This is my first post on ValuePickr so all the veterans please advise, if anything is missed out to start a new discussion.

MM Forging seems to be a good story in the making.

The Company was originally started in 1946 as ‘ The Madras Motors Ltd ‘ as an importer and distributor of the products of Royal Enfield Motors from UK. The current forgings business was started in 1974 and later stopped the dealership of Royal Enfield in 1990 and decided to concentrate solely in forgings production. (Focus in one domain)

MMFL now producing forgings mainly for auto , engineering and oil industries . The Company has increased its forging capacity step by step and now operating four factories in Tamil Nadu. The Company is one of the largest forgings exporter from India and more than 70 % of total income is currently coming from exports.

Below chart clearly shows good signs of dividend and two time bonus of 1:1 clearly indicates shareholder friendly Company practices across 15 years of time span:

In my opinion, following are the positives:

Good Cash sitting in balance sheet for current year;

Sales and Net profit has almost doubled in 5 years; and

Profitability ratios in mid teens year on year and improving.

In my opinion the following are concerns:

Volume of shares traded - But I think for small cap that will always remain a question; and

Debt has increased year on year.

CMP around 520, 52 week high @ 751, 52 week low @ 421

Discl: Not invested yet but seeing the growth prospect coupled with Shareholder friendly practices tempted to invest.

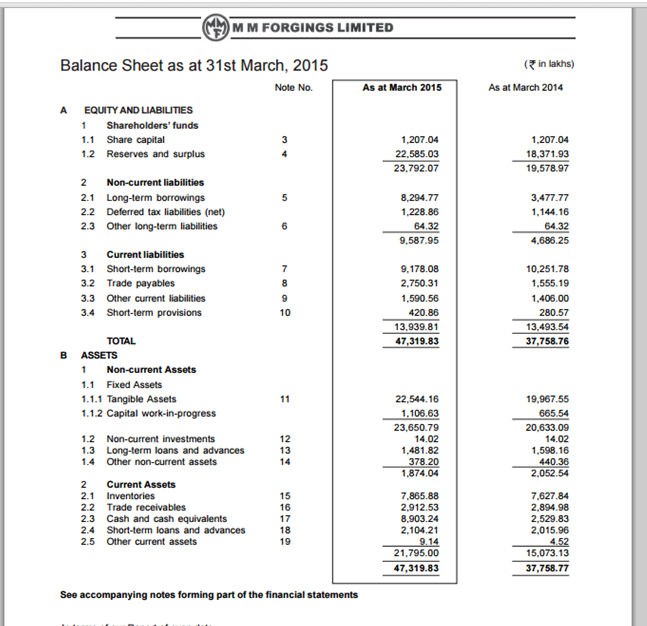

Thanks for your insights. I could not find Consolidated numbers on money control for 2015. Please find below the snapshot of current year Balance Sheet. 89 Cr is present as Cash and Cash Equivalents.

I agree with you that the volume of shares traded for a small cap company will always be less (atleast in the beginning). However that also increases the doubt that whether the price is operator driven or not. I think one way to check is that % of deliverable quantity(see link below) should be atleast >75% in such small companies. For MM Forgings it seems a bit low.

First of all thank you very much for your inputs. It is great to learn number game from veterans.

The figure is 89 Cr and what I could understand from your input is that there is 15 Cr of free cash for this year sitting at the Balance Sheet of the Company.

Further Net cash flow from / (used in) operating activities are 105.60 Cr while Net cash flow from / (used in) investing activities are (63.15 Cr) which shows FCF 42.15 Cr for FY 2014-15.

Thanks for initiating a discussion on MM. This company was coming up in my Screener filters and hence i got curious. I did have a cursory look at the annual report yesterday.

Is there a way to determine who are the major customers for MM? (The split is heavily towards Commercial vehicles followed by Passenger Cars. Given that most of their business is from Americas and Europe…have they mentioned the marquee auto customers anywhere?)

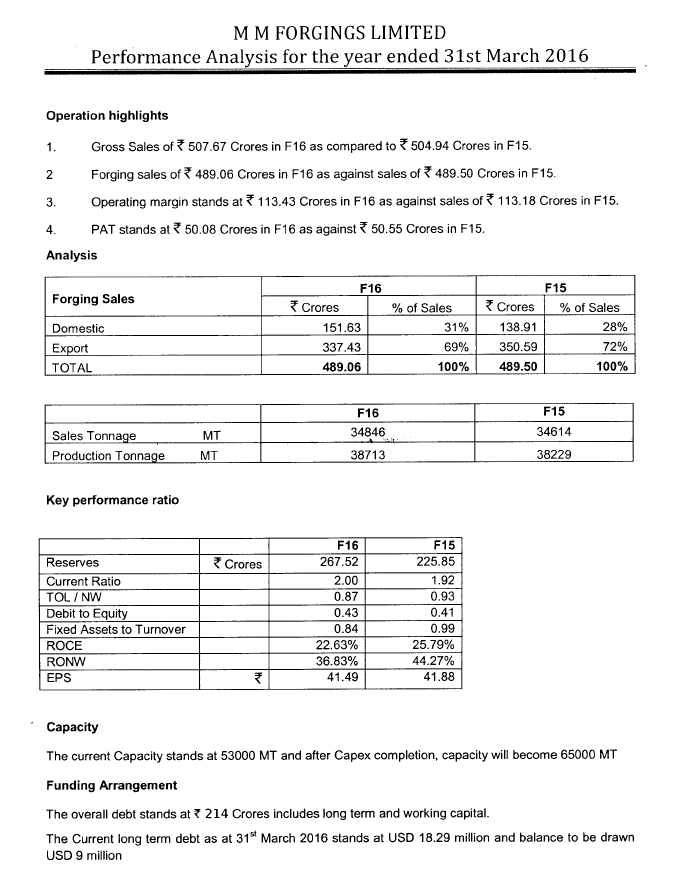

Stock has been taking a hit due to Bharat Forge news and stock movement linked to that. However strong fundamentals and attractive at current levels. Also MD mentioned in one of the interview being such a small player, it wouldn’t be too affected by business cycles in CV exports which is supposedly slow at the moment. Capacity expansion targeted more than 50% (from 40K to 65K tonnes) this year, results to show up from next year and then the stock should re-rate along with growth.

Stock has low liquidity and sometimes trade together with larger counterparts like Bharat Forge .

MMForgings has US CV market as customers which has started to slow down however if you watch the video there is an important comment from Mr. Kirshnan “MMFL is just a small fish in the bigger scheme of things”. Hence shouldn;t affect them. Also if you see the top line over last quarters has been very stable hand reached its capacity. So for growth then started to invested and expected to show up results.

guys, neone had a look at the latest quarter. they should some dip in first quarter results; is this because of start-up costs due to new capacity coming online??

Checked details from Screener - most of the things look descent - ROE, Debt/Equity, Interest Coverage Ratio, OPM and NPM being stable over last few years and earnings growth also descent.

The attached CARE ratings is A+ stable with reinforcement of healthy profitability margins, experience promoter track record. Even though the company is belonging to cyclical auto sector, the stable profitability margins reflect good execution skills of promoters and diversity in product offering of the business.

I gathered below information from various sources available on internet and company announcement, credit ratings etc:

-Total Capacity 72000 MT per year vs demand of 90000 MT per annum.(This Current capacity of 72000 is inclusive of capacity of DVS Industries which was aquired in 60Cr.)

-Four Plants:Singampunari, Viralimalai and Padappai in Tamil Nadu and one at Rudrapur in Uttarakhand

-Planned a mega capex of 500Cr which will be invested over a periodd of 2 years till FY20. 100Cr will be from internal accuarls and 400Cr will be raised from debt.

-FY18 total output was 47000 MT(72.3% of total capacity of 65000) with topline of 630Cr of topline

-FY19(Plan): 70000 MT turnover with 800+ Crores of topline which is 25% jump from FY18. Total capacity will be ramped up to 110000MT per annum from current 65000, an increase of almost 70%.

-DVS Industries manufactures approx 5000 crankshafts per month which is raised to 12000 crankshafts per month by Q1 FY19 already. Target is to take the production to 20000 crankshafts per month by December 2018.

-DVS will start contributing 100Cr to topline in fy19. Right now its contributin is 13Cr.

They have been able to pass the rise in raw material price to domestic customers.

-As of now company is focusing only on organic growth.

Overall MM Forgings looks to be a nice story which shall pan out in next 4-5 years.