“Beware the fury of a patient man”

1 Like

@Ediacaran97 but I think colgate will give you 10% cagr for the next decade. Patanjali who came and blitzed the market could not eat into their market share… inflation is at 6% colgate can increase prices by 3-4% if not more every year. toothpase market is growing by 5-7%. Colgate has 50% market share it will capture half of that, that itself is 8-11%. Add to this dividends that you are getting , 2% at cmp.

Total returns will be 10-13%. Simple. And you will get this for a long time and then a decent terminal value as well, since the space has low disruption and high visibilty. A de-rating could occur to 20x. Alternatively they bring in more products and go in for aquisitions or grow their mouthwash aggressively. alternatively dividends would also increase slightly over time. So you can account for that and end up making 10-12% cagr,

Very simple. When to buy? look at the median PE and take a call. But over such a long holding period the pe entry wont matter. Earnings only drive stock prices for the most part 99% of the time.

4 Likes

@dumboinvestor, there had been many complaints in the past regarding use of poor language, indiscipline. We have deleted many of such posts(88 in count) and you had been warned about the same. Looking at the continued indiscipline, your membership is suspended for three months. This is a warning to all the members who have been indulging in non civil behaviour that such things will not be tolerated.

15 Likes

Thanks for sharing the video. Its quite nice!

If I be bit more explicit about the concern I shared on lack of sufficient public information, there are essentially three kinds of reports on any listed company-

1.Reports published by the company (annual reports, quarterly reports, investor presentation etc.)

2.Reports published by the brokerage firms, independent analysts etc.

3.Conference call report - This is very important in my understanding because lot of times you would see the management being questioned on significant matters and they then divulge important details (for e.g. RJ questioning Titan management in concals!)

If you would notice, in a few instances in the past (Satyam, Vakrangee, Manpasand etc.) the management might not be truthful always to the investors. So, reports in #2 and #3 category above, help investors analyse things better.

2 Likes

Precisely only 2 things to be done as an investor.

- make a list of good companies - strong business models, clean balance sheets, able and honest managements, big opportunity (the criteria can be decided based on what you are comfortable with from the host of financial metrics at our disposal);

- And figure out the price you’d be willing to pay and then wait for the right valuation/price you’d be willing to pay (You did quote Sanjay Bakshi in one of your post - The post was titled’ “Pay up, but don’t overpay for quality.” I guess deciding the comfortable buy price is key).

I think just combining the two, you’ll be surprised by the results.

2 Likes

Horlicks sale is nearing and Nestle, HUL are front runners. Anywhere between 3bn$-4bn$ valuation of Horlicks. Now MCap of GSK Con is 30000 Cr= 4 Bn$. So I am not able to figure out impact of the sale on GSK share price.

- Sale of iconic brand Horlicks is a negative

- Cash gain of 4Bn$ is a massive positive.

Finance , M&A experts in VP- pls throw light on this. Thanks !

1 Like

Don’t really track either of these companies, but based on the media coverage, effectively all of GSK business in India is coming from the unit being sold (of which Horlicks is a big part).

GSK in India will continue to focus on Pharma (though it doesn’t make up a big part of the business right now), if i understand right. However, given the parent GSK’s strong pharma line-up, GSK India should do well in pharma. However, given that Indian pharmas are basically generics plays while GSK is mostly ‘innovative’ medicines, what role GSK India will play going ahead needs more clarity.

Effectiveky, any deal value above market cap will be good for GSK investors (as an arbitrage play). Else, Without much visility of what’s to come, taking a longer term view would be hazy. Someone with more knowledge could add to this. For me, at this point in time, arbitrage play is all i’d see.

Discl: Not invested. Take my opinion with a ‘bagful of salt’ given my shallow ‘Pharma’ knowledge

They already have a seperate pharma company listed. Does GSK consumer have any element of pharma?

I have burnt my fingers couple of times in merger/demergers…even corporates do not understand this much we are very small ![]()

I am thinking, I would invest in Glaxo consumer if I think the remaining brands can play a big role or I know their vision about their cash.

No doubt these brand sale out mergers are complex. My thought is like this. We all know its best to sell something at peak, isn’t it. Given long term outlook of malted drinks will decline as it has already, in developed countries, exiting Horlicks for 3-4 bn $ is great…that’s why I bought Gsk shares.

But what will happen to the cash, whether other remaining products will do well or Gsk Novartis will introduce newer products etc is unclear.

That’s the issue with minority shareholders. So far the share price has gained, slowly and steadily… But might exit if it falls or I fail to develop conviction. So 50:50

Gsk is trading at pe 35.

Other Pharma stocks in the range of 25 PE.

Is not like GSK is going to get into something new and and outperform the competition anytime soon. It will take time. That’s why it makes no sense to pay twice as much.

That’s exactly what we should know in order to invest long term. If not accurately, at least company’s vision in India should be known post this deal. Anyone having this info pls share. One more thing…Horlicks is not just a malt drink…it is an iconic brand…its a distribution network…and much more… it shows that company is not willing to transform and work with that brand anymore in India because its flagship product of malt drink is not growing as expected… not sure what is the vision for India for the rest brands, future brands and cash is…

My bad. Missed that. So, that brings in even more uncertainty as to what the leftover GSK consumer will do.

Its allright. With MNCs it gets very confusing in what areas they are in India. I knew this as Glaxo had been in my radar since many years, my bad that when I made up my mind to buy it, it made up its mind to sell Horlicks It will still remain in my radar as to what is its vision now for India

1 Like

Please Reconfirm PE. Its 35 to 37…where did you find 53??

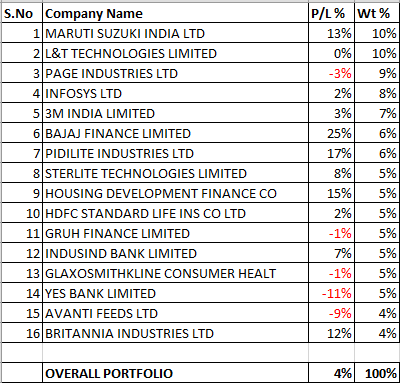

YB, Avanti & Page were laggards this week. Rest are doing fine.

Bought more of Infosys and reduced Page to have balanced portfolio, adjusted Brittania stock split.

Top 3 stocks are making less than 30%. No stock is less than 4%.

3 Likes

I have quite often come across from you, Donald and few of expert members to allocate and back your high conviction stocks the most. Even if diversification gets bit skewed.

From the beginning I had high conviction in Maruti, Pidilite & Bajaj Finance. However, I didnot load it up. After reasonable gains in the counters, still the overall impact is not great. Lesson learnt, but again only in hindsight.

Let me have your valuable inputs on averaging up on these 3 stocks and any advice that you may feel is important.

I have a month’s salary as cash

I dont follow Shankar Sharma, but this is very candid. Quiting the market out of panic or disgust is a criminal mistake. Easier said than done, esp for newbies. Although exiting to free up cash during overvaluation yet constantly watching for re-entry level is often a good idea. Some random posts…

Portfolio allocation is something that needs to be worked on with a lot of diligence. While looking at a company if it is a convincing story backed by good numbers and available at decent valuations the first thing that should come to mind is how much allocation should be made to that company. I usually reject a story if it is not worth 5% allocation atleast.

Coming to fat pitches, sometimes in markets you are presented with opportunities where you read up on the company and have a feeling that you know the business quite well, and its quite possible to trace a track in terms of its predictability of earnings, and its available at pretty cheap valuations, and you feel that at some point in the future the company is likely to catch market fancy, and thus lead to a lot of rerating, and so on and so forth. In such situation one has to have the courage to bet hard and usually I have seen these are the kind of bets which make the difference of a lifetime in terms of investing returns.

Atleast in my case I can say that some companies like Ajanta, Kaveri, Mayur, MPS, Manjushree Technopak (no longer listed I think) besides the recent big bets in companies like Bajaj finance have made a lot of difference. Even some not soo good companies but which had strong momentum in terms of price action like Everest Kanto, Kamat Hotels , LT foods etc (where I was pretty sure that there was a definite sell price – not the typical buy and hold kind of companies) with proper allocations made a big difference.

In cricketing parlance, if you are presented with a full toss ball or a free hit, its no use trying out a defensive hit. One has to try to hit a six. But for these kind of bets one has to be absolutely sure that most of the criteria I listed in second paragraph are met with.

19 Likes