materials have increased and we have been able to pass on the prices to our customers.

-

Future capex plans: We will be spending Rs.100 crore capex over the next 5 years out of which Rs.60 – 70 crore will be for new plant and remaining will be maintenance capex. For the Greenfield Tarapur project, we have received EC approval. We have started constructing some portion of the plant but our current focus will be to reduce debt and ramp up the brown field plant once it commences operations from February, 2019. We have also in discussion for allotment for a new land at Ambernath from MIDC which is expected to be receive in new few months.

-

Performance during Q1FY19: The entire growth in revenue during Q1FY19 is on account of the old plant which is now being run at capacity utilisation of 115%. We are now working on 7 days a week instead of 5 days earlier. We are also using diesel generators during power cut. The current run rate for Q1 is sustainable. Post commencement of the new plant we can ramp up to revenue of more than Rs.200 crore over the next three years (from commencement of new plant). The PBILDT margins have declined due to fixed costs of new plant.

32 Likes

I am new to NGL Fine Chem and i just started below are somethings which i want to understand.

Below is my notes from AR2018.

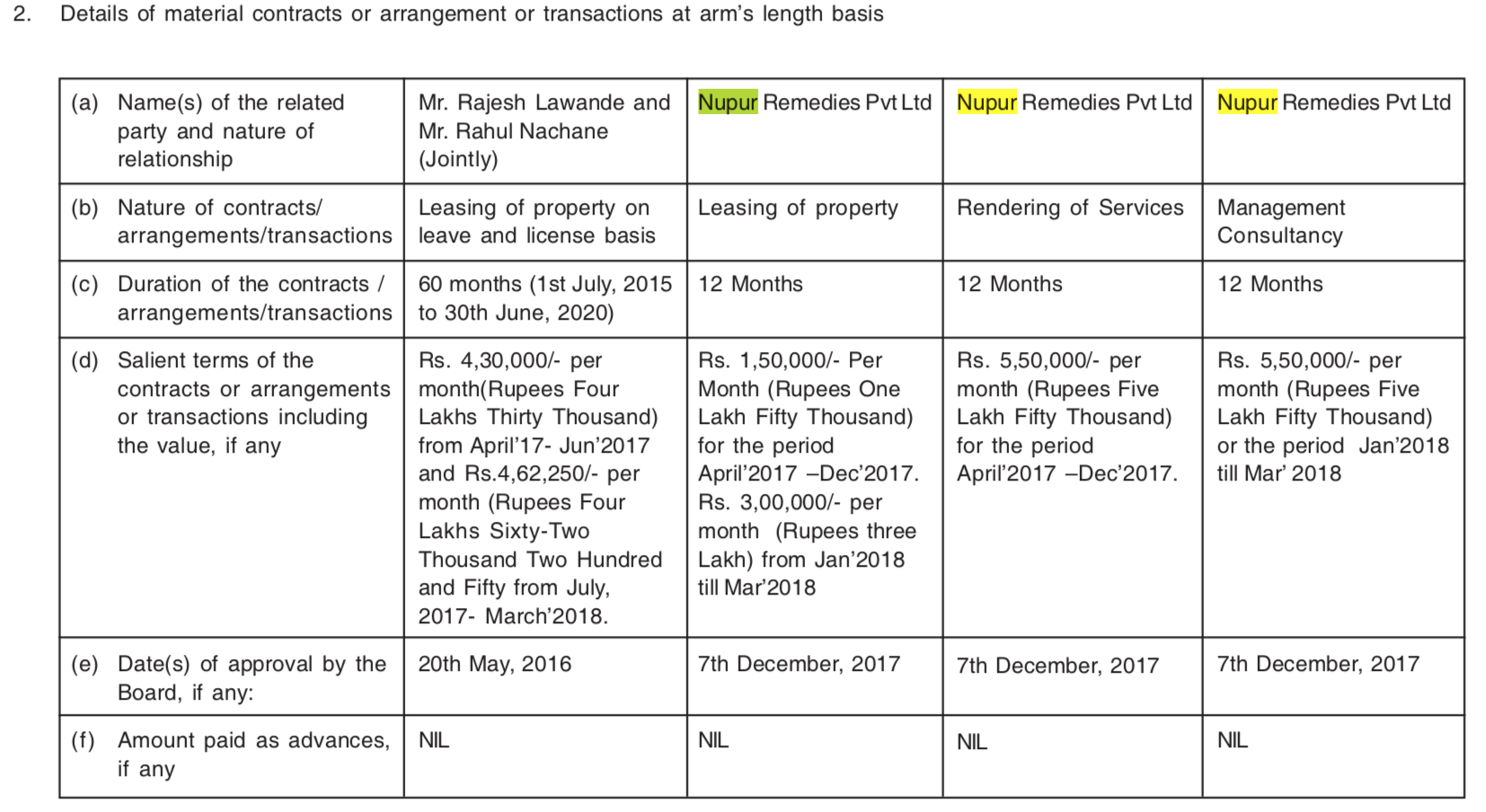

Promoters take 2.6 Crores in remuneration(Related Party Transactions Page 60) and profit after taxes is 12.59 Crores(Page 33) which is almost 20% of profits?

Nupur Remedies (a promoter company) draws 1.3 Crore on rent, Legal & Professional fees and Laboratory Contracts and others.

Below is from page 12:

If any company writes lease/services/Management of Consulting they are generally written on a 2+2, 3+3 or 5 year contracts, why do they write contracts for 9 months?

Other Minor things however they are smaller by number:

Page 46:

Depreciation Accounting/Asset Purchases …

There is a depreciation on free hold land?

Even though there is depreciation I think … it a little aggressive.

Page 58:

Repairs to Buildings and Plant it is almost 40 lakhs this year and last year. However if you cross check with page 46 Property, Plants and Equipment. They don’t match with additions why?

May be i am looking at things wrongly… let me know your thoughts.

6 Likes

Some of these things have been a concern. Yet, I would say that high salary has been a common thing in several small and mid-sized companies and I tend to ignore if the company has been doing well. In the case of NGL, its appreciable that they have delivered highest margins in the industry despite high expenses like above.

Regarding transactions with Nupur - as per response at AGM, Nupur operates the R&D centre and hence the payout. Its a big enough facility with about 20-25 R&D people (if i remember right).

Yes, the amounts have increased and it would be better if these things are not there.

Maybe one can write to the company - they usually respond to queries.

Regards,

Ayush

10 Likes

As per clause of Companies Act, cos have to take some govt approval and shareholder approval for higher salary and it was there in notice to AGM of 2018.

3 Likes

FY19 Q2 Results:

1 Like

The company is certainly throwing out great numbers in terms of growth. And the management is certainly very clear what they want to do in-terms of strategy as per my interactions in the AGM. The TTM EPS is ~ 28 and if we annualize the H1 19 EPS, FY19 EPS could be around INR 30/share. However as I analyzed the numbers closely, these are certainly buoyed by the other income, presumably from forex gains owing to currency depreciation.

In FY17 the company earned OI of ~ 2 Crores. In FY18 this was 4 Crores and in the first 2 quarters of FY19 it has already reached 4 Crores. In TTM it is 7 Crores. If we strip this out from the PBT and apply a 25% tax rate then the EPS falls to INR 19/share. I believe this number is closer to the Core earnings of the company. Over the last 7 years the OI contributes ~ 1% to sales.

If we take that to be a more sustainable number then the EPS would be around INR 20/21. If one takes a look at TTM multiples otherwise it is at 18x and if one looks at core PAT basis, the current multiples based on that would be 25x!

Still find it expensive.

Discl: Not invested

6 Likes

@rohitbalakrish_

I believe currently company is not being valued at TTM basis… It’s valued rich due to future prospects and good corporate governance.

Their completed capex is not showing fully at this point

Their margins have contracted due to crude rise

Their plant had a fire incident in between

And still you see these good numbers.

I believe next 18 months numbers will be significantly more than what it’s currently delivering and that’s the reason of valuation.

Again my message is qualitative and not supported with numbers but this comes from my experience of tracking this company

11 Likes

Not sure you have considered the one offs of other expenses in your calculations.

I feel company is on it’s way to deliver good growth numbers for next 4-5 years with current capex and the future one where the work is yet to start.

Regards,

Raj

Disc: Invested

2 Likes

Hi Raj,

I didn’t. It should be added to the EBITDA. Thanks for pointing out. I agree that the company is posting good numbers on growth and I was certainly impressed by the management. My point is more around entry valuations especially in a business where the predictability on margins is not very high and lot of unknown factors can impact the margins.

2 Likes

I agree that the valuations are a bit rich (relatively now…given the fall in mid caps). But i like the consistent performance of the company and very robust (and perhaps industry highest) margins since sometime now. Its good to see that the company has been able to deliver on growth despite the new plant not contributing yet. I hope they get the approval soon enough and get benefited from the expansion done earlier.

8 Likes

NGL Fine rating upgraded by ICRA.

Key points.

- The ratings consider its established customer base with low customer concentration risk. NGL’s customer base is diversified with the top five customers accounting for 35% of the total sales in FY2018 and 31% in H1 FY2019 (39% in FY2017).

- NGL’s operating income (OI) witnessed a 14% growth in FY2018 and stood at Rs. 113.66 crore against Rs. 99.72 crore in FY2017, on the back of a 4% growth in sales volume and an 11% growth in average sales realisations.

- The company’s inventory levels generally remain on a higher side (76 days as on March 31, 2018), owing to a sizeable WIP inventory (given that the production cycle varies from a few days for basic products up to eight weeks).

- NGL primarily manufactures various veterinary pharmaceutical products, primarily APIs which account for approximately 80-90% of the company’s total annual sales, while the rest are derived from intermediates and formulations.

- Despite having more than 30 APIs/intermediates/formulations in the product portfolio, NGL’s revenues have remained concentrated among three products (namely Diminazene, Clorsulon and Buparavaquone) which accounted for ~45% of the total sales in FY2018 and 44% in H1 FY2019.

Regards

Harshit

6 Likes

Did you receive any response from Company CS?

1 Like

Not yet , was not expecting either due to the type of questions !

Good Set of Results

Revenue 34.4 Cr vs 29.2 Cr (Q3 2019 vs Q3 2018) ,

Profit : 4.07 Cr vs 4.19 Cr (Q3 2019 vs Q3 2018)

Profitability hit on account of higher depreciation cost and other expenses.

.

9M Period

Revenue : 108.25 Cr vs 79.4 Cr ,

Profit : 13.3 Cr vs 9.5 Cr

9M EPS around 21.5 , May end the year with EPS around 28-29 !

At P/E of 15-18 , looks fairly valued with good possible upsides !

https://www.bseindia.com/xml-data/corpfiling/AttachLive/97a93774-04a0-487f-adb0-0c545df40244.pdf

5 Likes

@bharat19 sorry to say but I personally think street was expecting numbers better than this…

Not sure why YoY profits are still under pressure. Is it crude?

Any idea whether they are still working at 115% utilization or the QOQ revenue is down in this quarter as they started taking a day off for maintenance?