Investment Thesis - Long

Date : 13 June 2018

Navneet Education Limited is in 2 lines of businesses – Publication (since 1959) and Stationary (since 1993) and is based out of Mumbai.

- Publishing Business

The business contributes 55% to company’s total revenue (80% to profits) as of Mar 2018. Company is a publisher of workbooks (48%), supplementary material like Guides/Digests (35%), and last minute revision material (17%) catering to students from Grade 1 to Grade 12 studying in the state board schools of Gujarat and Maharashtra.

Of the above, workbooks are prescribed by schools, and thus the company has a marketing team of 350 members (as of 2016) who convince schools to prescribe Navneet workbooks as a part of student’s curriculum.

Reference Guides are suggested by school teachers or the tuition teachers and the choice is generally based on the content, author and some level of social proof (tend to stick with the known names since reference books are in addition to the normal textbooks and purchase rarely exceeds more than 1 reference book per subject)

Company’s “21 most likely questions” are last minute revision sets that are targeted to 10th and 12th Board exam aspirants since they cover a subject in a concise manner such that the entire subject can be revised in 1-2 days, and continue to remain the top selling revision sets over the years.

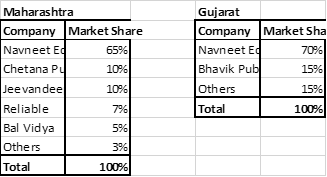

Long standing association with schools along with focus only on 2 state boards has resulted in the company having a market share of 70% in Gujarat and 65% in Maharashtra in their addressable markets, with low competitive intensity as can be seen from below -

Due to their size, NELI is one of the few publishers that have a variable royalty model with the authors wherein royalties are paid at a rate of 2-8% of the sales value (average royalty – 3.5%), while the industry practice is of payment of a lumpsum royalty. This not only helps in creating a stronger cost structure, but it also creates a network effect in terms of attracting new authors, since addition of a new author on Navneet’s roster leads to increase in sales and increase in sales brings in even more authors lured by the variable pay.

Below is the comparison of the cost structure of Navneet with S. Chand, pan India CBSE publisher -

As of Mar 2017, company has a total of 225 authors on its roster (some being retired school principals, exam setters, etc.), while as of 2014, they had retail touch points of 60,000.

- Stationery Business -

94% of company’s stationery business is related to paper stationary like notebooks, drawing books etc. (55% - Domestic and 45% - Export) while the remaining 6% includes pencils, erasers, crayons, etc. (all domestic)

The organized paper stationery market in India is only 20% of the total INR 100b market with ITC (Classmate) and Navneet being the top 2 players. ITC has been gaining market share over the years on account of high spend on Advt. and higher margins and credit period to dealers (its total market still 4%, while NELI has 1.4%).

In the export, 73% of the company’s exports are made to US (Walmart pvt label being a major customer), with remaining exports in EU and Africa. 100% export stationary is manufactured in house, while 50% is outsourced in domestic business. Exchange rate fluctuations and paper prices are important factors for this low margin business (10 year Average margins – 10.6%) and there is no competitive advantage here. The retail touchpoints total 85,000 in India.

Risks to an investment in Navneet -

- Acquisitions

a. K12 Techno - In 2011, company acquired 25% stake in international school chain K-12 Techno Services (manages Orchid International schools) for 488mn (7% of 2017 NW), which has been loss making currently.

b. Britannica – in Dec 2016, company purchased the curriculum business of Encyclopaedia Britannica (India) Pvt. Ltd. For 762mn (11% of 2017 NW). This division publishes content for CBSE and is currently used by 6,000+ schools and 5mn students. Based on FY2016 financials, this is a low margin business (3%) with NELI paying 1.1x Sales and 33x PE.

c. Company has been increasing its in house investments in e-learning (digitizing its content and offering to students through hardware), committing 1,566 mn (23% of 2017 NW). Although the sales have been growing at 30% CAGR since 2011, the division has not yet broken even and as yet, is making losses.

2. In 2017, the government mandated all state education boards to follow uniform Math and Science syllabus. The same might leave NELI open to competition from national level content providers.

However, the above can be mitigated with vernacular expertise (80% students study in te state specific language) and the existing author school relationships.

- Syllabus Changes

Since 2nd hand books are the biggest competitors to NELI’s current sales, syllabus changes bring in the bulk of the revenues and any shift in syllabus change timeline (currently once in 6 years) may lead to decline in revenues for the company.

Other important points –

-

In case of Navneet, the adverse M Score overstates the chances of manipulation. More than 50% of company’s revenues are clocked in June quarter, due to start of the school term investments in inventory and receivables in March is very high.

-

In its last 23 years, company has never earned below cost of capital, has paid a dividend in all years and has SD of 3.5% over average RoNW of 24%.

-

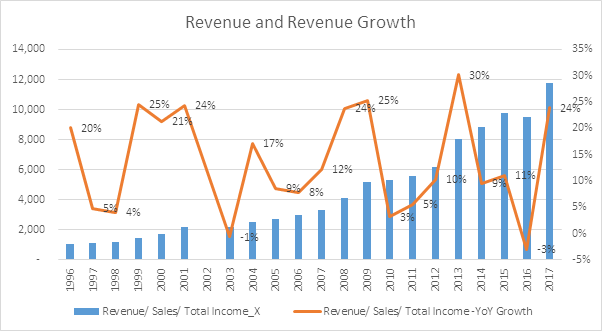

Due to the change in syllabus once in 6 years as mentioned above, the company’s revenues grow in a non – linear manner with 2 years of soft revenue and 1 year of strong revenues (when syllabi of multiple years change), as can be seen from below –

Valuation: Naive DCF with the following assumptions -

EPS Growth Rate - 13%

FCF/EPS Ratio - 45%

Terminal Multiple 14x

Starting EPS - 9.4

The valuation band comes to 80 - 160 after applying 35% MoS to the DCF value, and with CMP of 130, a case for an investment can be made.