what’s their model - is it cost plus or value to customer

do they get revenues from consumables or after sales/AMC

heard from a packaging expert that IML does not work well in FMCG’s - works well only in paints, lubricants or large packs of FMCG -like cadburys high end chocolates. will this change and when will IML come to the mainstream

competitors and their actions in India

professionalization of company - my reference check said mold tek is still driven by lakshman rao and hence constrained by his bandwidth

What is the status of their Dubai plant.

a) Total investment was supposed to be Rs.30 cr. Has there been any change?

b) When will full capex be deployed.

What is the plant wise current capacity IML & Non-IML and what is the % utilisation .

as was said earlier, there are some other companies making IML mold like jyoti plastics. so is mold tek just ahead of the curve and having good time for 2-3 years or does it have a moat that can last long.

2)whats the status of lube. how was it accepted. whats the reaction. will we see the impact of the lube in Q2.

3) how does the management divide time and focus between mold tek plastics and mold tek technology.all the three main promoters are active in both companies. any plans to make one person the main CEO so that he can focus only on plastics without worrying about the technology.

thanks

@ankitgor44 Asian Paints recently announced plans for a new plant in Karnataka - is this likely to adopt IML heavily as indicated by you earlier? What revenues (and timelines thereof) do you foresee?

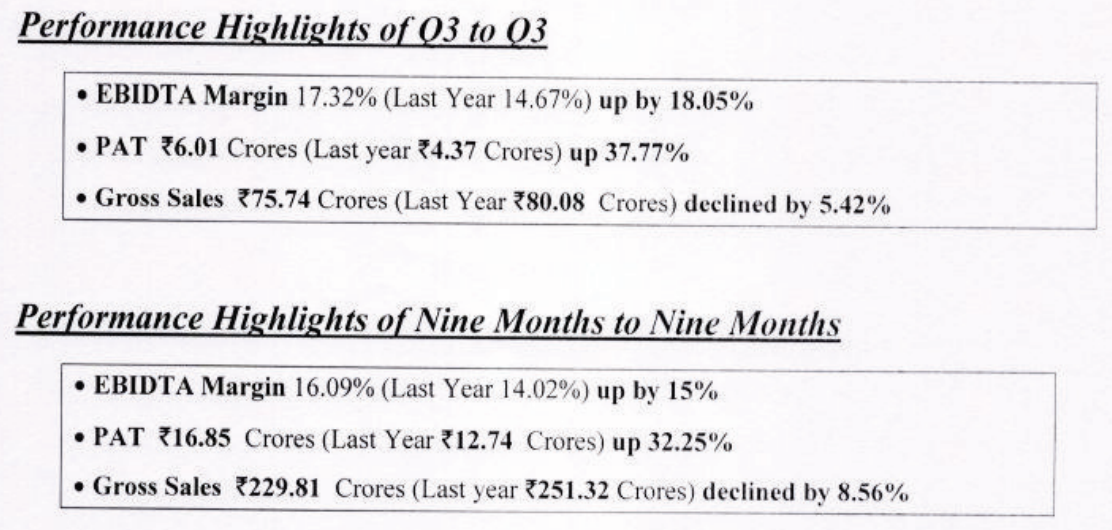

Net Sales: Rs. 638 mm, -19% yoy, -14% qoq Operating Expense: Rs. 538 mn, -21% yoy, -14% qoq. The fall in net sales is due to fall in crude prices which has impacted Poly Propylene, a key raw material.

EBITDA: Rs. 99.5 mn, -10% yoy & qoq. EBITDA margin at 16% in 2QFY16 vs 14% in 1QFY15. Margin expansion was due to higher share of IML products.

IML products share was 40% in this qtr vs 28% in 2QFY15. PAT was at Rs. 51 mn, up 13% yoy and -10% qoq.

1HFY16 results: Net sales: Rs 1375 mn, -13%, EBITDA: Rs. 210 mn, up 2%. EBITDA margin at 15% vs 14% last year, Interest cost at Rs. 6 mn, down 86%. PAT at Rs. 108 mn, up 29%

Mold tek Packaging has received Certificate of Formation & Industrial Licence from RAK Free Trade Zone. Likely to commence productions by May/June 2016.

Also, Kitara India Micro Cap Growth Fund – A Mauritius based Fund (Registered FII) of Kitara Capital purchased 143,478 shares or 1.03% valuing the deal at Rs. 401 lakhs.

Kitara Capital also owns stake in APL Apollo Tubes at 12.8%, Innoventive Industries at 3.14%, Compuage Infocom at 9.36%, Supreme Infrastructure India at 6.42% and Vivimed Labs at 11.29%.

Disc: Invested in the company. Even though Sales are linked to RM prices (mainly crude) and hence likely to go down, margins would continue to see improvement.

I wish they shown some growth in Gross Sales as well. Is current profitability sustainable on back of sales decline and once interest cost reduction is not substantial ?

Yes current profitability is sustainable. The company has no control over price of crude. All crude benefits are passed on (thats a part of their contract). the business model is raw material cost * volume + x (NOT x %). What matters is not rm cost (which is the most sensitive variable to gross revenue), but volume, which is shooting up. I was actually pleasantly surprised by their sales figure, was expecting a much lower number.

Benefits of lower crude -

Lower working cap

Reduced interest expense

higher ebit margin (as x is fixed irrespective of crude prices, long term contract)

IML products become much more competitive than screen printed & blow molded packaging.

The key driver is entry into food packaging. This segment is dominated by blow-moulded bottles that dispense edible oils and other liquids.Mold-Tek (MTP) is an injection-moulded player, whose costs a little higher but quality is way better. They supply high-end printed containers using a technology called In-Mould-Printing or IML. MTP has entered into food packaging through 5 liter and 15 litre pails. Food is a 2000 crs. segment that is a virgin market for MTP, who has more than 25% market share in paints and lubricants packaging. Entry into food packaging more than doubles the addressable market for MTP. Using superior injection moulded products with IML, MTP has already gained entry into smaller edible oil companies and has got trial orders from FMCG edible oil giants. As such, MTP is set for strong growth coming two years. Profitability will rise in line with increasing proportion of higher margin IML products.

Moldtek’s machines are imported from Japan, only the robots are built in house. No real impact of the above on Moldtek’s business. The announcement is more relevant for blow molded industry & local plastic injection mold machine manufacturers.

I was looking through cash flow statement, I see that tax is shown in Cash Flow from Financing & that too as provision for tax. Can someone confirm this practice in the industry? Any CA or can some one just ask management?

I think, here provision means they will pay the tax in future ( probably in few days). As the record date for cash flow statement is Mar31st, and many companies pay tax for after the financial year so they are recording it as provision.

Similarly, you can see provision for proposed dividend. Which means they will pay the dividend within few days after the financial year complete. But on that record date i.e Mar31st it’s just a provision.

Mold-Tek Packaging Ltd has informed BSE that the Company has received LOI for setting up 2 new plants to supply pails to the upcoming new plants of M/s. Asian Paints Limited.

The capacity of the Company’s plants will start at 3500 tons of polymer processing per annum in 2019 and would reach 14000 tons per annum in 2024, subject to our pricing, service & quality.

Borouge & Sabic are pushing very hard to strengthen their hold on India market for Polymers

I would presume this will only mean softer pricing for Mold Tek in years to come

Dont see crude oil getting pricier than 50US$ for next 24 months