3M India is the only listed company of 3M outside USA

Parent has appr 70,000 products of which only 10,000 are sold in India

3M India localizes products to cater to Indian needs and in my understanding they use their experiences to launch better and cheaper products globally as well

It has a low equity and is a MNC hence, beyond the traditional parameters of evaluation, there is a factor of demand and supply

No one is considering a capacity expansion by the company, which in my opinion is due any time

They have been smart to out source manufacturing lower margin products, evident from the bought out items in the P&L.

Good inputs But why there has been margin expansion in last 2 odd years. Sales is growing but very slow, so scale effect is ruled out. 3M products are varied so rawmaterial should also be varied. Can’t assume all raw material cost came down. So what’s the reason of margin expansion? Is this an exception or its sustainable or can be bettered?

I think, CEO Debarati Sen seems pretty competent and confidant. Read good reviews. But I don’t see hunger for growth in 3M, which a typical Indian company shows.

To answer to your question see point 6, that beside they are able to pass on the RM price hikes to customers as they have pricing power. This is sustainable in my opinion since I have been observing that they have been able to maintain it for the last 2 years as rightly pointed out by you.

The hunger for growth and expansion decisions are not taken locally but at global HQ. So, sooner or later it will happen since growth will now come from India and China.

Also note that the Bangalore R&D center is now also catering to not just local but also global requirements. I also seem at some time in future, local ops manufacturing for global requirements since it is a low cost manufacturing option ( i think its doing some of it just now).

Avanti feeds and yes bank are pure trading bets. I think they are available at cheap valuations. So I picked. Avanti is a market leader but glorious days are over. You may read avanti thread for wonderful insights. I have no genuine rationale so my answer will not add much value. Thanks @sreenu_k

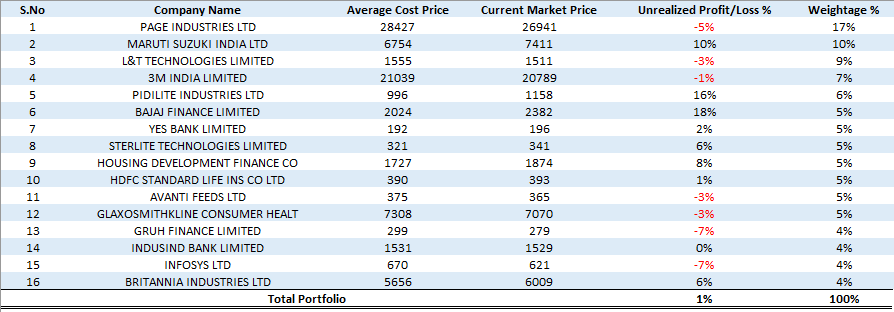

India indexes facing resistance and followed with mild correction this week. US index falling. Oil falling, rupee gaining, elections, constant hangover of over-valuation esp in quality stocks et all. This is an indecisive time it seems. At times, I feel no point identifying hidden gems as infact there are none Top it up with reports of Gold & RE returns beating equity…Nevertheless, I share my updated portfolio. In parallel, I am trying to broaden my circle of competence in quality mid/small caps. Seek Feedback !

Another funny aspect…pardon me for being silly. Oil, $ rising causes correction and same Oil, $ falling causes even more correction. News reporter seems to run out of reason. Just a month ago reports came Oil will cross 100$ and that is bad for Indian economy. Now its approaching 50$, no one is saying economy will leapfrog

A prolonged bull run ends with many companies quoting at high multiple, but only a select few of them have quality to withstand/bounce back from correction. Challenge lies in identifying these companies. In particular, you have to determine how sustainable their competitive advantage is, because that determines whether or not they generate high return on invested capital. They also must have long runway for growth. And lastly, in an economy with underdeveloped financial system, a consistent source of free cash flow is a huge advantage.

Now coming to the stocks in your wish list, many of them are cyclicals, they lack the consistency to be called quality, with them you have to be good at timing the underlying business cycle.

There is no free lunch for customers. I might be too optimistic, we have reading so many news insurance company fighting in court even for 10L insurance, which is mustard for them.

Few companies to track in a sector whose stocks are hitting or close to 52wk high ie Chemical Space

Atul Ltd

Vinati Organics

Aarti Industries

Transpek

Excel Industries

Gnfc

Sounds bad!!! However,this article has to be taken with a pinch of salt as all these details were in public domain since long ago.why not alert early??

Post your note, I looked at 3M India financials & other publicly available information to understand more about the business. For two queries I have, will need your help.

I found only 3 articles and 1 research report relevant from an investor’s angle. Isn’t this too little publicly available information to develop sufficient confidence on the business?

Also, as you would now, from shareholding perspective, the combined holding of MF + FII is stable at 11-13% in last few years. Why has the company not been able to generate interest from these investors?

@homemaker Please chip in with your views as well !

Even I didn’t find much investor information online & MF/FII holdings I have no idea.

I checked financials in screener, read few news, read wikipedia, read about 3M (USA), Annual report etc and a video of 30 years of 3M India. 2 things stood out

Focus on culture, values, R&D and CSR- sometimes I find CSR info more than core business

Co Seems satisfied with slow growth, didnt see hunger for fast track growth, that we see in India Co.

@homemaker a slow growth with consistently high roce over a long period of time will generate massive returns for you. But everyone wants that 10x in 4 years story. In order to do that you need to find a company that grows its earnings by atleast 5-7x in the next 4 years.

A hard task and perhaps a task best left to the experts in investing… (not large cap mf managers, they are mostly dumbos because of the many rules that govern them and the fact that they have only one objective, increasing aum to increase fee income and out performing the index in a 3 year period, they will under perform over a 10 year period but that doesnt matter, because by that time they will launch 10 more funds and sell those on a three year out performance due to smaller aum and as aum expands, the story repeats itself, this is in the case of large cap mfs)

Finding fast growers is not difficult. I can tell 50 stocks who have grown 30% YOY as of today. What I find difficult is most of these are not well known names or unfamiliar to general public. Mostly cyclical and uncertain longevity of that cycle. Try asking a general guy whether he knows mangalam, kanchi kapoor, aarti ind, sadhna nitro, misthana foods

However, I firmly believe VP is possibly the best and only forum to learn to identify and build conviction on these obscure super fast growers…

@homemaker Anyone can point out those fast growers. They may be cyclical as you say.

Last year we had a company by the name of vakrangee, fantastic business it was. Touted by many to be the ultimate Indian company in terms of the opportunity that they were tapping. What a business it was…If it was real… You can also screen another vakrangee now I’m sure.

Can you find a nestle growing at 30% or close yoy at a reasonable price? We have cos close to that, high quality, high growth, good industries, non cyclical in page inds and Dmart. Look at their PEs (since we all love PE).

Be careful as you might end up with 5 vakrangee’s and 5 PCJs in your portfolio… I for one cannot believe that people are saying no 15% compounding that a simple index etf will give you. Imagine doing 15% for 10 years. That in itself is 6x… I will bet that many here wont even make 3x in the next 10 years!

I atleast hope that I make around 5x in 10 years with some comfort and good sleep! Have a nice day:)

Dumboinvestor, can you explain the near stagnant or abysmal returns generated by a Hawkins, ColPal, Crisil- excellent ROE/Roce, in oligopolist sectors, but poor revenue generation last 5 years. Slow growth is reflected in their share price appreciation in last 5 years.

But why there has been margin expansion in last 2 odd years. Sales is growing but very slow, so scale effect is ruled out. 3M products are varied so rawmaterial should also be varied. Can’t assume all raw material cost came down. So what’s the reason of margin expansion? Is this an exception or its sustainable or can be bettered?

But why there has been margin expansion in last 2 odd years. Sales is growing but very slow, so scale effect is ruled out. 3M products are varied so rawmaterial should also be varied. Can’t assume all raw material cost came down. So what’s the reason of margin expansion? Is this an exception or its sustainable or can be bettered?