This initiative is really appreciated dumboinvestor. In certain cases, handholding may required for new investors specifically who hasn’t seen the 2008 / 2009 carnage or who are new to the market. The above is a general comment and not intended against homemaker. In fact, I really appreciate her learning process as we are all here to learn.

I just wanted to add that all these stocks / picks suggested by dumboinvestor are solid names with strong parentage. When an investor is putting his / her hard earned money, just pause for a moment and try to think like a private equity guy what would one get by putting the money into this company. As we are not private equity guys, we can’t forsee 5x - 10x kind of return or cannot undertake all the rigorous risk factors they would consider; but if your investment can guarantee sound sleep at night, that should be enough for an individual investor / shareholder. Another test would be to make sure that whoever runs the business of the company you hold, still the business would do well.

While there are 15 stocks, depending upon the risk profile, one can invest in 6 / 8 / 10 most high conviction stocks. I would say the key is to select the most conviction stocks based on one’s analysis / circle of competence (no need to put money in all these 15 names unless you want a fairly diversified portfolio with 15 stocks). One can also take a few bets in small / midcaps stocks which could do extremely well. This is the approach I am following for the past few years in the market. See the returns Vinati Organics has generated in the last 3 years (whopping 333%…!) So, in hindsight all looks fine and if one can’t find such kind of names early, just SIP in names from the above list.

Coming specifically to the stocks, majority of them are really sound names which would qualify for ‘buy and hold’ at least for the next 10 years. Personally, I would disagree on one name, i.e. Ashok Leyland. I won’t invest in Ashok Leyland but would consider names such as Kotak Bank if one wants more weightage in financials or Bata in the consumption space (probably not at this price level but after a meaningful correction) or may look into Honeywell Automation, the Indian subsidiary of NASDAQ listed Honeywell International.

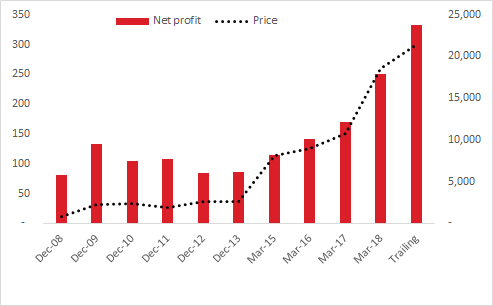

We are all familiar with Kotak bank and the returns it has generated over the decades. Also note that the AMC / broking business are not listed at the moment. Uday Kotak is under pressure to reduce his stake in Kotak bank and this could be an overhang at the moment. Otherwise, it looks solid as a rock. Similarly, there is no need for an introduction on Bata, how they changed themselves and become the leading player. See the products they have recently launched in women wear / athleisure. See how they are protecting the customer base and pricing strategy thus not losing to Sketchers (whose products are known for comfort at a higher price band). Regarding Honeywell, I came across a few articles and based on my quick look, it looks like a solid bet with good parentage. Note that Honeywell US has been in business for more than 100 years and if Honeywell India can provide all the technologies / products of the parent in India, then that would be fantastic. As I am not techie nor an engineer, slowly grasping the business at the moment. Anybody, who has looked into Honeywell or whoever has the circle of competence into Honeywell’s business, please share your thoughts.

Interview by Honeywell India, MD in 2018

Disclosure - Holds a few stocks from the above list. Also, I am conscious of the fact that Ashok Leyland might have been included in the list by dumboinvestor just because Homemaker currently holds it.