The amount of hard work that requires in building a sustainable business that has the below qualities:

(past)

- Return on equity (RoE) and return on capital employed (RoCE) of about 50% over a very long time (across business cycles).

- Maintain a Net debt of Zero.

- Growth of about 25% over such long period.

- Grew even in difficult times like demonitisation and GST and did not take an easy way out saying GST impacted the business etc.

- Pay out 40%-50% of net earnings as dividends. (The confidence that the balance sheet, PnL, cash flows are real is from quarterly dividends).

is NOT easy. This is NOT easy.

What is much easier is sitting at home and without building a business, no experience over business cycles and then pass comments on valuations! The proof of pudding is in the eating.

The past track record and the assurance of future growth the investors have that the company will keep growing at relatively and comparatively higher growth is what majorly decides the PE of such companies.

Understanding the reason behind high RoE, Growth and its sustainability and investing in such a company at the right balance of valuations vs. quality is real hard work and then sticking onto such businesses even during steep and broad market corrections might be lazy but is the prudent approach.

Why only a certain company is trading at high X times 2020 PE despite such upheaval in many mid caps? Why not any other company? The thousands of stock market investors are biased only towards that ONE company only and that to over such a long period? Is the company their relative? No, right?

Market as an aggregate has NO emotions otherwise companies won’t fall 60% in a day. Market is ruthless when their assumptions go wrong. So you need to do that hard work and find that balance in valuations vs. growth & quality & sustainability.

If a company has sustained a median valuation of high PE over many business cycles but you arrive at a valuation that is 1/3rd that then we must have the humility to understand that we may be going wrong somewhere and try to learn instead of broad brushing that market as a whole is wrong and that to over many business cycles.

There are hundreds of ways to make money in stock market and mine is this and others have theirs but none of our ways are lazy! (as long as they are legal)

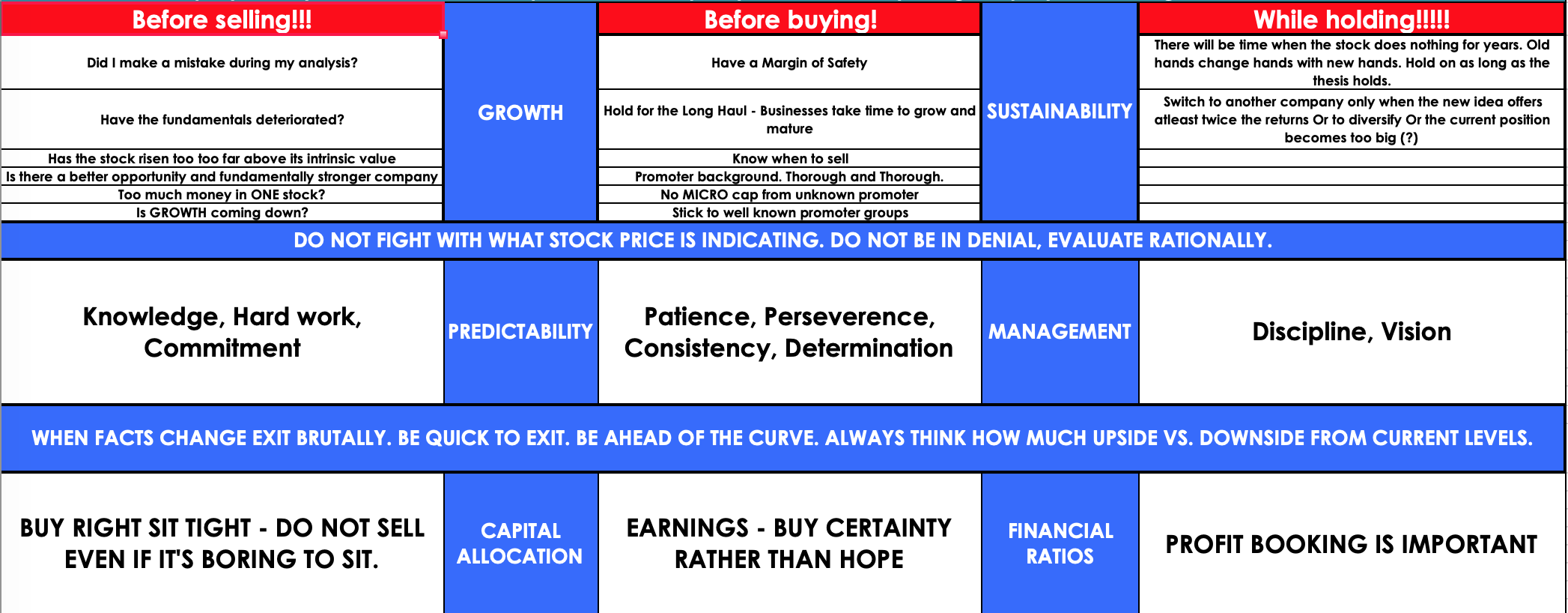

Investing in Equity market is about GROWTH and its SUSTAINABILITY. Let that sink in first.

In all humility, am not in for arguments please. These are my opinions backed by experience and good CAGR. I respect opinions that make money otherwise a lot of inexperienced people throw so much gyan, excel analysis and that too with so much confidence these days in forums that the people/new investors who really wants to learn and grow in life are being misinformed and there is a danger of getting influenced at an early stage. Again, the proof of pudding is in the eating.

Do whichever actually worked in real world scenario and not in the seemingly logical writings, including mine.

Nice strategy!

http://forum.valuepickr.com/t/page-industries/1255/624?u=richdreamz

this is where one wishes if he had a higher allocation to an alpha stock

this is where one wishes if he had a higher allocation to an alpha stock