Excellent sum-up Dhwanil & Hitesh…you both have covered almost the entire concall commentary very well…just few corrections as per my understanding of the commentary :

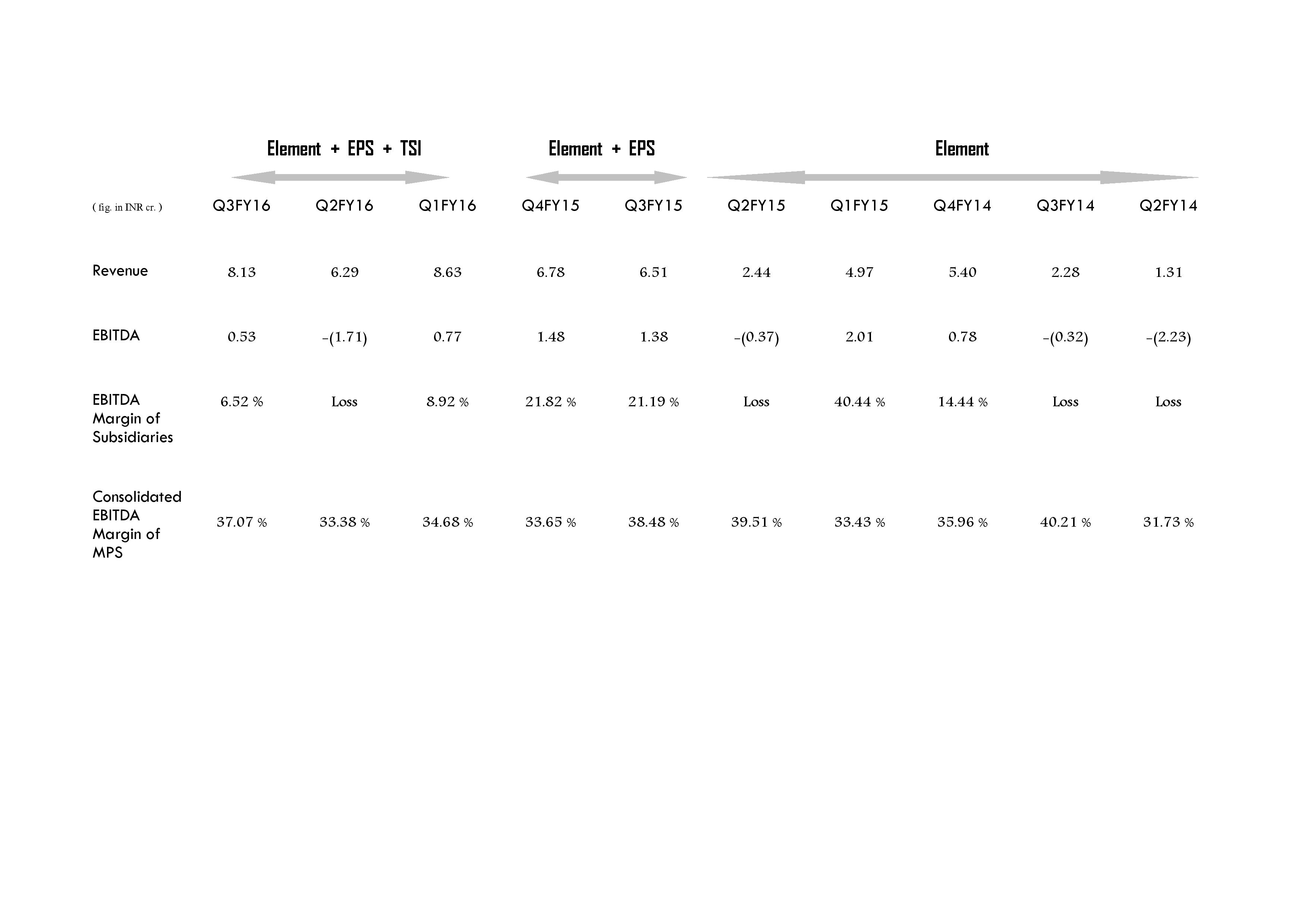

(1) In addition to consolidating all three acquired entities under MPS-NA, what they have done is consolidated Element & TSI under K12 division because of which it was difficult to provide separate revenue figure of TSI.

(2) Although management was confident of good Q4, but as usual they refused to commit whether Q4 will be bigger than Q3 so whether historical trend of Q3 being seasonally the best quarter will remain or not that is unclear.

Now, some observations :

I continue to maintain that Disconnects remain and continue to widen even post Q3 results & concall commentary…Before mentioning anything want to state it clearly that management seems genuine and ethical – and I repeat, ‘Genuine & Ethical’ but it seems that they are unable to admit certain things because of market and business dynamics…but as an investor, when numbers don’t matchup for stated things I need to be cautious as one more bad quarter could raise extreme caution, in general, amongst investor community for the company.

Explanation for muted Q3 – Likely Better Q4 ??? – A look at the history :

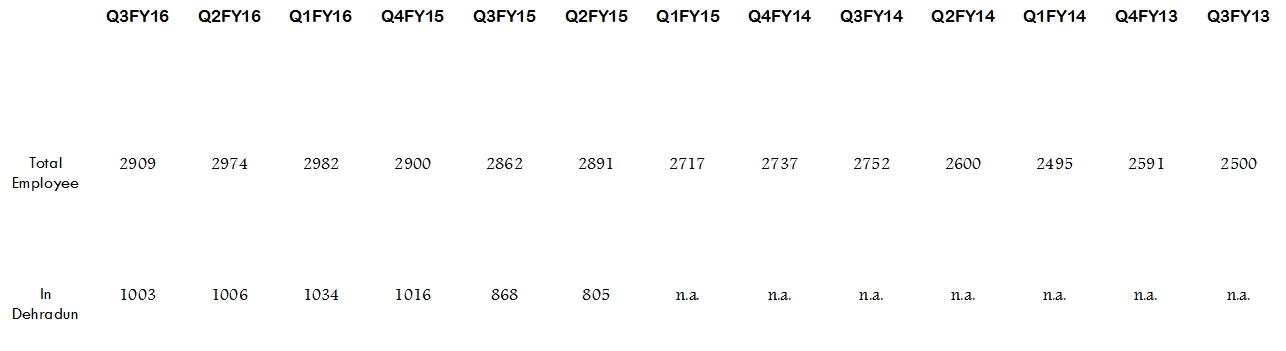

Those who are following MPS story closely and have heard management since the time Mr. Arora acquired MPS must be aware of all the initial management commentaries where Mr. Nishith took pain in explaining in detail why Q3 is the biggest quarter for the company as well as industry (even under Macmillan it seems Q3 was the biggest amongst all 4 quarters for the current acquired business). Now, management is right in its saying that if there is more project-based revenues or content-creation projects, revenues might be lumpy and may be booked more in one quarter than other. But, for significant project based revenues which are expected to be booked in next quarter, normally employee bench is created. Let’s see the total employee trend over last many quarters for MPS :

As can be seen, total employees have infact decreased from the level of 2982 in Q1FY16 to 2974 in Q2FY16 and further to 2909 in Q3FY16.

Another important notable thing is, for the first time post acquisition of MPS by Mr. Arora, Dehradun has seen layoffs or atleast stagnation in employee count for two subsequent quarters.

Counter argument to this could be project-based revenues or content-creation projects might be more onsite than offshore, but, in absolute terms atleast some addition should be visible in employee count which is missing.

An answer to this could be TSI employees – 15 odd that they have taken on rolls – but, do they have capability to generate revenues of almost INR 0.50 cr. per head for one quarter – only time can tell.

Now, lets leave this aside for the moment and look at last year’s Q3, that is Q3FY15…

Those who were present in Q3FY15 concall (those who were not present can hear transcript on RB), remember the explanation given by management of then muted quarter --”since Q3FY14 was a big quarter and having higher base so Q3FY15 looks muted”…so this is not the first time management has faltered – consecutive two quarters’ YoY they have shown muted growth and that too with unconvincing explanations…

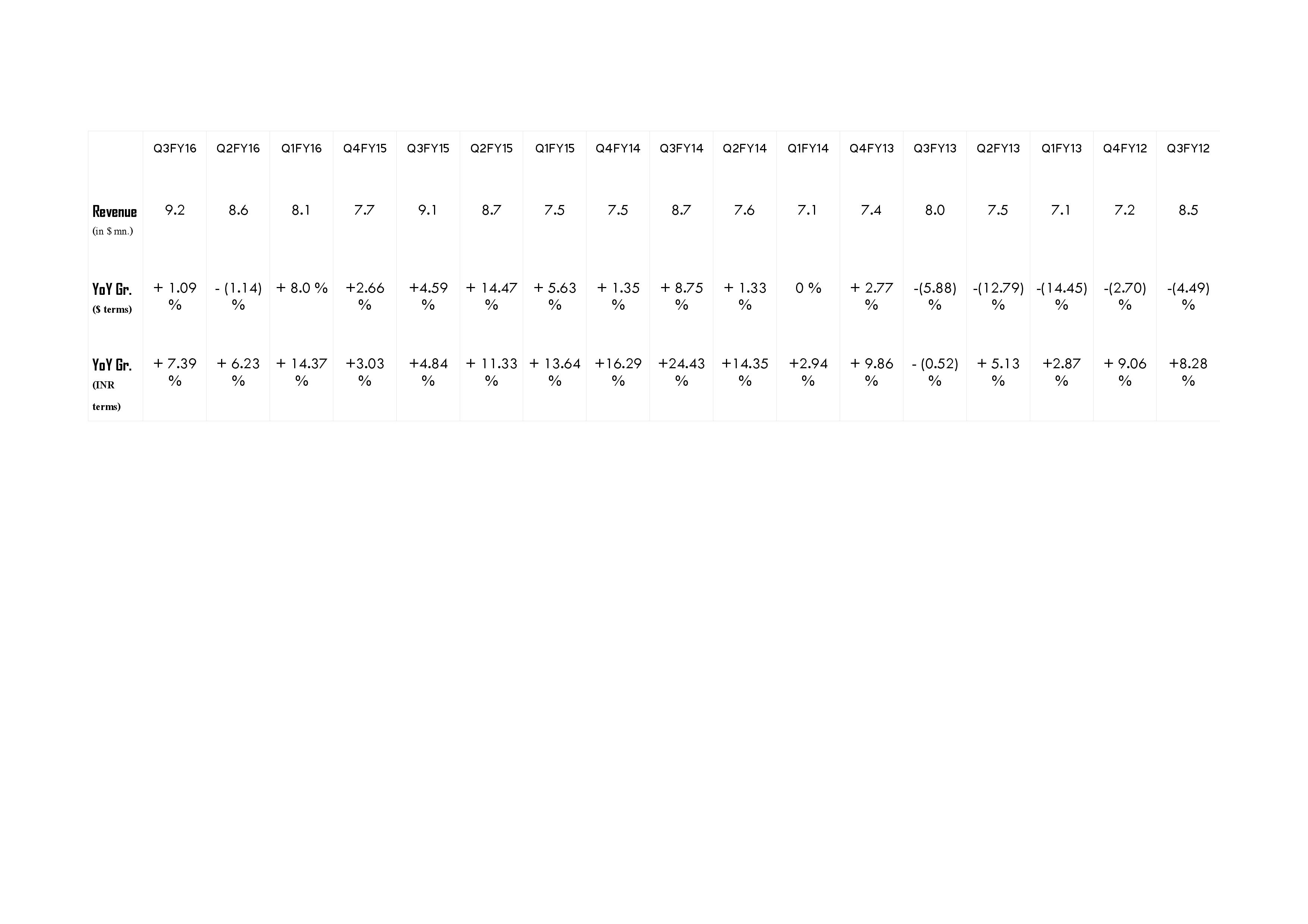

58 % YoY Growth YTD in MPS North America – is it Logical ??

Management has told to look at 58 % YoY growth in MPS North America for 9MFY16 and see it as a very positive sign— in previous 9 months we had only and only Element revenues booked for 6 months and for 3 months we had EPS+Element revenues…Element had a topline of INR 15.09 cr. in first full year of operations under MPS and EPS as management has told had a yearly topline of INR 15 cr. before acquisition and was not bleeding as it was just a selloff by an aged promoter who wanted to retire…

Now, look at current 9MFY16 where we have Element+EPS+TSI revenues booked and that too aided by 6.6 % currency depreciation (9MFY16 USD-INR Average = 64.67 vs 9MFY15 USD-INR Average = 60.66)…So, now let’s do the calculation :

– Element booked yearly 15 cr. revenues under MPS in first year and we will assume nil growth and nil currency impact so effectively negative cc growth even after 10 quarters under MPS,

– EPS booked yearly ~15 cr. revenues before acquisition and was healthy profit making but still we assume here 10 % haircut in topline with no currency benefit which will effectively mean 16 % haircut in topline even after 5 quarters under MPS,

– TSI booked 18 cr. yearly revenues before acquisition but was bleeding so here we will assume 50 % haircut in topline without currency benefit which will effectively mean 56 % haircut in topline…

So, then we should have 15+13.5+9 cr. = 37.5 cr. yearly topline on the most conservative basis for MPS North America without assuming any growth whatsoever i.e. 0 growth…out of 37.5 cr., we have booked 23.05 cr. in 9MFY16 with 14.45 cr. still remaining to be achieved in Q4FY16…

Are we not fair in giving more than 50 % haircut on recently acquired entity TSI and more than 10 % haircut on EPS which has already passed 5 quarters and negative cc growth for Element which has passed already 10 quarters ?? so after such a fair assessment where is the growth visible in MPS North America in 9MFY16 ??

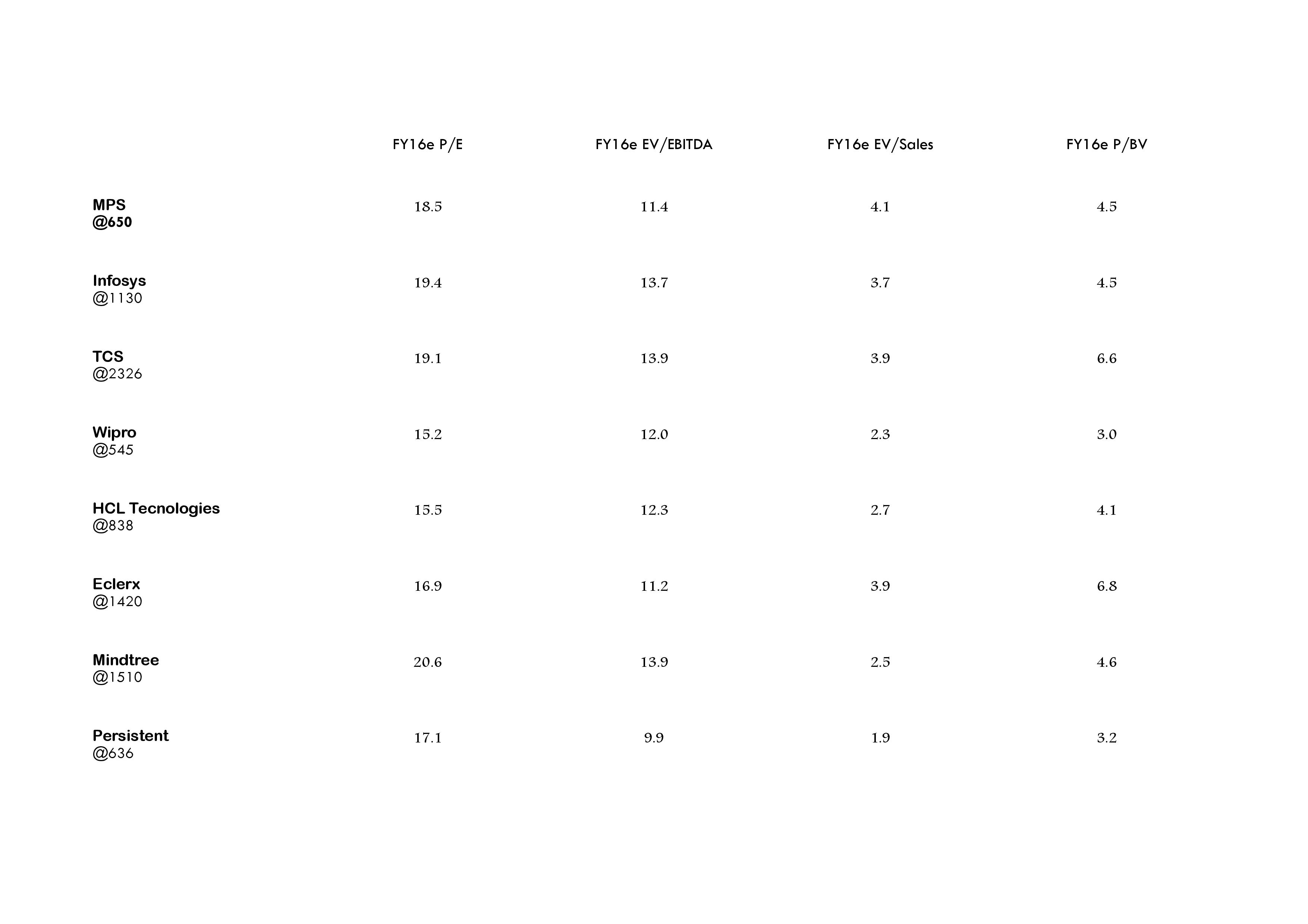

Current Valuations ??

Let’s do a valuation exercise for MPS at CMP of 650 against most established and promising Indian listed IT companies…

As can be seen from the above, at current rate of INR 650 per share, MPS trades at premium on many valuation multiples to even Wipro, HCL Tech, Eclerx & Persistent and almost at par to Infosys, TCS & Mindtree.

Finally, though I want to believe the management but numbers just don’t matchup the talk and when numbers don’t matchup I like to play safe. Q4FY16 or likely acquisition profile will be crucial – faltering on even one of them might not allow MPS to trade at premium or even at par valuation to other IT biggies…this is my personal view and I can be wrong. For the time being high dividend payment might support the valuation.

Discl. - Have Sold to reduce my allocation and looking to sell on every opportunity. Would like to take fresh call post Q4 or Acquisition profile is known even though it might mean reentry at an appreciated rate.

Note – This is not a buy/sell/hold recommendation of any kind and is part of just a general discussion. Discussion is based on available statistics & facts and based on this no Investment/Divestment decision should be made.