Also, Sold Repco. Can not trust Ministry of Home officers running the company? If there is default on loans I guess govt will step in to provide loan waivers.

I would like to invite review comments from forum members about composition of portfolio especially @hitesh2710 ![]()

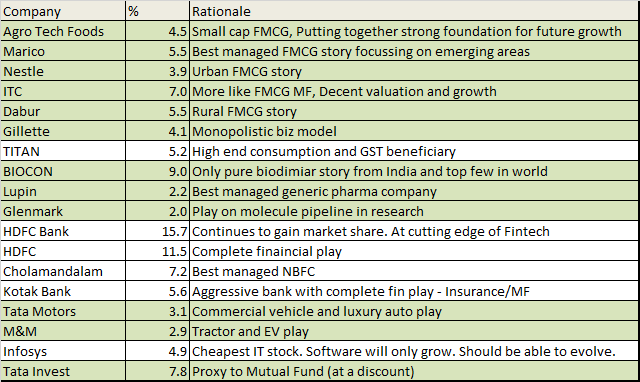

Please note that I am almost 100% in equities so bias towards a capital preservation portfolio.

If you are not a conservative investor, then I would sell Nestle, ITC, Dabur, M&M, Tata motors and Infosys. These stocks will provide marginal returns, not great returns. I would look into new sectors like Airlines, Insurance, related to Electric vehicles, chemical companies which are growth sectors. Markets favours growth stocks.

Thanks. I am a conservative investor.

I also need to manage risk as I am fully invested in stocks. So other way to look it is to consider these 28% of portfolio equivalent to debt portion in a balanced portfolio meant for capital preservation. I know that may not be best way to look  . Capital preservation over 2-3 years is paramount.

. Capital preservation over 2-3 years is paramount.

Have been exploring insurance but I don’t find valuations reasonable and insurance cycles are long and underwriting quality is completely unknown.

EV - Tata and M&M should make headway. Searching for auto ancillary in this space. Can not find any.

Chemicals - They costly for commodity nature of biz.

Airlines - Looking for reasonable valuations.

Chemical Industries- what pharma industries were at 6-7 years back, chemical industries are at the same stage now due to plants shut down in china. Most of the stocks are trading at 10-17 PE, Please try to buy if you get any correction.

Airline stocks- I will suggest to buy Spice jet on declines and i am invested in it. Going forward, Indigo and Spice jet will be the leading Airline companies in India.

Insurance- Try to invest in HDFC Life insurance IPO and agree that valuations can be expensive but there are exceptions like Dmart and HDFC Life insurance falls under same category.

You have a good collection of companies most of which are rock solid. But i get the impression that it looks like a defensive portfolio with a lot of fmcg/consumer names and large caps like hdfc twins and tata motors and m&m. This offers good downside protection if markets were to correct from here.

I personally would prefer companies where i could clearly visualise strong growth or a change in fortunes. Having said that, since you are a conservative investor, the PF seems suited to yiur purpose of capital preservation with moderate returns.

1 Like

Thanks for asking something I may find difficult to answer. It would depend a great deal when you have entered, when you have added, when you have exited partially if so. To do that I can share what I metrics prepare for investing portfolio:

- Average Amount of winner

- Average amount of looser

- Average margin of % profit for winner (more than year one the compounding return)

- Average margin of % profit for looser (more than year one the compounding return)

- The largest looser

- The largest winner

- Cash or equivalent holding against total portfolio

Analyse the looser why it happened? It would answer 90% of your questions without asking anyone. Don’t get me wrong, extremely difficult to vet anyone’s portfolio.

Few general questions may help:

- They are all companies with having big balance sheets. Are you comfortable in analysing? I was holding Larsen for long time before I realise company is too big to understand.

- What kind of valuation methods you are using?

- How do you take position (amount invested) each time? Do you average out or average up?

- When do you plan to protect capital i.e. what loss?

- I find good amount of prediction in your statements. You said software will only grow. I think completely reverse, because market itself is not respecting. In fact I am wishing the money of institutions stacked up in software should go some where else. So align your thinking with contrarian opinions as well.

Finally I leave you with a thinking: Glenmark Pharma

Good business may not be good investment. Please focus on risk management, more important when you deal with established names. Or else it won’t provide much returns in every market situations.

Thanks

6 Likes

Thanks @The_Confused_Consult.

Most of my holdings have been there for > 3 years and therefore in profit. Will need to go back and calculate compounding returns. Agrotech has not given any profits.

My recent holdings which are profitable are Gillette and Dabur.

My recent holdings which are under losses are Tata Motors and Infosys.

I am holding very little cash ~3%. My cash holding is never more than 10%.

I am not doing very deep balance sheet analysis. It is call on company’s products/services and management. Normalized PE, Growth and RoCE is what I look at.

I tend to buy desired amount within a short period of time if I find valuations are reasonable.

Capital protection: I look at high quality companies bouncing back after correction. I am very poor at timing.

Software: Markets can be wrong. It is just made of people and their understanding of biz. I have noticed that our market(compared to west) is inefficient in valuing IP based biz. At one point of time, market was valuing Ajanta Pharma more that Biocon. Which was ridiculous.

I agree and I think u can add Bosch ltd at current level to your portfolio in the electric car and tech play. It might not be a multi bagger but in my opinion it can provide superior returns than the likes of Infosys.

Disc. Invested.

Thanks @vaibhav101

I like Bosch but I am afraid that EV work happening in non-listed entities of Bosch - Bosch Chassis Systems India Limited and Bosch Electrical Drives India Private Limited. Listed entity is highly dependent on diesel/gasoline engines. Also volume of Bosch component going into EV will much lower compared to traditional engines.

In addition Bosch growth, RoE, dividend has been lower in last 3 years compared to Infy. But trades at 3x valuations of Infy. I don’t see any value in scenario where their moat is likely to be disrupted with EV technologies.

@nav_1996 @vaibhav101 I was searching for some discussion on BOSCH and came across this thread.

Need your views on the business prospects and any other micro or macro element related to the fundamentals of Bosch.

Disc: I have about 6% of my portfolio invested in BOSCH bought at around 25K … Basically I inherited this share when I closed and withdrew my PMS stocks. Since BOSCH is a well known brand I have been holding it since 2015 …

It is now trading at around 18K … and as per technical charts, is consolidating between 16K and 25K … Though a lot of Auto scrips like Maruti did very well, Bosch has been lagging behind in sentiment.

There is not much debate as probably few retailers hold these high priced stocks.

Did a bit of research … and here is the update from SMC Results update (Broker report) :

Bosch Ltd.’s quarterly profit rose for the first time in five years on the back of a

marginal increase in effective tax rate but below market estimates.

The auto component maker posted a net profit of Rs 281 crore for the December quarter,

around 30 percent higher than the corresponding period a year ago. The company said the

positive result was achieved on account of higher sales volume, improvement in material and

personnel cost.

Revenue rose 14 percent year-on-year in the three-month period to Rs 3,071.9 core.

Key performing division was the gasoline systems business, which registered an impressive

growth of 37.1 per cent.

Sales of the diesel systems’ division registered a similar growth of 33.6 per cent, the company

said adding that its automotive aftermarket division witnessed a stable growth of 4 per cent

after recovering from GST transition.

Management Comments

Soumitra Bhattacharya president of Bosch Group in India said: We expect to remain on

a path of growth in both areas in the current business year and are well prepared.

I don’t track this company closely. Can you check what businesses/size eleven unlisted Bosch entity have compared to Bosch lndia Ltd. That should give an idea if “cheese is moving to unlisted entities from listed entity slowly” or not. My fear is that futuristic growth drivers may be in unlisted entities. Listed entity may just be left with traditional biz with sub-par growth.

You dont frequent your own portfolio thread that much. I chanced upon your first post and liked the concept of playing safe, solid and steady. Wealth preservation is often forgotten in the quest for wealth creation.

Not taking extreme sides though, I find after prolonged slow growth/stagnation, the financials (TTM) of BOSCH & Colgate Palmolive better/ improving in 2018-2019. Nothing spectacular but yes, better than may be last 2-3 years. Is this due to low base effect or indeed sustainable.

Considering both are High Quality Companies, whats your view. Do you own any of these or have plans to. Eager to know your though process on these 2 from a 3-5 year future perspective.

1 Like

Bosch is no as auto components it makes for combustion engines is being disrupted. They are launching new products thru unlisted subsidiary.

Colgate is evergreen. But for this level of growth I have ITC which is much cheaper and better div yield.

Will post my portfolio. Very little has changed.

1 Like

Only If you are comfortable you may share bit more details on the below…

- How long you been investing

- Is Conservative approach a recent approach or you believed in this for long

- What’s your average return cagr… Range. Is it better than index or MF

- Don’t you miss, not participating on fast growers and multibaggers

I have been dabbling in stocks since last 15 years but started seriously only since 8 years.

I started with being more conservative. I strongly believe in it. You win by not loosing.

Everyone doesn’t have to be RJ and Buffet. We just need to create a corpus for a decent living.

My returns should be around large/multicap funds. I haven’t compared. I don’t think it is important. Multiple advantage - you get dividend, MF owns stocks which I hate (Vakrangee/Manpasand and many more), you can really own businesses you like for long term.

I own companies which had grown fast in past have been few baggers like Chola, Titan, Marico. One does not need to own low quality businesses which goes up 5 times and then comes down by 80%.

7 Likes