Thanks Niraj.Let’s hope there are no governance issues.

Finally, an acquisition. 80 cr spent.

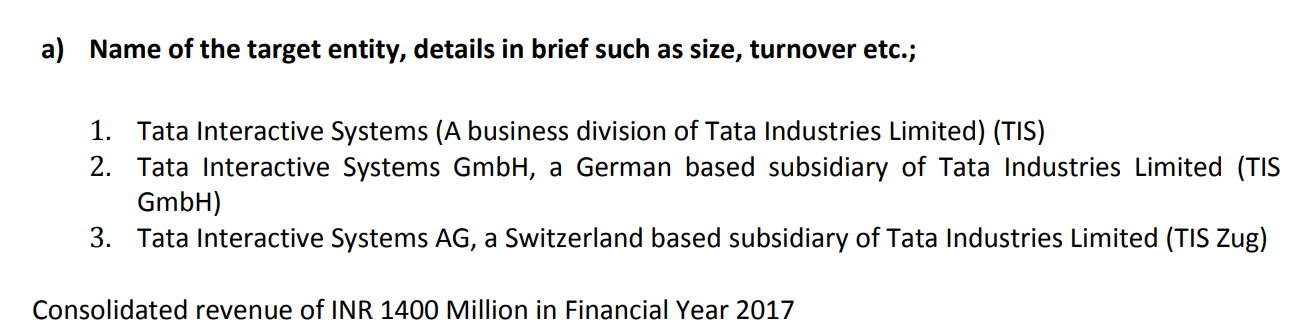

Financial of Acquired Entity :

Notes :

(1) Aquired entity’s margin profile seems to be lower than MPS…Max improvement upto 12-14 % EBITDA margin might be possible not more than that.

(2) Revenue cut might not be that significant.

(3) Its again a stable cash generating acquisition which seems to be a preference of the management.

(4) In absence of growth and focus in core high margin business, such low margin acquisitions might in the long run bring consolidated EBITDA margin to 20-24 %.

(5) Management seems to be moving towards the path of making MPS a Holding company of stable cash generating interesting businesses which, although is clearly not stated today, but might get clear few years down the line.

Rgds.

Discl. - Small Holding.

6 Likes

Thx for your views.

On what basis do you say margin can go up to max 12-14%?

Based on historical margins at which acquired entity has operated even in best of its times.

1 Like

Like in case of McMillan it may not be an unreasonable assumption that the acquired Tata Company also has quite a bit of flab which can be cut and margins can be improved. Of course it will depend on how the acquisition is handled.

1 Like

Ok…don’t you think a Tata company, culturally, will have a lot of flab and, therefore, far higher scope for margin improvement…Tata is a better pay master plus attracts better talent which is costly in the first place…so double scope to reduce cost in the medium term  Then the overall mindset of MPS of cost reduction compared to Tata’s which really never would have any reason to cut costs in a business where the mandate would have been to focus on building the biz. So, my sense is that margins can even double in 2-3 yrs as MPS wud run a very tight ship. My concern however is on MPS moving towards “enterprise sales” where they hv no experience and they anyway never appeared to be great in selling, besides, enterprise selling is far tougher and more competitive…so they cud struggle in this business in the short to medium term…so, overall, this deal does open up a far bigger oppty for MPS to grow than they ever had before…but their perf on growing sales more than improving margins, wud be watched closely over next 1-yr.

Then the overall mindset of MPS of cost reduction compared to Tata’s which really never would have any reason to cut costs in a business where the mandate would have been to focus on building the biz. So, my sense is that margins can even double in 2-3 yrs as MPS wud run a very tight ship. My concern however is on MPS moving towards “enterprise sales” where they hv no experience and they anyway never appeared to be great in selling, besides, enterprise selling is far tougher and more competitive…so they cud struggle in this business in the short to medium term…so, overall, this deal does open up a far bigger oppty for MPS to grow than they ever had before…but their perf on growing sales more than improving margins, wud be watched closely over next 1-yr.

Rgds

RR

Disc: invested…small position

Whereas possibility of that happening always remains but why I feel such a drastic improvement in margins might not happen in Tara Interactive Systems case is because :

-

If we closely observe past financials and annual reports, TIS was not a bad run company under Tata’s fold.

-

There was also no misadventure on part of management as was in macmillan case. We need to note here that in case of macmillan what new management of MPS did was corrected the misadventure and brought back margin level to historical normal. In TIS case historical normal itself is low.

-

TIS seems to have mainly suffered because of real operating business dynamics and not by mismanagement of available resources.

These are my personal assumptions based on how I see and interpret TIS historical records and I can be wrong.

Rgds.

1 Like

MPS’ strategy is always to move a bulk of the work to its back-office. So in all probability, they will retain the key people at TIS and rest of them will be gradually let go with a severance package. Expect some expenditures on that account in the coming quarters, which happened with MagPlus as well. Overall, I think management will have gone into this with the mindset of getting close to MPS margins eventually. Eventually could take up to a year I feel.

I do not think they would go for an acquisition which has significantly lower scope for peak margins (based on their model). The management has never seemed shy of keeping cash for the right opportunity (which they themselves define as something that can deliver MPS margins with some restructuring) and it would be pre-mature to believe they have made an acquisition out of desperation.

More will be revealed in the next concall, which should be soon.

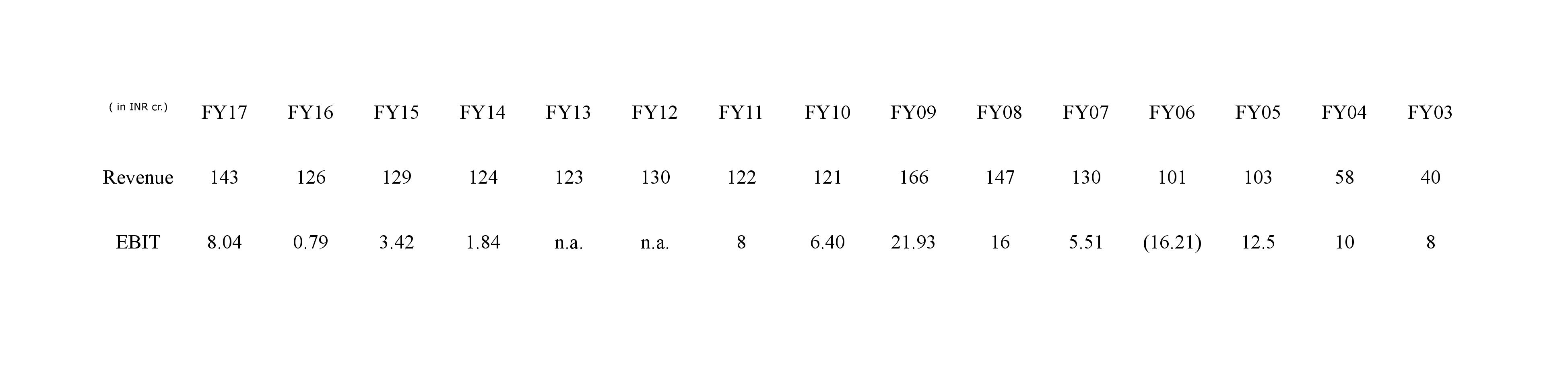

It is always better to look at productivity rather than only payscale when we compare two M&A companies – TIS is already at around INR 1.8 mn. revenue per employee level v/s MPS’s current (improved) INR 1.1 mn. revenue per employee level and Macmillan’s traditional (before acquisition) INR 0.7 mn. revenue per employee level. Hence, to think of cutting employee size at such a good productivity level might not be a right strategy as business is not similar to what Macmillan’s business was. Also, if goal of MPS is to retain TIS’s current positioning in the segment as well as retain Fortune 500 clientle, again attracting cheap talent is never a good idea. TIS, much like Magplus, is a prominent player in its space and senior management of MPS led by Mr. Aroras might not be right persons to drastically change the model and strategy of the company.

This is not an act of desperation…Not atall…instead, this seems to be a well thought out strategy of the management and in future too this might continue…Management led by Mr. Nishith Arora seems to be on lookout for businesses who enjoy good positioning in their respective segment and are profitable but might not be scalable (as scalability might require further investments and possibility of burning of cash which MPS management might not be interested in)…MPS seems to be listed vehicle to channelise such investments wherein it will benefit from steady cash that will get generated out of such businesses…However, what we thought in the beginning and what Mr. Arora used to tell regarding acquisitions in his forte so that steadystate EBITDA could be achieved at 30-32 % + — this seems to be difficult to achieve — if Mr. Arora can again achieve it even outside his forte it will be a great feat.

Rgds.

1 Like

Great discussion. Thanks Mahesh,SSRN et al for some good points. One point that I think should perhaps merit discussion as well is the acquisition cost. 80crs for an average(last 7 yrs) EBIT of approx 2 crores seems excessive. You would recall previous concalls where Mr. Rahul said that they are aiming for an acquisition cost of 3-5 times EBIT. Not sure what the book value of the company is but notwithstanding that it still looks high especially by MPS standards which believes in buying things dirt cheap. This time perhaps they have been outsmarted by the Tatas.

Discl; Large holding

1 Like

Your logic is actually quite good. However, I would say the following:

-

MPS made some senior US hires last year in the education space. They might have some ready customers for the products in the US, which may help improve profitability significantly if there is operating leverage.

-

TIS may have unprofitable contracts, or R&D spend, or possibly not enough expertise in the domain to truly leverage their products - MPS may see an opportunity to use its connects and experience to leverage the products quickly and/or shut down non-profitable ones and cut R&D expenditure not giving returns.

-

Going forward from point 2 above, being a Tata company, TIS may be having ‘unhealthy’ revenue that can be removed. So maybe we should take the 140 cr number with a pinch of salt, it could very well be 80 cr with 3-4x the PAT.

All this is still in the realm of conjecture, though. It will depend on what MPS thought and how it will actually pan out.

1 Like

Tata generally has top tier client base, so a definite opportunity to cross sell existing offerings. The benefit should show in long term.

Attached below is the link to emkay’s event update on the company :

what is the effect of

the final deal inked that MPS Ltd will acquire Tata Interactive Systems

source

http://equitybulls.com/admin/news2006/news_det.asp?id=226420

What i can understand from equity raise by other cos in e-Learning is that

- There is good interest in the space by PE and VC investors

- Bringing down cost of education is a serious focus for many govts across

the world, and - that can be done only by technology

Overall, i am positive of this acquisition by MPS. The management is

serious task masters in cutting costs and razor focussed on bottomline

growth.

Vetri

2 Likes

What the chart is saying is that it made a double top at 680. If it gives a break out then it will give a BUY signal. If that happens then the next levels can be 760-780-820. However, this is not my recommendation. Please do your own research.

1 Like

What i like about the management is that in the 2 years they were holding the QIP proceeds without investing, in all the concalls they were very clear that they do not want to acquire just because they have money in their pockets and that they are very focussed that any potential asset should have strong long term potential and a reasonable price.

Given that most companies function on a Q to Q short term outlook, this is a very refreshing attitude.

While I do not expect the stock to give great returns anytime soon, i feel this is a good niche business with high margins and good RoCE and limited chance of competition, the kind i would be comfortable holding for the long term even if as Buffet says markets shut down for a year. Someday it will get discovered and get the valuation it deserves.

2 Likes