I started investing since 2014, initially only in Mid/Large caps like Indusind, icici bank, L&T, now I seriously want to build long term portfolio and more importantly decent returns.

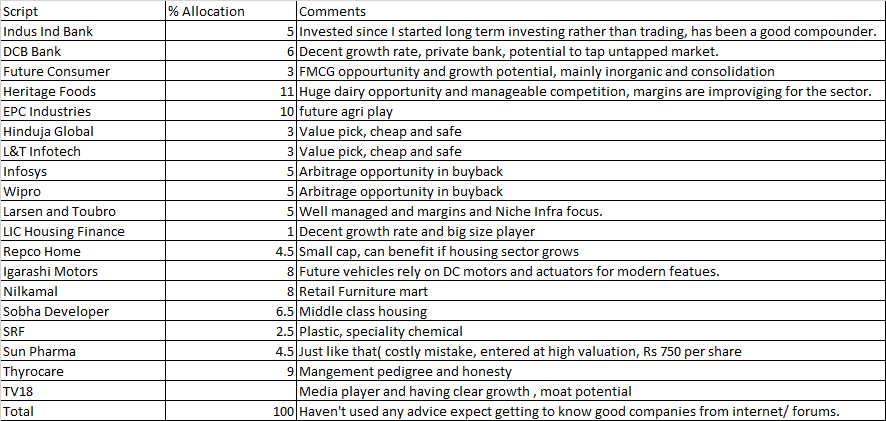

Script % Allocation Comments

Indus Ind Bank 5 Invested since I started long term investing rather than trading, has been a good compounder.

DCB Bank 6 Decent growth rate, private bank, potential to tap untapped market.

Future Consumer 3 FMCG oppourtunity and growth potential, mainly inorganic and consolidation

Heritage Foods 11 Huge dairy opportunity and manageable competition, margins are improviging for the sector.

EPC Industries 10 future agri play

Hinduja Global 3 Value pick, cheap and safe

L&T Infotech 3 Value pick, cheap and safe

Infosys 5 Arbitrage opportunity in buyback

Wipro 5 Arbitrage opportunity in buyback

Larsen and Toubro 5 Well managed and margins and Niche Infra focus.

LIC Housing Finance 1 Decent growth rate and big size player

Repco Home 4.5 Small cap, can benefit if housing sector grows

Igarashi Motors 8 Future vehicles rely on DC motors and actuators for modern featues.

Nilkamal 8 Retail Furniture mart

Sobha Developer 6.5 Middle class housing

SRF 2.5 Plastic, speciality chemical

Sun Pharma 4.5 Just like that( costly mistake, entered at high valuation, Rs 750 per share

Thyrocare 9 Mangement pedigree and honesty

TV18 Media player and having clear growth , moat potential

Total 100 Haven’t used any advice expect getting to know good companies from internet/ forums.

I don’t have any specific theme since I want long term portfolio, current allocation is not ideal but I am going to re balance , dollar cost average.

Books following( Intelligent Investor-Benjamin Graham , Security Analysis( Benjamin Graham and David Dodd ), Rules of Weath- Richard Templar).

Articles: Buffet letters to Partners.

hi, you have almost created a mutual find . I just looked at your Heritage foods, i fail to see how its a fundamental buy ? It has no MOAT, no pricing power and to me it appears to be just a run of the mill dairy business. Or am i missing some. What will you say is your most fundamental Pick ? i will look into it and may be buy it if it fits my MOAT business.

Hi Dobhal, Heritage management have announced that they want to increase sales from current 2400 crores to 6000 crores by 2022, primary using direct sales channel ie. using Milk parlour which seems to be a low capex, company has invested 100cr in capex for various needs. Compared to Hatsun agro financial position is better interest cover 9.74 vs 3.41( Hatsun), so they can with stand pricing pressures or commodity(milk) prices swings.

please go through the link about management future plan/forecast, http://www.thehindubusinessline.com/news/heritage-foods-sees-boost-from-value-added-products/article9832268.ece

hi Sri, its good that management is all bullish. But one thing i have learned is to take everything what management says with a pinch of salt. This company has no pricing power, no brand unlike Amul or Mother dairy , and even with Brand names these companies don’t enjoy absolute pricing power. So good luck may your analysis turn up true. Any other company in your portfolio which you say has Moat ? i will look into it and may be buy it…

Hi Dobhal, thanks for your review, could you please elaborate on the pricing power disadvantage for heritage foods?

Do you mean pricing power at customer or at sourcing? How are Amul / Mother dairy able to source a lower prices than Heritage?

Caution:**** Hi All & Dobhal, my portfolio is constructed within Last 6 months only, so its untested at the moment.

Though I am extremely confident about Indusind Bank and Larsen and Toubro which I have been holding since 2 years and added some more.

Please ignore Infosys and Wipro, its purely a buyback bet which I think is stupid, but I like to participate since there is not much risk compared to what Mr. Market is at (25 PE) and earnings growth are not improving.

I have seen Heritage gain traction in Bangalore. Mother diary and Amul do not have such a strong presence in Milk in Bangalore. Maybe this is true for the entire Southern region.

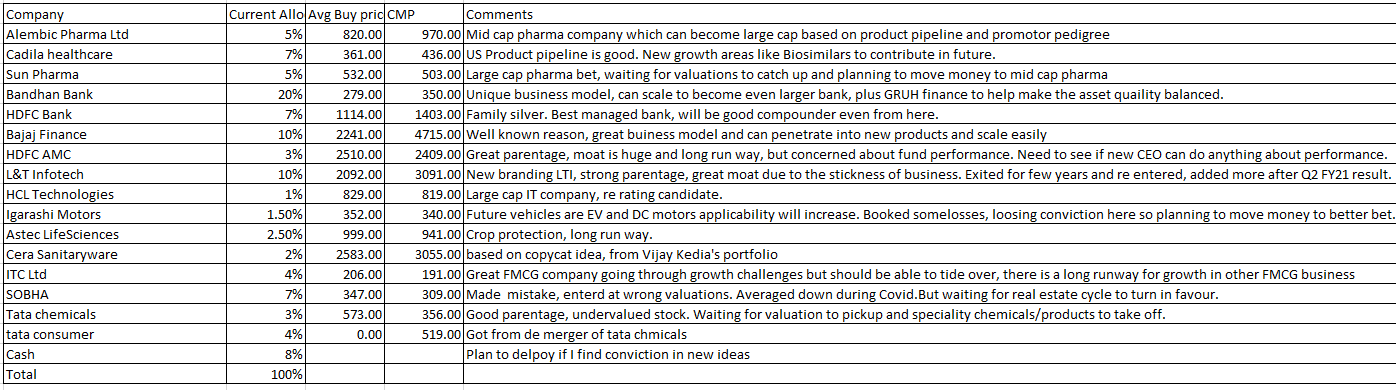

Posting current portfolio.

I work in IT industry. I have immensely benefited from this forum and made decent returns.

Aspiration is to get 15% return CAGR. Need suggestions and ideas to move to better bets and general re structuring of portfolio.

Equity still accounts for only 30% of net worth. Plan to ramp this up once I find good conviction ideas to reach aspirational goals.

Have some investments in Mutual funds but prefer equity route.

Apart from general re structuring and profit booking. Paid decent tuition fee for 8K Miles, wanted to find some diversification from L&T infotech . Booked 80% loss in 8K Miles.