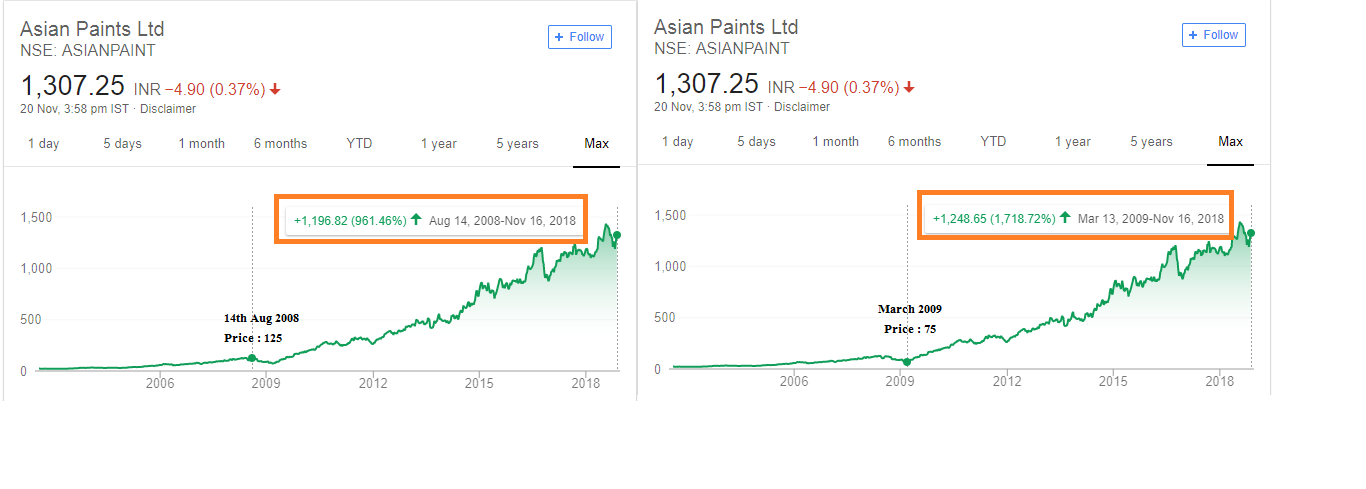

That is not at all correct. Entry point always matter no matter how long the horizon is ! In fact , in longer term , the returns are far more superior when you enter at low Price. Also the dividend Yield every year makes a good impact too ! See below the comparison of Returns of Asian Paints when one entered at different Prices. Though entering at bottom Prices is a different Matter. The only good thing about having these stocks is that they protect your Capital over the long term and creates a decent wealth.

This is the best advice one can give and clearly it comes from the experience @hitesh2710 Sir has had. Market always throws good opportunities at different different times. It is better to make a list of stocks along with comfortable prices to enter and sit sideways and wait for those prices to come. Also better to buy these names in SIP if you feel your calculated valuations are difficult to come. Often it happens that when market tumbles and fear takes over , we too become very irrational and fearful. These are the best times to buy the stocks from our list of stocks.

Disc: I am a new investor with less than 1 year of experience so one can simply ignore my views.

Above discussion is spot on…this is the master class of VP forum.

I find selecting quality names is not difficult now-a-days. May be I sound bit arrogant with my little experience but even a novice reading VP blogs, MOSL reports, Using screener , host of free analysis websites, even looking at top 10 holdings of good MF will help in making a Watch list of top quality large & midcap. However challenge is to set a buying range (e.g. Asian Paints : 1100-1200) and acting upon timely. Now valuation is not an easy job and is seldom accurate if done with half baked knowledge. What do you suggest instead- pls share your views and add options if necessary.

Methods List below:

Speculative interest on lower side( earnings growth>price growth)

Lower than 52 week high > 30%

PE lower than latest high

PE nearing 10 yr avg PE

Also suggest which website/ App (FREE !!) has best alert for buying/selling. I prefer email & sms both.

N.B. Identifying hidden gems/ future leaders/excellent micro caps is not part of this post and IMHO, is most difficult and I don’t have skill set as of now to comment.

If you are talking about Asian Paints in particular, then I would classify it as an Index Scrip. By that I mean that the company is in open public light; none of its aspects are undiscovered by the market participants.

In other words all of its goodness, its excellent management, market growth, leadership position, future prospects everything and the current Euphoria of the general stock market has been factored into the CMP, leaving us with no edge to exploit.

Our advantage as investors is to buy when the company is facing a temporary hiccup, and weak hands have decided to fold. This gives a nice drag to the price. Even better would be, if this happens when the general Euphoria in the market has receded, which is when Nifty PE < 22. Then, the investor would have enough advantage and reason to invest in Index Scrips. Afterall, one must get Risk-Adjusted-Returns.

(The excel I posted follows both these aspects.The EPS growth and Speculative growth.)

Furthermore, I have settled on a belief that for Index Scrips if Nifty PE is anywhere above 20 (or 22) then it may not be cheap anymore. Above PE 25 is definitely expensive, which is where I would stop doing SIP.

If I must chose one out of the multiple choice you’ve given, I’d say 4.

You have selected good set of companies. Your initial list and modified list is fine though there is always room for improvement

1 year, 3 years and even 5 years is less time period to judge one’s portfolio. For longer period you can see good price appreciation on your current portfolio.

Time, reading, analysis will teach you experience and you can go ahead with allocation / portfolio mix accordingly. I just want to say that you are doing good. Inactivity or taking less actions is also good thing in stock market.

PE is not the only way to look at investing but since its very east to relate to comparable valuations, its become popular. And its almost always available at the punch of a button these days.

If we are looking at quality companies for the really long run it makes sense to focus on a few things.

Opportunity size. How big is the opportunity for the company to grow and for how long. (how long is the runway for growth.)

Scalability. If the opportunity size is huge then how competent is the company to scale the business and what kind of hurdles it faces to scale.

Business quality. It can be gauged by past track record. Whether growth is sustainable, predictable and prone to hiccups,disruptions and so on and so forth. Good quality businesses will have very good returns on capital ratios over long periods of time and would have very good cash flows and free cash flows. And these businesses would have grown over the years without too much stretching of balance sheets.

Management quality. This is often tricky and there is a lot of subjectivity involved. But some tell tale signs are walking the talk and delivering on promises made in annual reports and concalls, rewarding minority shareholders, absence of signs of pilfering and petty things etc. Another sign is to see how the management has steered the company during troubled times.

Valuation should come in last during the investment process. e.g in case of 3M. Its a high quality company as is evident from the track record. Besides this, the parent has a lot of innovative products in its basket which it can keep on introducing to Indian markets as and when they feel the Indian markets are ready for them. So for them the runway is quite long. These are portfolio kind of bets which one can keep on adding during market falls and remain invested for long term without bothering too much about valuations as they often change from time to time depending upon market moods.

More than investing, I am amazed at your writing skills. To explain ambiguous, contradicting and complex things like investing in plain English is indeed an art. I am sure it comes from clarity of thought and experience. No doubt your posts are so closely watched by all. Thanks Hitesh Ji👌

3M has shown phenominal margin expansion. Since this year was roughly the peak, I was bit skeptical of further margin expansion. Since the sales growth is 11% , the profit growth may revert to under 15% from next year - thats my guess. But this is a classic case of a business improving on all efficiency metrics. This is worth adding to my portfolio , but during good corrections only I feel

@hitesh2710 bhai, Peter Lynch himself couldn’t have explained this so succinctly ,

Coming to 3M India Ltd, it ticks all the right boxes. But wish to have your views on the valuation part of such companies. At a PE of 65, Mkt Cap to Sales of ~ 10, Sales growth of 10-12%, isn’t 3M India trading at exorbitantly rich valuations? Similar is the case with some of the well known FMCG names. How to value these companies? How much is too much in such situations?

It is real growth after inflation. A 8% fixed deposit in India is same as 2% term deposit in US in real terms as the real return after inflation is the same.

Hi there, will share my POV.

The very basic of investing is buying an underlying business cheap.

Justifying a crazy valuation is vague. Many have said what runaway a company has?

It is very difficult to know how long a company can grow, it is a constant review process. No1 would know it in the begining. Hence too long a projection shall best be avoided, few years would make much sense. But even for that one would do a good diligent study.

Assumptions as such are dangerous.

Fall from ATH is also vague parameter and hold no value.

Investing cannot be just based on bigger fool theory.

Hence when a premium in price is paid for a business one would try to analyse what virtue and advantage a business holds for such valuations?

Wish you good investing journey.

Your POV is well taken.

What market thinks and how it values such high quality companies is indeed vague. I think beyond sales and profit cagr, there is something which drives valuation. May be not in financial models but in thoughts and hopes. I agree this will sound like mere justification…

Market assumptions in my view.

Market believes 3M with 30 years history in india can grow steadily for may be next 30 years.

They can invest 5% of revenue in R&D and come up with game changing products.

With only China and India as growth subsidiaries, may be they acquire companies and grow inorganic. Walmart flip kart kind off…

Command pricing premium and ride inflation led growth for a long time

Also, often in business after sustained period of lull, opportunities arise out of nowhere and all of a sudden. Big companies can capitalise on them, when conditions are favourable. Ex. Ola/uber boom driving swift dezire and waganor sales up.

Size and brand also gives these flexibilities which can’t be captured in an excel sheet.

I am interested but can’t make up my mind… Perennial problem of a confused mind

I have always been amazed by the mindset people have while paying 60x kind of valuation. It becomes even more confusing for me when company has growth rate of 10-12%. Rather than operating fancy financial models, if I run a simple calculation assuming company keeps on growing its profits by 15% every year and I pay 65x of profits as on date, it will take around 17 years for me to get back all my money (in terms of net profits, taking a simple assumption of PAT= cash flows while i fully understand there will be depreciation and other stuff but for sake of simplicity, I assume depreciation equal to capex in longer term). Now this is the time i will need to get plain cash assuming 100% of cash flows are paid back to me. However if i factor in the opportunity cost since I can park the cash in a FD at the same time and assume 7% interest rate for so many years, I will need around 27.5 years to get my money back. Isn’t it too long a period and that too filled with significant uncertainties of world and business. Same goes for companies like Page Industries, HUL, Britannia etc. although their rate of growth may be bit high in high teens or early 20s resulting in lower payback period (as profits not the capital). Just to clarify, I am talking about mature businesses and not turnaround stories or fast growing companies showing yoy growth of above 25%yoy

Some of us are unsure about whether in near term returns will be satisfactory, if invested at 65PE. As a solution waiting for correction to 45PE level seems logical. Some debate that 45PE may never happen. Yet that seems to be the only logical thing to do.

Even the strongest proponent of Page Industries has chosen to shy away from investing in it at these lofty multiples.

For the advocates of valuation with PE as benchmark,please watch this interview of Mr Bharat Shah- my favorite investment guru and an industry veteran.

PE as per him is one of the most deficient way of judging valuation.Hear him at 10:50 minute.

Global giants like 3M will not succeed in india unless they make india specific products. The dna of these companies makes them innovate and create local products…3M has done it and keeps doing it…con agra aspires to do it…etc etc

We can now certainly say 3M is great company in indian context also…i wonder what vision great investors like mr damani had when he bought huge quantities of 3M years before probably then even flagship products of 3m india were either not present or insignificant…if anyone understands their thought process pls let us know. Thanks

,

,