Portfolio is stellar and it will do really well over a long period of time. However, I wish you would trim some names and bring the number of stocks under 17…

All the best

Portfolio is stellar and it will do really well over a long period of time. However, I wish you would trim some names and bring the number of stocks under 17…

All the best

I have abbott in my portfolio wanted to know your view about its valuation is it justified to give such a high pe because a high pe stock is benifical only if there is comfort in his topline for next 3 -4 years i understand they are planing to launch 100 new api but wanted to check your thesis

My thesis is same as yours. New launch or new introduction of battery of new products, less dependence on US FDA norms and being an MNC are plausible reasons for high PE.

I dont know which ones to sell. Should I sell the losers or the winners. Todays loser becomes tomorrow’s winner and vice versa.

I read somewhere, selling is an art of investing and is more difficult than stock picking

This is what warren told to Peter lynch

Selling your winners and holding your losers is like cutting the flowers and watering the weeds

Actually, no. Peter Lynch first used this sentence in his book. Warren Buffett called Peter Lynch (That was the very first time Buffett talked to Lynch) to ask his permission to use his quote in his speeches or Annual Letters.

Correct…but what my intention is never sell your winners and lap onto the losers in PF…

This is what happened next when

Lynch said he mistakenly sold his stocks in Home Depot and Dunkin’ Donuts too early because they would have soon grown over fiftyfold.

When and which businesses/stocks to sell:

Selling is 10 times more difficult than buying!!!

@kush.pawan

Distilled wisdom,in those 4 points regarding selling parameters.

To the wealth of wisdom in this thread,let me add my mite.

Point no.3 about reduced growth prospects due to increased competition, Page Industries is at stratospheric valuations,and has not belied investor expectations,so far.

But the entry of Under Armour,into Indian markets,may challenge the dominance of Page,though it remains to be seen if they get their entry strategy right,and not join the ranks of those MNCs who failed to understand the Indian consumer. Entry price points and perceived value propositions for the price-conscious Indian consumer, have proved to be quagmires for those who failed to do so.

A retail investor does not have to behave like a fund manager and that is his advantage. A fund manager cannot choose to disinvest 50% or 80% of the funds under his management and force the investors to take the disbursement. Simply because that money will go to other funds. Their objectives are different than ours.

This is retail investors Prime advantage. It is a risk. But, currently odds are in favour, given the current situation.

Therefore, i would recommend phasing out entire PF as and when the current bull market gives a spike in individual scrips. And diverting that capital to Gold Bees and corporate bonds yielding 10%ish, which VPiers can guide with.

I don’t believe Under Armour is direct competition for Jokey, they are into high performance shoes and sportswear (just that thy carry some sports undergarments)

Asian paints growing at 25% And dividend yield of 2-3%? I don’t know in which alternate universe it is happening. How can a stock going at 60 PE give a dividend yield of 2% leave alone 3%? I have owned Asian Paints till last Friday and will own it in the future too. But I know it is not growing anywhere near 25%.

Asian Sales growth is not 25%, but around 15%. Then the question remains, why Is the market paying 60PE for Asian?

I think, one factor is that a bulk of the money chases certainty as fund managers need to show annual performance. Their job is even more tough now as the markets have too much liquidity lately, Mcap to GDP ratio is a good measure of that.

Putting both the factors together, there is massive money chasing stocks that display certainty, which is why 50% of the [growth in Nifty 50, in the recent times, had come from growth in mcap of only 3 stocks] (https://www.google.com/amp/s/www.livemint.com/Money/pXYezxo5piGz9IEcWdJjpL/Only-3-stocks-responsible-for-over-50-of-the-rise-in-Nifty.html%3Ffacet=amp)

Should there be a hiccup in the company, or the country or it’s economy, or something global, and suddenly either the excess liquidity is squeezed or economic prospects appear hampered, then this money which is only after certainty will park itself in stocks and bonds. This is the nature of this money, to chase certainty.

I think, a retail investor has an advantage here. He isn’t under annual performance pressure, he should give up the need to see certainty in the current fiscal. So, he could pick his stocks that are available at reasonable PEs due to near term slack, but long term prospects are good and intact beyond any reasonable doubt.

In his attempt to seek out value, the investor must have a very strong sense of:

A. The amount of risk he is comfortable with. If you can’t wait beyond two years, then don’t but mid or small caps.

B. Have a reality check in your stock picking skills

Pharma Auto Cement stocks are currently soft. Hence Risk reward ratio is better. Instead of paying 60PE for 15% growth (Asian). I’d happily pay 18PE for 10% growth (ACC Or Herohonda or Cadilla).

How do you know the company is a great company. If this is the case everyone would be investing in the same. I guess best way of investing is to find bargains and those comes only in the bear market. So wait patiently for overall downtrend rather investing in all seasons. Also i believe there is no point in making 5-6% gains. Try for big gains which diversification can’t give. It would require you concentrated bets in special situations. So no point in investing all the time in market.

After 6 months of relative inactivity, I am again trying to look at below stocks cautiously… Thinking of allocating 3 % of portfolio to each if at all i decide to buy.

Hawkins

Accelya Kale

VIP industries

Atul Auto

Look forward to your views and opinions on quality and safety and future growth as these are not big companies.

of course its your decision and I am no one to ask but just out of curiosity why direct stocks and why not MF , if investing for the first one

Yeah agree with the view.

If we are adding more than 10 (max 15) stocks in our portfolio, MF is a better option.

MF has large no of stocks to diversify, reduce risk and volatility and may be compliance. Also MF shows NAV which though looks one number but is weighted average of many scrip prices. MF manager frequently buys and sells as well.

Now I don’t intend to do any of these myself. However, as I don’t sell, rather not selling, so every buy is making the portfolio become bigger. What could be an option is buy more of existing names, which also causes FOMO on other stocks.

The clarity of thought or strategy is clearly missing that’s why my approach looks like mimicing a MF, though I don’t intend to do so.

N. B. Beyond my portfolio I do buy MF in lumpsum approach and treat NAV as a individual stock. Whenever index corrects by say 10% or more, I put lumpsum.

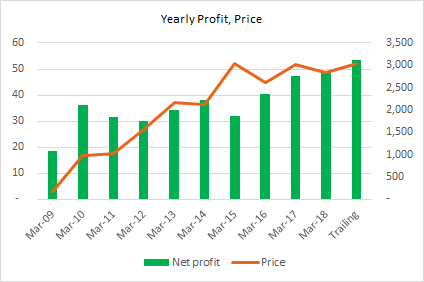

Since 2015, profit has doubled and share price is same. So approx PE has halved. However, profit has been growing consistently.At 30 PE, it looks ok valuation wise.