Hello everyone,

I’m Abhishek, a recent graduate about to start employment. My introduction to finance came in 2013 while I accidentally stumbled upon the book Too Big To Fail (I was preparing for my medical entrance test back then!). That seems to be the turning point in my life as I felt it was finance that was what I was most interested in.

Hence gave up the medicine career for the world of Investments. I have read Buffett, Lynch, Graham, and those must-read books on investing to develop a long-term investing mindset. I won’t say I am a newbie to this field and I approach it with a 10-15 year horizon.

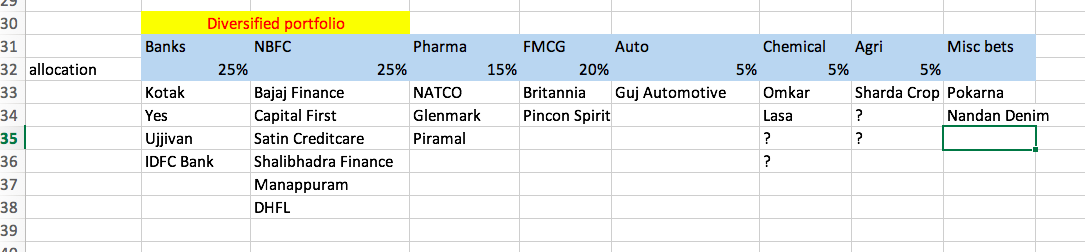

My investing process: While picking companies, I looked for Promoter quality, large headroom for growth, good ratios and growth rates in that order. I’m based towards tried-and-tested businesses with predictability. I completely avoid infra, real-estate, sugar and steel stocks which I believe is the general consensus here on VP . I am biased towards stocks that are consumer-focussed ones with strong brands that any common man who knows nothing of stock-markets knows of - Kotak, Yes, Britannia, Piramal, Bajaj Finance. I’m heavily tilted towards the finance sector as I believe this sector shows steady growth and a degree of predictability ( reasonably confident that Yes, Kotak, Capital First etc will continue to post 20%+ YOY earnings) and my belief that the new-age private banks will continue to gain market share from public sector ones.

Avoided IT altogether as I haven’t can’t differentiate one from the other (what makes Infy’s margins 22% while Wipro has 15%) and also these have grown too big to be able to grow 10x from their current levels. Couldn’t find small caps in this space with high conviction.

Same with Auto stocks, the existing ones are the leaders and are too big to be able to grow their sales by 10x from here. Had a stint once with Eicher (bought by looking around the many new Enfields in my college parking lot - the true Lynch style!) but sold out early ![]()

I stumbled upon this excellent forum a few months ago and can’t thank the people enough for their invaluable insights.

I request experts to please give me their advice and opinion of a portfolio I have built over the years and continue to deploy my salary proportionately(started in 2013)

Thank you so much.