Annual report 2015-16 released:

http://moldtekpackaging.com/pdf/Mold-Tek_Packaging_AR_2015-2016.pdf

Discl: Invested

Annual report 2015-16 released:

http://moldtekpackaging.com/pdf/Mold-Tek_Packaging_AR_2015-2016.pdf

Discl: Invested

Any idea why the company continues to pay out such a high portion of profits as dividend, rather than re-investing it in building more IML capacity, especially if they foresee so much growth?

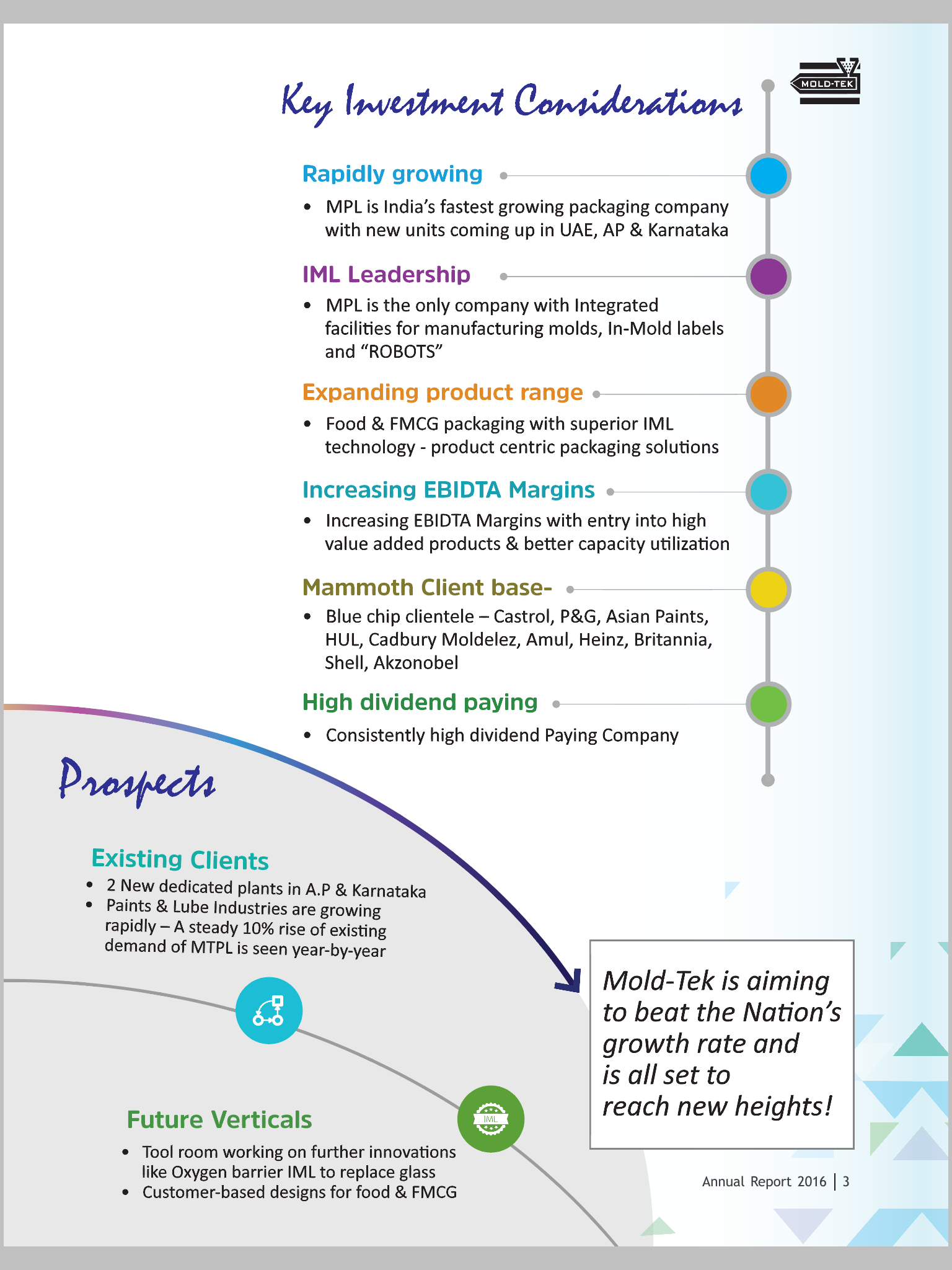

While there are quite a few things to appreciate about the company’s Annual Report for 2015-16, I can’t help but question some of the information highlighted within the first 3 pages itself.

My inferences -

I haven’t come across any other company’s Annual Report with similar Market Cap related milestones (would have been understable for me if it had become a part of any Nifty or Sensex indices) or a whole page dedicated to investment credentials.

Would be really glad to hear from others if they’ve seen similar things shared in any other company’s annual reports.

Disclosure - Invested from 80+ levels (split adjusted) and obviously pretty satisfied with my returns so far and more importantly the business performance. But think this reveals an interesting side of the management.

@gurjota - I feel they might have hired IR team to make annual reports before QIP and retained since then. This seems to be art of IR more than management. Obviously, management could have raised objection and could be have removed this. I have never heard such comments or boasting about share price during the conference calls though as far as I remember.

Discl: Invested (from much lower levels and satisfied with performance of the company so far but this surely raises eyebrows)

thanks gurjot for highlighting

unless there have been some doubtful transactions - we can ignore their bad job on annual reports

Although not related to Mold Teck Packaging, members on this thread might be interested in having a discussion on aseptic packaging technology (Tetrapak). Here is the link to the thread:

According to a report by Systematix Shares, the packaging industry in India stands at US$32bn and is expected to grow at 18% CAGR to reach US$73bn by 2020.

http://www.capitalmarket.com/Cmedit/story50-0.asp?SNo=848178

Disc: Not invested

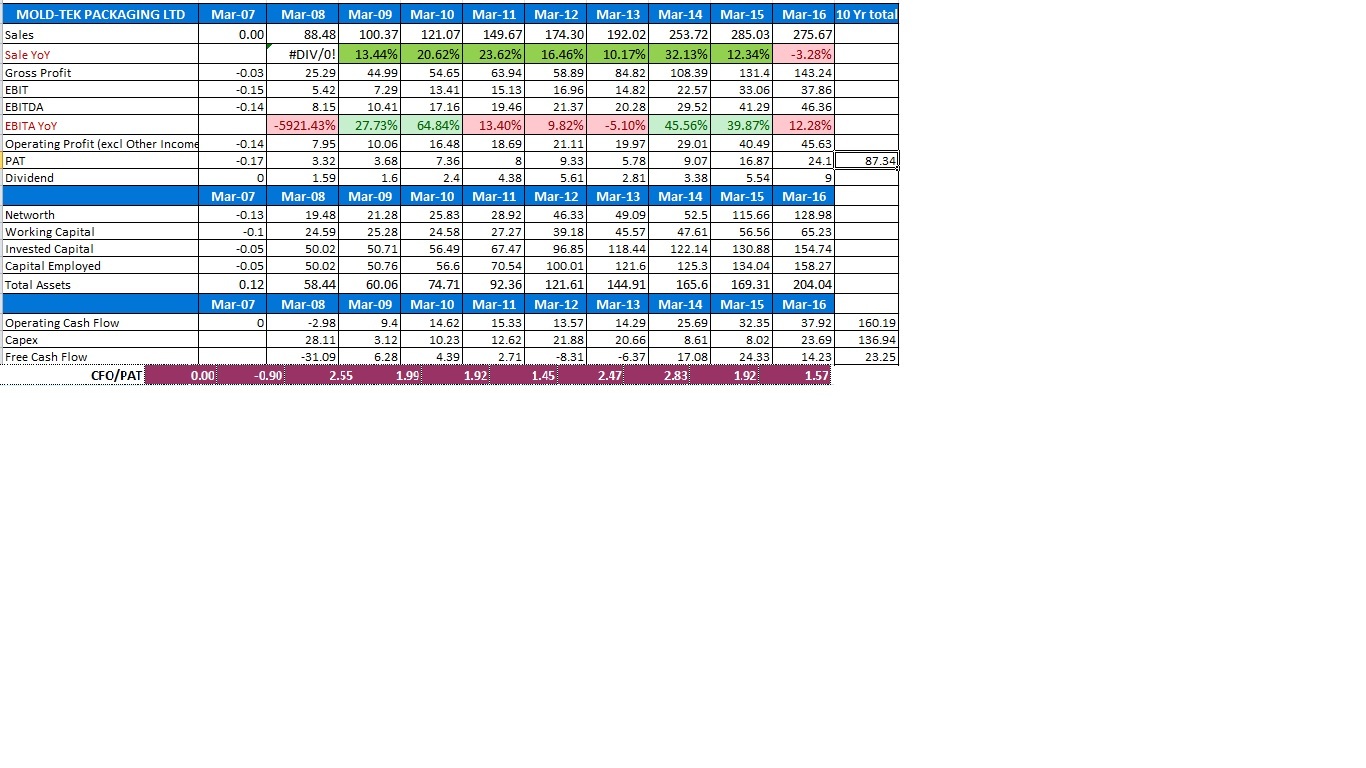

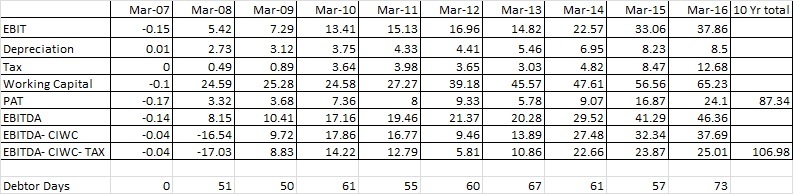

CFO in many cases will be more than PAT as in order to find CFO we need to add depreciation to PBT subtract Working capital change and make adjustments for non cash charges. Finally actual tax paid is subtracted to get CFO. So incase Change in Working capital is less than depreciation, CFO will be more than PAT.

Specifically for Mold tek the company doesnt include tax paid in CFO but include Tax payable as part of CFF. You need to make adjustments to calculate actual CFO.

Thanks @Rokrdude

I tried removing depreciation and Tax but still the number looks big when account receivables increasing.

I came across a nice coverage on the company in Outlook magazine. The link is provided below for the benefit of all. https://www.google.co.in/amp/s/www.outlookbusiness.com/amp/markets/feature/good-things-come-in-small-packages-3514

Moldtec is looking good technically as it is on the verge of multi top breakout with good volume

what is the significance of writing letters to the exchanges with regard to an article ? do they want the share price to increase ?

Does the promoter looking to sell at high prices ?

what are the views after q2 fy 18 results? What I found interesting is company slowly increasing share in FMCG besides paints and lubes. This quarter it has 15% of revenue from fmcg comparing 5% last yr and targeting 20% in coming months. Good performance expected from RAK facility in H2Fy18.

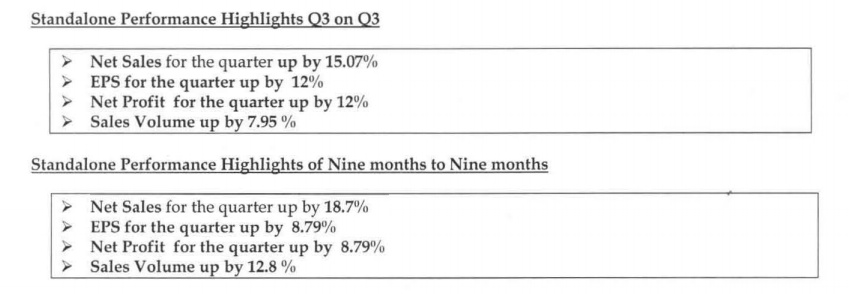

Mold-Tek Packaging Q3 results are good in spite of higher depreciation provision and higher interest outgo due to capex for two plants which are likely to be commissioned this qtr.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b6c4fbbd-7c42-4d1d-82ec-de855c664d1d.pdf

Summary of Concall:

Per KG EBIDTA = 34.09; 9M = 33.86

Depreciation and interest has gone up due to recent capex and expansion

Oil and Ghee packaging doing very well, with 200%+ growth over small base; More orders in pipeline

HUL ice-cream contrainers started from this month + Hatsun also gave order, supply will start soon

Revenue guidance: 20%+ growth in next few years

Last Qtr: Edible Oil 8 Cr sales (vs. 3-4 cr last year)

Orderbook details: HUL is trial order 6 lac container/month (~1Cr sales); Similar for Hatsun + Oil/Ghee…can contribute ~25-330

IML sales contribution ~65%; Food and FMCG sales contribution also picking up (currently ~20% from 13% earlier)

Utilization levels for Ice-cream packs ~30-35%; can easily scale up this year without any further capex addition

RAK UAE were running at 30-35% utilization, few machines moved to Hyderabad plant; Now utilization at RAK ~50%; Can ship more machines if orders don’t pick-up

Total debt on books incl WC loan: LT-10 Cr.; WC-80 Cr. (75% of current assets), used 25 Cr. WC for Capex, interest has been taken out this year itself (WC is cheaper currently)

2nd Phase expansion for Asian paints can happen only after 2021; Currently Vizag and Mysore should be sufficient

May expand edible oil capacity if required, most likely at daman (possibly 8-10 Cr); Potentially a pilot in North for Nerolac (5-8 Cr)

2087 non-IML tonnes; IML-3100 tonnes; RAK-150 Tonnes (quarter)

Mondalez: was drop in Q3 due shift from bigger to smaller packs (30% drop), this might again improve from coming quarters

New orders margins will be in-line with current IML margins; HUL is order is pan-India to supply to all their major plants, Hatsun is for South India plant; Volume will be seasonal tracking ice-cream business

RM prices gets passed on monthly/quartly basis, so this doesn’t impact the company

Don’t see much EBIDTA/Kg margin from herel; can be just minor increase if new orders pick-up

Edible Oil new client NK proteins ~8-10 cr. annual order, can see more pick-up in order (started from December); Discussion with Two more clients

96 Cr breakup: 61.2 Cr IML, 34.7 non-IML

Paints: 44 Cr. (vs. 38); Lubes: 29 Cr. (vs. 28) F&F: 22.8 (vs.16.8)

F&F volume this quarter 920 tonnes (vs. 628 tonnes)

Definitely there is seasonlity: paints and lubes dip in monsoon; Ice-cream dip in winter; Edible oil picks up in marriage season

Top 3 clients F&F: M2K, NK Protein, HUL/Damani

Expecting F&F contribution to 25% next year accomodating Paint growth

Opex: Mysore and Vizag employees already reflected in operating expenses; Yet to add labourers and contractors if capacity ramps-up

Order visibility for few clients (likes of Asian Paints) is ~5 years

Started depreciating new machines in Hyderabad, yet to capitalize Mysore and Vizag machines

NO custom duty payable when machines moved from RAK (10-15 lac transport cost)

Sun Pharma proposal still pending and stuck with mold issue; FOcussing on Edible Oil since it is showing traction

Also in talks with COke and Pepsi

Lubes sales dropped by 7% possibly due to rapid growth last quarter

Interest rates: WC 8.8-9%; TL-10-10.25%

RAK there was no establishment cost; 2 cr. loss due to issues there; Machines have been fully used

RAK: Iranian sanctions were lifted but that didn’t work due to re-imposition of sanction; Economic situation in the region is not so good and resistance to shift to plastic containers

Edible oil guidance ~50-55 Cr next year (vs. ~15 Cr); Ice-cream guidance ~25 cr. including ghee next year (vs. 10-12 cr.); Ghee packs can be done in off-season of Ice-creams

Considering to raise the stake but nothing firm yet; No plans to buyback in immediate future

Spent 52.5 Cr this year for capex; Next year ~8 cr.; This is one of the largest capex in the history of the company

WC cycle stretched due to big clients like HUL but they allow for interest cost to factor in pricing; NOrmalized cycle of ~60 days; No credit given for edible oils, taken in advance due to credibility issues with some companies

Please cross-check the above with actual concall transcript since I might have missed some details or mis-interpreted few points

Disclosure: Invested

This is review of Q1FY19 dated Aug 12, 2018 by Kotak. It is relevant even today except status on RAK plant.

thanks vivek, this is very helpful

Promoters have pledged 11.11% shares.

Pledging is for their personal requirement or for company’s requirement?