Update on recent fire incident on newly expanded capacities

On June 27, 2018, NGL Fine Chem Limited (NGL) announced that there was fire accident at the company’s plant located at F-11, Tarapur and that the assessment of damage is under process. At the aforesaid plant, NGL was carrying out expansion of their production capacity and was undertaking trial production when accident happened. However, the company has adequate insurance cover for losses caused by damage fixed assets and loss of profit. CRISIL believes the incident will not have a major impact on the company’s business and financial risk profiles.

Healthy financial risk profile

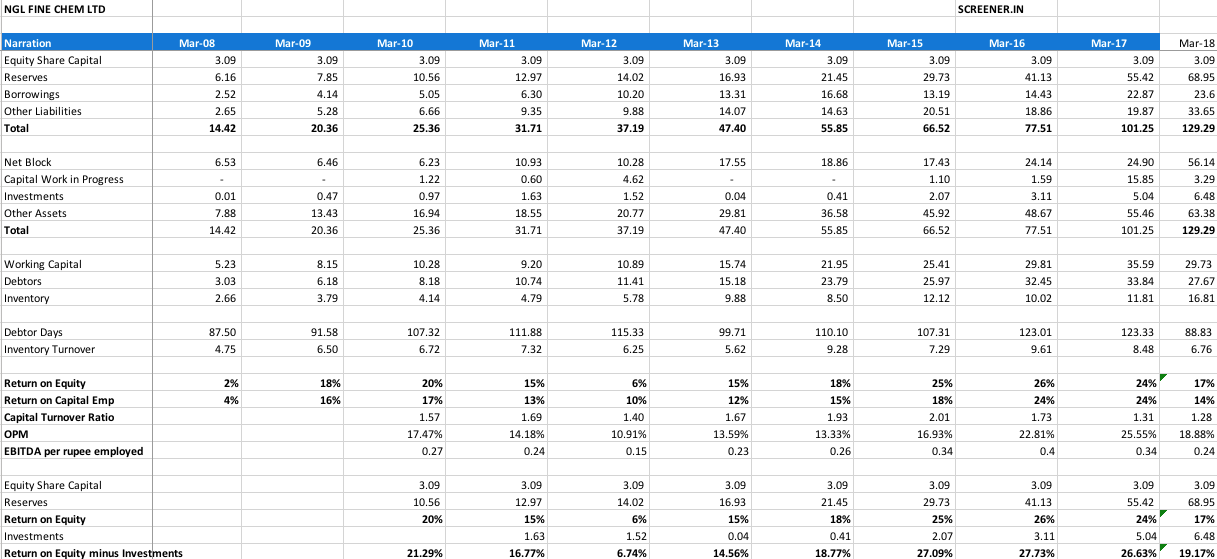

The financial risk profile is supported by comfortable networth and gearing of Rs 58.3 crore and 0.39 time, respectively, as on March 31, 2017. Debt protection metrics are strong due to healthy profitability and controlled reliance on debt.

Experience of the promoters in the pharmaceuticals industry

NFC manufactures bulk drugs and intermediates for human and veterinary diseases. It primarily manufactures active pharmaceutical ingredient (APIs) under the antiprotozoal therapeutic category. The promoters, Mr Rahul Nachane and Mr Rajesh Lawande, have experience of over a decade in the pharmaceuticals industry. Their expertise and experience have helped NFC establish its presence in the highly fragmented bulk drugs industry and establish relationships with clients, which will support the company’s business risk profile over the medium term.

Weakness

Modest scale and working capital-intensive operations

NFC’s scale of operations is modest, compared with that of established players in the domestic pharmaceuticals industry. Also, operations are moderately working capital intensive. The company extends credit of 90-120 days to its clients. It has to maintain raw material inventory of 30-60 days to cater to urgent demand and remain competitive. Ability to scale up operations in the coming quarters, improvement in the margins and management of its working capital cycle will be a key determinant of its credit risk profile over the medium term.

Outlook: Stable

CRISIL believes NFC will continue to benefit from its promoters’ industry experience and established customer relationships. The outlook may be revised to ‘Positive’ if revenue and profitability improve on a sustained basis while financial risk profile remains healthy. The outlook may be revised to ‘Negative’ if the business performance weakens considerably, and if capital structure and key debt protection metrics are hit by larger-than-expected, debt-funded capital expenditure or acquisition, or if working capital cycle lengthens.

About the Company

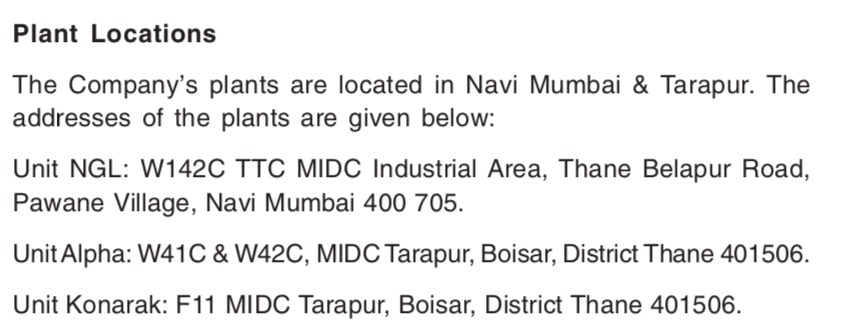

Incorporated in 1981, NFC is managed by Mr Rahul Nachane and Mr Rajesh Lawande. The company manufactures human and veterinary bulk drugs, intermediates, and formulations. It primarily deals in animal healthcare products such as antiprotozoal, anthelmintics, and growth promoters. Its administrative office is in Mumbai and manufacturing facilities are in Tarapur and Navi Mumbai in Maharashtra.

Hello Everyone, I recently started tracking NGL FineChem but unable to connect dots here…

Management First announced Capex in 2016 AR where it mentions that statutory consents have been received

But I found this EIA Recently dated May’17 wherein It is seeking permission for similar size of the project but its a greenfield project as per EIA, Whereas management earlier informed that the project is existing tarapur plant http://www.environmentclearance.nic.in/writereaddata/FormB/EC/EIA_EMP/17052017EMT7ICMKEIA.pdf

How is this possible? Is this EIA for a newer project apart from the one which completed last?

Also, Got one more link wherein company has some hearing related to State Expert Appraisal Committee conducted on 27/02/18… Any information what is it about? If plant is already built, why such hearing or else is it for a newer plant ? 7EB8585A6BEB4EB7993D1A156D3EB8D9.pdf (152.0 KB) (check Sr.no 9)

This are the plants company mentioned in AR17, it does not include plot of land mentioned in EIA

Hi

The one you are checking is for new green field project which will take time to start…it’s waiting for approvals…

The 25-30 crore capex has been completed and October 2017 trial runs commenced…I am not sure whether sales have started from that probably this quarter it will come

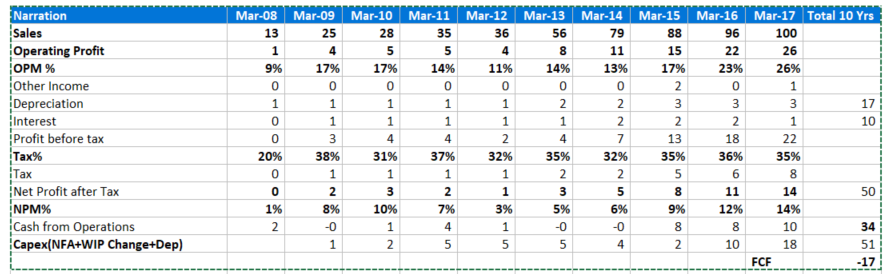

In the last 10 years , the company has not been able to generate enough cash flows to meet the capex needs. In fact the free cash flows over every year in last 10 years is negative. They are raising debt to grow and that is why not paying any dividends. Why do they require capex every year. Is the business highly capital intensive. Receivables around 35% of total sales which is too high. No doubt , the numbers and other ratio’s are great and interesting but for how long a company can grow on debt specially when it requires continuous capital. Does it have any listed Peer !

Disc: Not invested , Understanding the business

Recently started studying it, no doubt, both your concerns are correct but here is my view:

Capex : Most of the capex you see happening is maintenance capex. Substantial Gross Block were added in 2011,2013 and 2016 and 2018. As per my understanding capex is required additional products in portfolio…How can they grow top-line without capex? After all its a manufacturing business! Also, sales are consolidating for past 3 years because of high utilization levels

Regarding high receivables : That is a high concern but it seems to be norm in the industry and they get compensated for this in terms of higher margins, refer to this excellent Q&A done by valuepickr community http://www.valuepickr.com/resources/2044/

They need to raise debt because of higher WC requirement which is due to higher debtor days (which management explained will continue)

PS- Sequent Scientific Ltd is a peer but they are targeting regulated market unlike NGL

I my opinion some small proportion of receivables going bad is part of every B2B business, but if it gets to significant amount, will need constant tracking…

I had the same concern… maybe they are expecting return higher than cost of additional debt and don’t mind leveraging their BS ( I agree with you here, they should not be doing MF thing at the first place and focus on core business)

Yes they are milking company nicely but they might be there only source of income but if they keep on raising their salaries then it should be a critical concern…promoter had other servicing business as well but it seems to be no more functional as per MCA data…

You are wrong @bharat19. Promoters are conservative when it comes to capex here…

It’s not about cash flows… In terms of taking debt too they have thought for a long…and only from last two years they took it…

@aashav23 and @bharat19 - Good to see your concerned effort in getting further business understanding. One request is do not use the forum as workbook for every intermittent query - adding up a long stream of unnecessary posts. Spend time in going through the ARs of the past few years, gather all your queries and then present your consolidated findings to the forum. It would be useful for yourself and for all other boarders too. Thanks.

@paresh.sarjani1 The point bharat was trying to highlight was that if Capex is always greater than OCF, it is a never ending cycle for a company. Yes, he is right about lack of FCF generation, however companies need to achieve that inflection point where incremental capex can be handled by OCF and FCF generation starts. NGL is approaching that point but is not there yet.

Also there was some concern about receivables and cash flow trends. It is always important to observer trends - improvements / deterioration as compared to absolute numbers in 1 year, as absolute numbers are often of little relevance. As you can see from below receivables growth is largely in line with sales growth. While last 3 years of OCF trends and key metrics (OCF/PAT and OCF/Sales) clearly signal improvement as compared to the 12Y aggregates.

i normally use financial data from past ARs as i found data from screener to be a bit off in the past.whats been your experience lately.i ll delete this message from the forum once you reply.if you do at all

You have made a valid point on the investments done by the company despite being in growth phase and funding the same through debt. Ideally, they should have utilized this money to reduce debt. Earlier, till 2017, I felt the investments would have been there to have some liquidity as they were undertaking a big capex (given their size…the gross block as doubled as per March 18 balance sheet). For eg…recently they had some fire at their plant and during such un-expected times…some liquidity helps.

I don’t believe too much in net free cash flows (very rare in growing manufacturing companies). I generally look at operating cash flow over a block of 3 year period vs net profit figure.

sir,above mentioned lines excites me but unable to properly understand it,please elaborate it for the understanding of new investors like me or tell where should i clarify above lives.I think it is based on clarity of thoughts and deep fundamental understanding & experience of Yours, please help me sir.

Operating cash flow is actually what you get from operations.

Net Free cash flow is the amount that is left over after considering all capital expenditures that might be required to maintain or grow a company.

Example: You have an existing lemonade shop. The shop returns Rs 3 L as annual profit that you can safely park in the bank. But, you decide to expand your business and try to either enhance your machines or expand into new locations. In that context, let us say that you clock in an expenditure of 2L for that year. Now, the net free cash flow would be 3-2 = 1L.

For growth or/and capital intensive companies, the net free cash flow will be very less as they heavily invest in themselves or have high leverage (and hence the associated costs)

Big capex completed where Net block has increased from 25 Cr to 56 Cr. RoCE appears down because of this.

Capital turnover has been dropping for last 4 years

OPM quite low for FY18 which I presume is due to Crude

EBITDA per rupee employed (Capital turns x OPM) is down and is on a downward trajectory

Debtor days is down but so is the inventory turnover.

If the company is able to get back to capital turnover of 2 levels seen in FY15 and OPM of 20-25% levels seen in last couple of years which can happen if new capex starts contributing and crude drops down. I am assuming crude is causing RM impact on margins but the AR has no such mention however material costs seem to be rising so my assumption is that its due to crude.

NGL FINE CHEM FY18 Annual Report Notes.

Company did not reveal much in the Annual Report 2018, though first time it talked about the quantity of animal and human API. Much more information was covered in Management Q&A here.

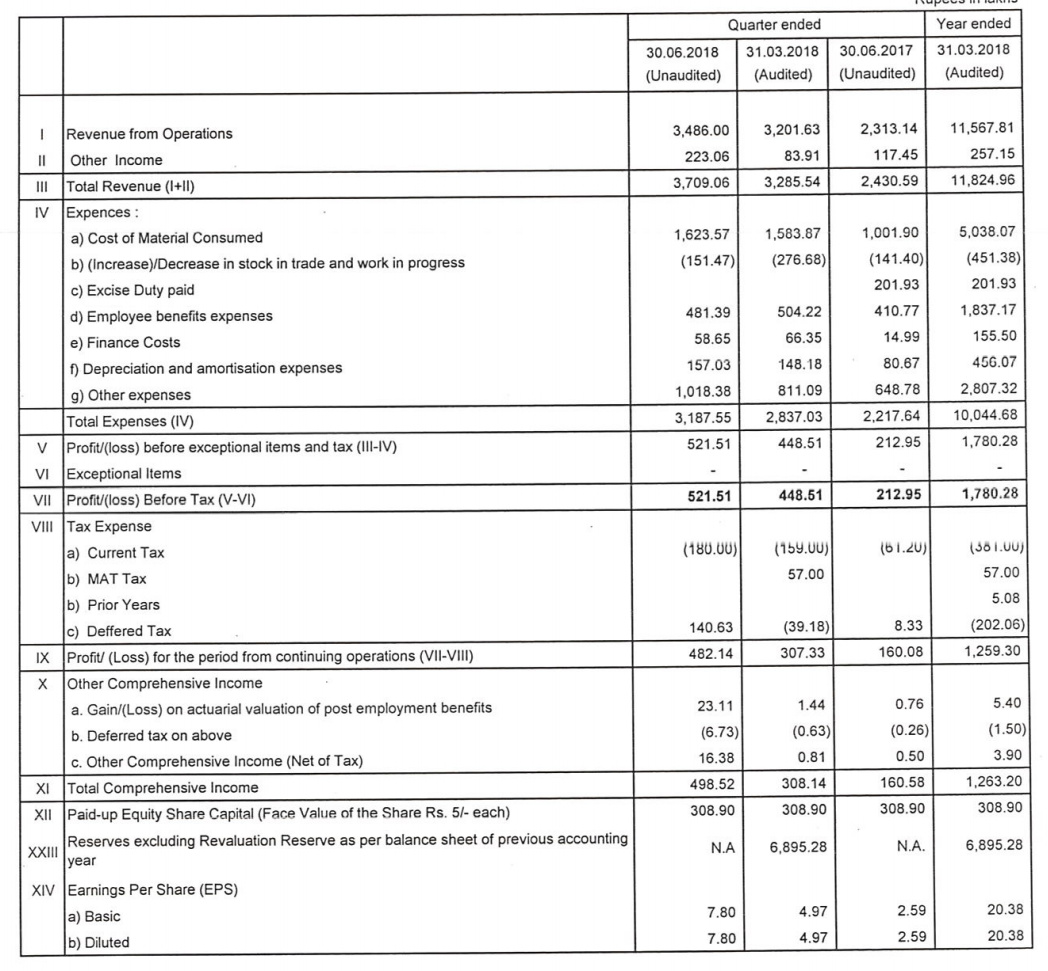

During the year under review your company achieved a sale of Rs. 11,567.81 lakhs (previous year Rs. 10,647.53 lakhs) resulting in an increase of 8.64% over the previous year. The profit before tax is at Rs. 1780.28 lakhs (previous year Rs. 2281.40 lakhs) resulting in a decrease of 21.96%. Profit has decreased to Rs 1263 lakhs which is an decrease of 14.7% over the previous year.

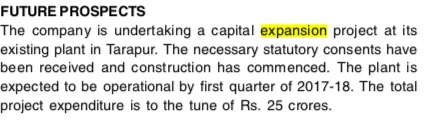

The company’s expansion project in Tarapur has been completed and trial runs have been undertaken successfully. Capacity ramp up are expected in Q2 of the current financial year. We expect to have double digit growth in sales from the new capacity roll out. (As per AR2017 it was expected to be operational by Q3FY18).

Our focus is not the developed markets of America, Europe and Japan but the developing markets in rest of the world. While these are price sensitive, the opportunity exists to enlarge market presence and deepen the reach. We plan to extend our reach in these markets and improve our performance by being one of the most cost competitive producers.

The company now manufactures 18 APIs in the veterinary range and 3 APIs for human health. These products belong to different therapeutic categories such as anthelmintics, endo paraciticides, ecto paraciticides, growth nutrients, etc in the veterinary range and angina, anti malarial and anti diarrheal in the human range. We expect to have continued growth with better market penetration.

Excellent Cash Flow numbers. Cash flow from Operating activities increased from Rs. 10 cr in FY17 to Rs. 23 cr. (excluding Non Current Liabilities & Non Current Assets). Company has used the cash to fund Capex without substantially increasing debt.

Total addition to the Gross Block during the year was Rs. 36 cr. Additions during the year and capital work in progress includes Rs. 69,24,515 (previous year Rs 18,51,023) being borrowing cost capitalized. In Plant and Machinery addition of Rs. 29 cr during the year over opening gross block of Rs. 15 cr, that’s a very substantial amount even after removing the borrowing cost capitalised amount

Cash and Investments of Rs. 10.2 cr and Debt of Rs. 23 cr. Net Debt of Rs. 13 cr.

Foreign Exchange Earned Rs. 8696.78 lakhs and Foreign Exchange Used Rs. 986.35 lakhs.

Sale from Allopathic Medicines: 86.47% and Chemicals Used in Pharmaceuticals: 13.53%.