I would think, absolutely no correlation. As a company grows it starts activating (or managing better) their branding and communication programme. Media visibility is merely a result of improved Public Relations and should be viewed as a positive rather than negative

from past interactions with management, I feel the promoters are

conservative people who are hesitant to dilute equity. The entire complex

is likely to be built up using internal accruals only.

IMHO, the promoters are talking to the media in order to increase their

exhibition business. Higher visibility in the business press will help them

easily get more exhibitors and tenants for their IT building 4.

I notice that some exhibitors who had conventions in other parts of Mumbai

are also shifting to NESCO.

disclosure: holding

shiv kumar

2 Likes

Businesses that generate steady cashflow generally have low ROA hence these are generally leveraged to generate acceptable ROE. With steady cashflow, it is easy to service the debt so leverage is generally used. Nesco is in a sweet spot where it has steady cashflow with good ROA. That’s Nesco’s moat.

Generally businesses with similar cashflow can be leveraged 2 to 4 times. ROE will jump to 30-50% in that case. Promoters are too conservative and expecting either ROA to drop or cashflow to get volatile. Let alone a QIP, company should buy back shares and increase leverage to boost shareholder returns. However, since current ROE is 22%, there is no pressure to increase it further. Return on incremental capital is also a healthy 20%

2 Likes

buyback should be ruled out because management wants to plough back profits

in constructing IT building 5 after IT Building 4 is completed and also

rebuild the exhibition centres. So one can expect only bonus and stock

split for the next ten years at least.

shiv kumar

To me the company seems to be a multi year compounding investment.

They would rather invest the cash to build infrastructure which will fuel future cash flows, rather than going in for buy back.

Attached is the revised model based on latest management guidance…

NESCO_model_v3.xlsx (21.7 KB)

13 Likes

hi vivek,

few queries on your model:

their IT 4 shall be ready by mid year 2018. should you not take 120 per sq ft rent from the time its leased?

also some tenant would get into long term lease agreement and their rent hike could be less than 5%? os 5% assumption based on their earlier increase in rent for IT park1/2/3,

also i think in ROCE calculation, you need to correct cell in formula to get income for BEC which is coming in later years as 401. due to this , ROCE is wrongly showing as 8% instead of 27%

1 Like

Hi Rohit,

Thanks for closer look. Agree on ROCE, I have not updated this tab since this was used to prepare the presentation last year. You can ignore it.

For query on IT 4, you are right, as per management interview the building will be ready by June 2018 and furnishing would be done by Sep 2018. Hence it will be leased for 6 months for FY’19. If you see, in the model I have used 50% occupancy to reflect this. And yes rent hike is also as per historical trend of other IT parks.

If you see by using this rental and occupancy of 50% we are getting 100 cr of revenue which is exactly what management provided in guidance and same way for next year of 200 cr. So, I am assuming that our assumptions are sync with what management is projecting.

Feel free to let me know if any further queries or any further insights which we can use to update model further. Many thanks.

5 Likes

Hi Vivek,

Thank you for such detailed modelling. Based on your model, what

could be the intrinsic value of Nesco?

Regards

Bharat

I believe…forward PE of 20x-25x is fair multiple if business can grow CAGR 20%+ net income for next 3-4 years.

2 Likes

Hey Guys,

Any idea what the status of the order from the Mumbai police to Nesco, on not accepting bookings for more than 50% of the capacity of BEC on weekdays?

If it is implemented, wouldn’t BEC’s topline be impacted in a major way? And any idea what has been the historic capacity utilization at BEC?

Also, its encouraging to see that commercial space leasing has grown by 8.5% in Mumbai in 2017, but any idea on the commercial real estate inventory in Mumbai, that would be on the block in the next couple of year?

Thanks

IMHO impact would be very little since NESCO presently does not take

bookings for more than 100 days a year. Also the biggest hall is reserved

for events and not exhibitions.

shiv kumar

Nesco discussed at Manual Of Ideas 2018 seminar…

6 Likes

hi vivek,

can you share key takeways from the seminar as access to nesco is limited to members

thanks!

Thanks @vivek_mashrani for the excellent projection sheet and ongoing updates on Nesco. My assessment is that you have been prudently conservative in some of the assumptions. In a way thats the right way to go about.

Generally, DCF based valuation can be tricky due to number of assumptions to be made and moving variables with business. However, feel that this kind of business can be a good fit for DCF valaution.

Have added a new tab to calc the discounted valuation. Key point is that I am going by PAT (as projected in your spreadsheet model + factoring-in for CapEx basis management guidance) since direct visibility of FCF could be difficult due to lag in different buildings coming on stream. This PAT based approach should be a good proxy to FCF since even today OCF and Net profit are matching aptly for last 3 years.

NESCO_model_v3_01212018.xlsx (24.3 KB)

To me, basis current visibility and with certain assumptions, even after the run-up this is a at approx. 3% discount to future cash flow. Assumptions being, 12% discount rate, 10x multiplier for terminal value and major chunk of capex going into FY18-19.

Thanks again for all your effort on this thread. This has helped me a lot.

Thanks,

Tarun

6 Likes

Thanks Tarun for adding one more important dimension to the model. Ideally we can assume some depreciation as non-cash item in FCF. This means we have additional margin of safety broadly at current valuation.

2 Likes

hi vivek

in your model, you have assumed continuing income from building 1&2, while one of recent research mentions that both will be destroyed to expand BEC and hence no income will accrue from these 2 building from FY 19 onwards. As BEX expansion will take some time, have you considering making the revenue NIL from these 2 buildings?

2 Likes

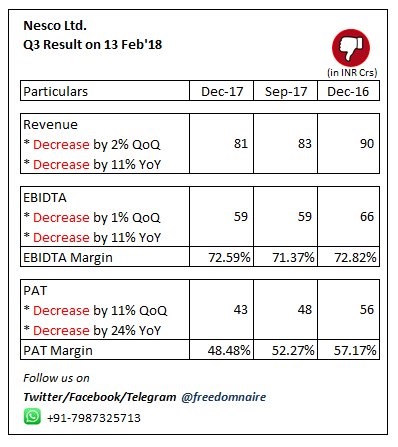

NESCO Q3 Results:-

:

Courtesy:- @Freedomnaire

what happened ? I turned bullish on and this happened