Natco Pharma results are out.

Revenue has increased by 28% YoY and Net profit has increased by 93% YoY

Natco Pharma results are out.

Revenue has increased by 28% YoY and Net profit has increased by 93% YoY

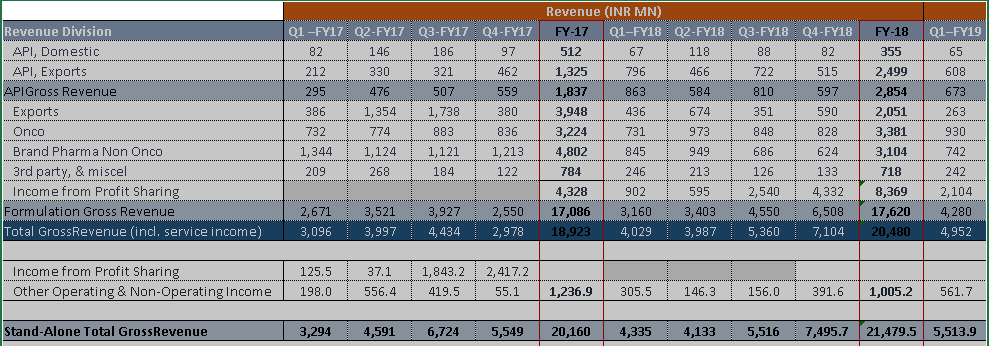

Total Consolidated Revenue increased by Rs. 125.80 cr yoy from Rs. 448.70 cr in Q1FY18 to Rs. 574.5 cr. in Q1FY19. Out of this Income from Profit Sharing increased by Rs. 120.17 cr., Domestic Oncology Formulation increased by Rs. 18 cr. and Other Income increased by Rs. 32 cr. Almost every other business segment of the company showed decline in yoy revenue numbers, something we need to keep a watch on.

Latest Investors Presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/24274c20-032e-44a7-899d-6ccc30df1a0e.pdf

Regards

Harshit

NATCO PHARMA FY18 Annual Report Notes

945.5 million (net). Amongst these, Canada was profitable with about737 million in revenue, while our arm in Singapore had a fruitful year with eight product approvals.Regards

Harshit

Disclosure: Invested

My take away from Q1FY19 result and concall:

gCopaxone - Approx 18% market share (think this was 15% start of the quarter). So far Mylan + Natco has been conservative on pricing war with Teva. Mylan’s gCopaxone was pitched just 14% below the brand price, i.e. $5,000 vs Teva’s $5,800. However, off lately Mylan has been into all out showdown with aggressive 60% price to $1900. This is expected to shift market for them fro incumbent. Other important aspect that Natco management acknowledged was that this is not entirely pricing aspect, from therapeutically perspective this has some short of stickiness due to which the market share acquisition

is slow.

Hep-C franchise: There was a slow down in run rate from ~110 Cr/Quarter to 75 Cr/Quarter. Management assessment to stabilize around 85ish Cr. Expanding foot print to rest of the word particularly condensed pockets of HepC like Indonesia and Philippine. based on past comments, 12 countries has HepC approval against filled for 30 countries.

Though recently NPPA has imposed price cap on certain Hep C medicines however may not have significant impact o Natco as its flagship drug Velpaat is already priced much lower than the cap. (this was indicated in one of the concall as well, think in Q3’18 call)

http://nppaindia.nic.in/ceiling/press04July18/FormulationPrices(50).pdf

VELPANAT ( Velpatasvir 100mg + Sofosbuvir 400mg): Proposed retail price 15482 vs. Natco price 13875.

Tamiflu: with other generics coming in fray the numbers will not repeat itself from what they saw during flue season CY17 and CY18. Though they have approval for both suspension and table now. Interesting comment during concall is that they have not booked entire profit in Q1 and will spill over to Q2. (Substantial -in managment words).

Substantial cash in books: company is sitting with whopping 1450 Cr. cash/liquid instruments. Additional strong cashflow expected from Copaxon and Doxil for the FY. Though Rajeev has been very tight lipped during concall, Investor presentation calls for inorganic growth.

CnD segment: Growing well. They had a projection of ~150 Cr topline by FY’19. Again, targeting niche products under CnD. Within a very short duration of forming CnD segment they are looking at gBrilinta for India market. This appears to be one of the top drug in US market with $1B clocking. Though have been stayed by AstraZenca:

AstraZeneca sues DRL on patent - The Economic Times

CapEx: 400 Cr. for FY out of which 100 Cr. so far utilized. Vizag plant expected to come online by mid of year.

Revlimed: Same stance, they have limited launch agreement with Innovator however can move early (as early as 2019) if competition comes in.

Targeting at least two, three FTFs this year.

Operational break even for Brazil sub by year end.

Other income break-up: approx 56 Cr. other income as against 40 Cr last quarter.

export credit 20 Cr.

Forex gain: 15Cr.

Interest income: 20 Cr.

Overall, seems that the same industry wide headwinds (short of) are at play for Natco as well. However, couple of big opportunities makes it equally interesting. Additionally, managements focus on play by strength gives some confidence.

Thanks,

Tarun

Disc: Invested, no transaction in last 90 days.

Good news for Natco

Hi All,

Natco to consider buyback of equity shares in a board meeting, to be held on 5th November.

You can read the official announcement by clicking here.

Regards,

Yogansh Jeswani

Disclosure: Holding

Back to back good result in last two quarters . Share buy back also announced at Rs 10OO. The stock is range bound for quite some time. Whether market is anticipating lower profit realisation in FY19…Can any one share some light on its future growth prospect hereon…

Market adversely reacted after publication of decent results and buy back from Open market not exceeding @Rs 1000/- Let us see how it opens in next trading session…

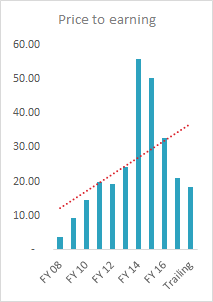

I wonder, Natco Pharma looks like an excellent value pick, kind of market mis-pricing. Any specific reasons for the same.

Growth looks fantastic.

Return ratios >30%

PE of 18

PEG of 0.34

me too wonder the same. if some one have idea on future earnings please share with us

Seems market is discounting earning from profit sharing/services …If we exclude the same result would be negetive or at most flat as far as Q1 presentation…But I am not able to understand whether this earning under profit sharing/services is sustainable for next few years or not…

Disc …Invested …

cef2640d-a3cb-4a5e-afd2-44c6596427f7.pdf (2.1 MB)

Will be interesting to go through investor presentation to see which segments have given the boost to top line.

Disc- invested for some time now. No transaction in last 6 months.

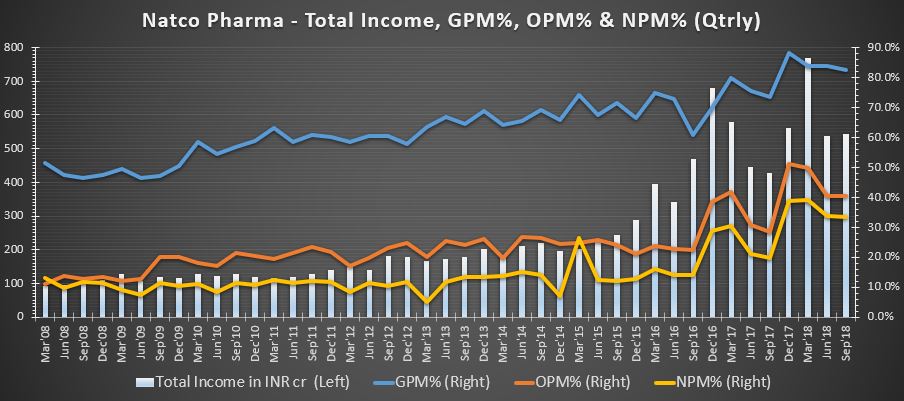

One of the best margin numbers in the sector (Divis is closest, however Natco leads). The question is, is it sustainable in the long term? High base in quarters to come.

Possible triggers

Possible dampers

Disc: On radar (no holding currently)

Concall Q2FY19 notes

Formulation Domestic Sales: Rs. 193.87 cr

Formulation Export: Rs. 247.81 cr

API: Rs. 66.81 cr.

Other Income = Rs. 53 cr

Subsidiary = Rs. 22 cr.

Our top 4 products in USA are Tamiflu, Copaxone, Liposomal Doxorubicin and Lanthanum Carbonate.

Copaxone: It is doing well. Market share increased from 15% to 20%. Our discounts are much better than Teva so price is not a challenge. New Generics not a challenge as the prices are already low. Problem is to take market share from Teva. Market share will improve further, it will show in results next year.

Key Triggers

Near Term: Increased market share of Copaxone.

Medium Term (FY20-21): Brazil, Canada and India.

Long Term (Beyond FY21): Revlimid and other exclusivities.

Capex: Rs. 400-450 cr planned this year. Already spent Rs. 200-250 cr. Three main areas of Capex will be Vizag Plant, API in Hyderabad and Oncology expansion in Hyderabad. Vizag should be completed and go online in FY19, inspections will be triggered early next financial year.

Tamiflu: Flu this year is not as intense as last year. We will see decline in flu earnings this year. Margins in current quarter reflects some portion of of delayed profits of Tamiflu of last season.

Brazil: Bullish on Brazil due to two reasons - New partner and Good Product Profile. This new partner was earlier associated with Mr. Arun Kumar of STRIDES. He has made some strategic changes for Brazil. Will see positive affects in FY19. Brazil is a Branded Generics market. For Oncology it’s tender based business. We are making 2 unique launches in December 2018 and this will wipe out our losses in Brazil, some other launches in April-June 2019. In FY19-20 we will see meaningful contribution from Brazil to our balance sheet. Base case turnover is $10mn and best case is $ 20 mn, but depends on products.

China: We are looking to enter China. Some positive regulatory changes have taken place in China. One of them is that if you have approval in western countries (USA) then they will fast track approvals in China. It will take 12-18 months for approvals in China if already approved in USA. We have 3 filings pending in China. If you get 1 product approval in China then numbers will be as good as US launch or India Branded launch. Will do business through local partners there. We are cautiously optimistic on China.

Domestic: Oncology = Rs. 97 cr., Non Onco = Rs. 79 cr and Other = Rs. 17 cr.

15-20% growth in domestic oncology will be maintained this year.

15% market share in domestic oncology market. (educated guess by management).

12-15 unique launches this year.

Hep C did sales of Rs. 74 cr this qtr as compared to Rs. 69 cr in previous qtr. Volumes and Prices are stable.

Domestic and Subsidiary sales are around Rs. 220 cr currently, going forward would like to see this number increase to Rs. 300-350 cr. in next few qtrs.

Buyback: Cash as on September end is Rs. 1365 cr. Doing buyback as cash position better than anticipated. Buyback does not mean that future investment opportunities not there.

Bullish on Oncology and MS pipeline in Brazil, Oncology pipeline in Canada, Oncology and Cardiac in India.

Focus on Non USA business. Spending 60-70% of R&D on Non USA business and 30% on USA. Earlier it was other way round.

10-12 filings in USA in next 12 months. 2-3 FTFs approval expected.

Earnings guidance intact as given in earlier quarter.

We do only niche products. We never did any combinations, so no affect of ban on FDCs in India.

Regards

Harshit

Very valid questions, Bharat. I did some high level research and found that the company did multiple QIP in past years - which explains the dilutions. Also the dilution is not a lot while at the same time as Tarun and Sandeep highlighted, the returns have been good. I did not find any reflags here - hope I dint miss anything.

It might be one of reason. Working capital to sales is very high particular to this year (~67%) & average 35-45%. Looks very high.

Hi Bharat, From which site did you get this info of Promoter & Promoter Group?

The promoter share holding had gone down from 51.19% to 48.36% because the promoter Mr. Rajeev Nannapaneni had donated 1.5 lac shares to LV Prasad Eye Insitute .

The link for the same is given below: