REDTAPE is already famous for premium formal leather shoes. First global brand from India. Now they have diversified into different segments such as sports shoes and footwear for women’s etc…they are selling their products through almost all major online portals such as Amazon, Paytm mall, Flipkart, Myntra, Jabong, Snapdeal, AJIO, Tatacliq, and they are selling through both online and offline formats in the stores such as Shoppers stop, Lifestyle, Metroshoes. So far, they were concentrating only on exports which declined due to BREXIT and all. so slowly they are expanding their domestic presence with new range of products. these new products may do well globally who knows, in the upcoming years exports may also grow.

Mr. Shuja Mirza who is responsible for domestic market who has completed his degree from California. so obviously he could have visited many stores/outlets in USA. whatever he learnt over there with respect to retail business, store outlook etc… is applied here. As they started sports shoes with brand name "REDTAPE now+ (Athleisure range) it needs time for people to get to know about it. that’s the reason why they are selling with hefty discounts to compete with global brands such as Nike, Adidas, Reebok, Puma, Asics. so when you have to compete with the global brands, you have to sell it at affordable cost with quality, so that one can try and if the quality is at par with the global brands mentioned above, then obviously they will win the race slowly by capturing market share and when the demand increases they will reduce the discounts and no discount on new arrivals etc… This is the mantra being followed in any retail segments (Footwear & appeals).

one of my friend bought Athleisure sports shoes(black) and he is using it for the past 3+ months and he is happy with that, very soft and light weight at par with the global brands that what the feedback i got from him. Younger generation people those who are major customers for the sports shoes. if the quality is good, no doubt people will go for it. i think from March 2018 they started serving Women’s as well which is a huge market globally. men used to have few pair of sandals or shoes where as women used to have more pair of sandals/shoes comparatively. nowadays people become so conscious about their health/fitness. so to be fit by going to GYM, Walk, Yoga, Aerobics etc… 5 to 10 years back that was not the case, right? nowadays i see age old people (mothers/grandmothers) also started wearing sports shoes and walking in the morning which is a good sign. even i am thinking of getting a pair of buying a pair of sports shoes for my mom. I didn’t mean that everybody will buy REDTAPE, as they are expanding in domestic, people will give a second thought of buying their shoes as the feedback/reviews are good and available at affordable cost.

Why do they need retail stores? as they are coming up in new segments/products for Men’s & Women, they want the people to visit their stores and get a feel of the product. i would say this as a marketing strategy. unless your brand become popular, your brand gets recognized, you need retail store to exhibit your products and make the consumers understand and feel it. This can happen only in their own retail stores. Even in metro shoes they have Redtape brand as well. but they may not advertise the same way you do for your product. because as they have so many brands, where ever they get margin, they will advertise those brands only. so, my point is to create awareness among people they need retail stores. Even now many people including me before buying a sandals/shoes we go to that exclusive show rooms and check the model/size whether it fits perfectly. then i will order the same through online as online portals offer hefty discounts.

Initially they may not be making huge profit as they are spending on opening new stores. over a period, say after 2 years or so the brand REDTAPE will be one among the global brands in sports shoes section. with the assumption that the quality is good and at par with other global brands. That time they will reduce the discounts and they may close loss making stores as the brand become popular. Eventually the major sales will be through exports/online.

I do read that from many other posts, reports that the this is family run business and they do have some private companies, and they draw huge money as salaries and charge hefty commissions for bank guarantees etc. Again, retail expansion is not so easy, and they may lose some money. but once you build a brand which will pay for you later years (after 2 to 3 years)

I am still in my learning curve, if anything wrong with my views please feel free to point it out. Please provide your feedback which will motivate us to study and share our views on businesses

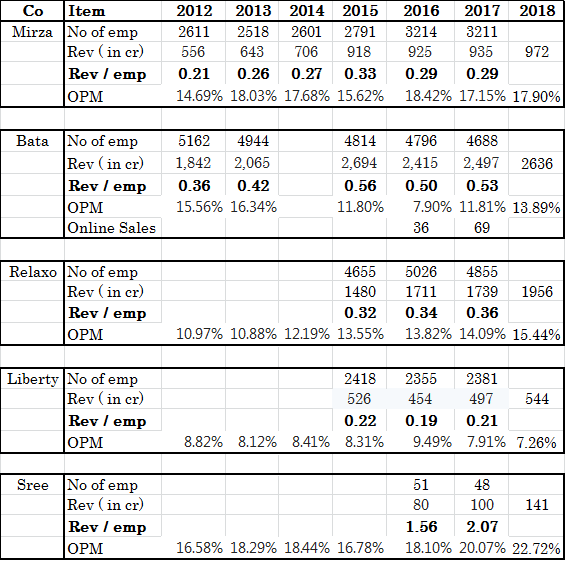

Retail store details:

No State No of stores(july18)

1 Assam 1

2 Bihar 2

3 Chattisgarh 2

4 Delhi 30

5 Haryana 17

6 Jammu & Kashmir 2

7 Jharkhand 3

8 Karnataka 6

9 Kerala 1

10 Madhya Pradesh 6

11 Maharashtra 12

12 Manipur 1

13 Punjab 24

14 Rajasthan 9

15 telangana 3

16 Utterpradesh 12

17 Uttarakhand 6

==========

Total as on July2018 137

==========

Note: Even though all the story looks good, still i am keeping it in my watch list. may add position slowly on dips. This is not an investment advice, please consult with your financial advisor or research analyst before you buy.