Then I think we need to look at longer history to understand promoter psychic with transactions in own share. Will check. Thanks for highlighting

5 Likes

Just trying to get a sense here and some preliminary views that I have after going through some numbers. No indepth study so looking for answers.

I see downside more than I see upside

They are planning to load up on the debt to grow earnings - like what relaxo had done. But relaxo had room to increase prices and a short replacement cycle for slippers. I don’t see that in mirza

What am I missing here? Relaxo itself is seriously overvalued.

If roc stays where it is for mirza, the PE will drop further to maybe 6-7 - But earnings will grow. If earnings grow by 50% and PE falls by 50% - the price won’t go anywhere

I looked at multiple reports - anand Rathi is actively tracking it. They are all projecting an roe of 15% that also on a levered balance sheet.

Any perspectives appreciated

Their current RoE is around 14%. With the additional leverage of 126 Cr (Debt inc between FY17 and FY18), the D/E is now 0.47 compared to 0.28 last year. If they can continue to generate a RoCE of 20% on this additional capital, EBITDA should increase by 25 Cr which should increase the PAT by about 15 Cr i.e 20% inc in PAT compared to FY18 which is roughly what the management has guided for. This means a RoE of about 16% from their current RoE of 14%. This is assuming their domestic business continues to perform which is what my bet is on, having seen the way they are focusing on and getting traction in a relatively short-time they have been focusing on the domestic market. They do have issues with their inventory but its too early to call it trouble as their justifications in the concall seem reasonable.

Now export market has been de-growing for them but recent months have shown marginal uptick in exports for leather footwear to UK so maybe there is some recovery there as well which will definitely help going forward.

Leather Footwear exports to UK

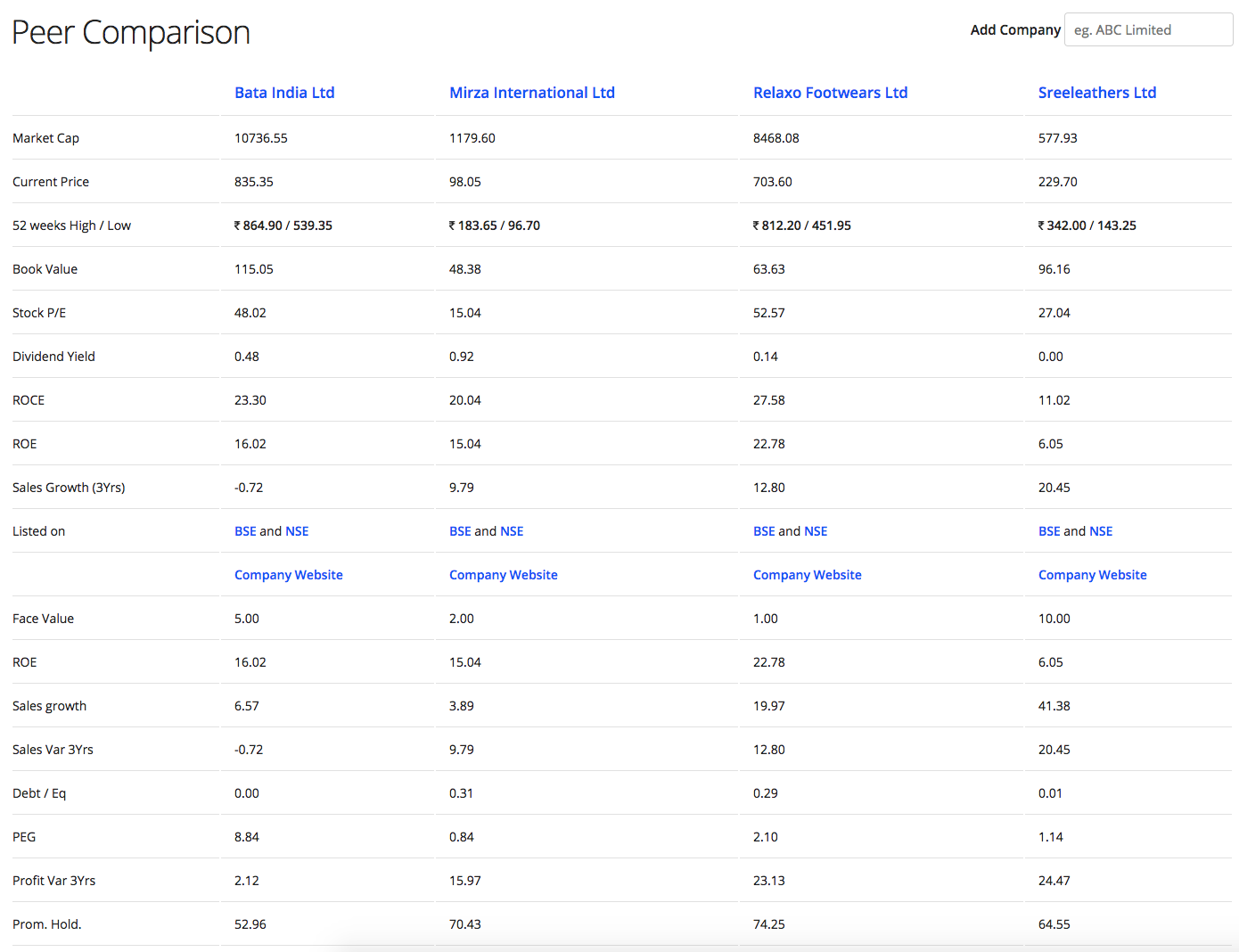

Current EV is around 1450 Cr and with a EBITDA of 200 Cr in FY19E (Up 15% conservatively from FY18), EV/EBITDA is about 7. Bata and Relaxo trade at 26-28 levels and even Sreeleathers trades at 17. It is this relative valuation gap that is giving me comfort in investing in Mirza. Views may change over the coming quarters after listening to management further and following the P/L and AR when it comes.

3 Likes

If I remember correctly, the increase in stake you refer to earlier was not a market purchase. They took this as a consideration for acquiring a promoter-owned company named Genesis Footwear. The decrease that @Marathondreams refers to above is due to reclassification of some of the not-very-active promoters. Some of those not-very-active promoters had also been selling prior to the reclassification, and maybe the company did not like all those insider trading alerts to be triggered!

Overall though, my sense is that the margin of safety is very high in this company. I personally feel that corporate governance moves on a scale from white to black, and I am okay with light gray shades. As long as the company throws up a good amount of cash, am OK with the promoter helping himself to some. This company seems to have strong fundamentals. Also no promoter pledging of shares. I’m writing more below in another answer.

Disclosure: Invested, from very low levels

Hi @phreakv6

Appreciate your views. My concern mainly stems from how much capital you can deploy efficiently in this sector because Mirza is not a small co , it is equivalent in size in terms of its capital base compared to some other footwear cos. So maybe the amount of capital the industry can absorb could be capped due to size limitations. Bata is working with a capital base of 1400cr and we know that they have been around for a while, similar is the case with Relaxo which is working with a similar capital base. Just trying to get a sense of the scalability and trying to point out that sometimes the sector is just not that big as we think keeping in mind that mirza has ambitious plans and they are going to add more capital to their already large base.

| 2018 | Mirza | Bata | Relaxo |

|---|---|---|---|

| Capital Available for deployment | 841.35 | 1474.69 | 886.56 |

1 Like

Dear @bheeshma, you must note that most of Mirza’s capital base has been deployed so far for exports. One thing the company said in its conf call was that because the flagship brand was at a premium price point, that would restrict the market. Acc to them, their entry into sports shoes and Bond Street was because this segment could be a good growth engine.

For sports shoes and Bond Street, they aren’t manufacturing these - they are being traded; so the investment is really in working capital. They want to gauge the response, and if and when a critical mass is reached, they will invest in manufacturing facilities for these.

I feel that any of the following levers, if they fire, will more than justify the current price level:

- Turning around of UK exports, as @phreakv6 pointed out

- Opening up of new export markets, especially if the US is cracked. This is very low probability; I recall the company trying to crack the US puzzle for some years, without notable success. Falling rupee helps (in the very near term)

- The domestic story for their flagship brand working out, with the renewed focus

- Bond Street and / or sports shoes tasting success

There are some risks:

- Corporate governance is light grey. Some of this has been discussed on this thread. I am personally OK with these type of transgressions. An analogy: I see many people also draw the line differently in case of domestic help “borrowing” stuff. Some overlook small items because the quality / value added by that help is much more, while some are fanatical in drawing a line with zero tolerance. To each her own

- Competition is intensifying in the sector. I can see aggressive moves by Pavers, Clarks, Ruosh. Hush Puppies is also gaining traction (I like Bata, which owns the Hush brand, but valuation is too stretched for my comfort)

Overall, I take comfort from the strong brand and good quality of product. I have personally used (and know many who use) their shoes. Also reviews on e-tail sites (incl. Amazon UK) are positive, as pointed out in this thread also. Scuttlebutt corroborated this story for me. The fundamental financial numbers are strong. Dividend has been rising. Debt was reducing until recently - when they started expanding the sports and Bond Street business.

Red Tape is also an old established brand - there is even an old ad with Salman Khan. They later reduced focus on the domestic market; now there is renewed attention. I like the idea of really owning a strong brand (unlike say a Page Industries, which merely licenses Jockey). Hopefully, it will pay off (it already has, but the heart wants more!)

Discl: Invested, from low levels

8 Likes

Does anyone know how many pairs of footwear were sold by Mirza in FY18?

FYI, following are the nos i could gather about the 2 competitors:

Bata: 47 Mil (Source: Annual Report FY18)

Relaxo: 157 Mil (Source: FY18 Q4 ppt)

Regards,

django

I remember both export n domestic nos were discussed in concalls of last 2 years. So, can be searched there.

We need to understand some key points when a business tries to transition from a B2B to B2C, this will also highlight the risks that one needs to watch for -

Order fulfillment to Order Management - In the export business, their models get approved by large chains they are selling to, quantity etc is also decided by this counter party. In any business the entity closest to the customer decides the quantity, style and seasonality of the business. Since MIL works as a white label manufacturer for majority of the exports, they just have to focus on getting the product made on time and to right specifications, then they transfer the entire lot to Mirza UK which in turn does the bulk breaking and supplies to end counterparties. In an order fulfillment model demand planning, inventory management, receivables management is not on MIL

In the domestic business where they are selling a brand they own, the effort required is humongous since they also need to focus on demand planning, managing inventory across channels (EBO, distribution and e-commerce) and also manage receivables well. What models to produce, where to sell and what price to sell at are all decisions that MIL needs to take internally. Suddenly things like seasonality of particular models, the right placement, inventory obsolescence and pricing management at a bigger scale become very important

Which is why the business will be hungry for funds over the next 2-3 years since they are building channels and infra from the scratch in most places. Scaling up from 150 stores to 300+ is not easy and will call for significant channel capex - which is what Shuja keeps mentioning on the conf calls that channel capex is what they need now, not manufacturing capex. Building an optimizing this channel not only to put the product on the shelf but also set up a demand sensing mechanism that can give inputs to their design team calls for a change in how the teams are working right now.

I’ve run the numbers for capex per EBO, rent per store and store expansion plans across some players (Bata, Relaxo, Metro) and MIL appears to be doing things that are logical, most players are thinking on similar lines. Where MIL appears to be ahead of the game is in terms of their proportion of sales from online, they have shown a very steep ramp up - obviously at the cost of higher working capital since most sales are happening on the consignment model.

There are some very interesting things happening now, investing into a business like this will call for a much deeper analysis than just looking at high level financials. By the time (if that so happens) the financials start reflecting all the positive changes my sense is this one would have run away. There is always the possibility that the market may see higher debt QoQ and start becoming more conservative but we need to look deeper and see how the B2C transition is being managed internally

24 Likes

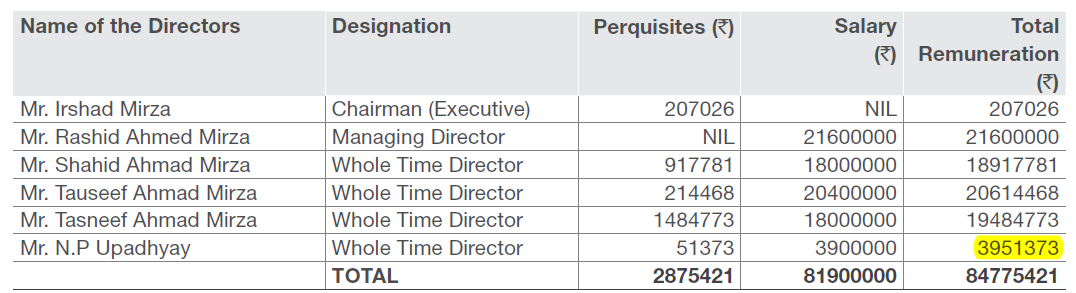

Salaries as a % of sales have gone up from 5% to 9% between 2015 to 2018. High salaries are causing the profits to go down requiring the company to borrow money to fund expansion and then promoters charge the company for proving loan guarantees. Because of this, their cost of debt is also high at 14%. Promoters should be bringing in the capital to help the company grow, not milk it as if it is operating it at its peak profits. If this is how they behave when the company is small, imagine how they will behave when (or if) it grows. No large investor will be willing to fund such a business.

Promoters could have easily pledged their shares to provide loan guarantee. None of the promoters have pledged their shares. From a lender’s perspective, pledged shares is always a better way to guarantee loan than a personal guarantee since it is easy to invoke. It is as if promoters want to provide a personal guarantee so that they can charge the company for doing so.

Salaries would have been OK if only the top 1 or 2 guys were earning at that rate. There are too many Mirza’s running the show. I don’t think so many are needed. A professional from the retail industry is likely to do a better job and will work for less. Since company is venturing into a new line of business where its expertise is not proven, ESOPs are a better incentive than cash compensation. Needless to say, there are no ESOPs outstanding.

The only non-Mirza director earns less than 1/5th of the salary of the Mirzas.

Source: 2017 Annual Report

About the products, I think premium genuine leather shoes will be expensive and I am not sure if the market for that is large. There is definitely a market for that but I think income levels in India have not reached a level where there will be huge demand for premium genuine leather shoes.

Low cost branded products sounds like an oxymoron to me. A brand is created to communicate quality in a market flooded with low quality products. You don’t need a brand to sell low cost products. They are also not making it but just selling it. It will suck capital away from the premium brand which needs it most. They are trying out everything hoping something will click.

Lots of items are offered at a huge discount on their website. Usually, high quality products are not offered at a huge discount.

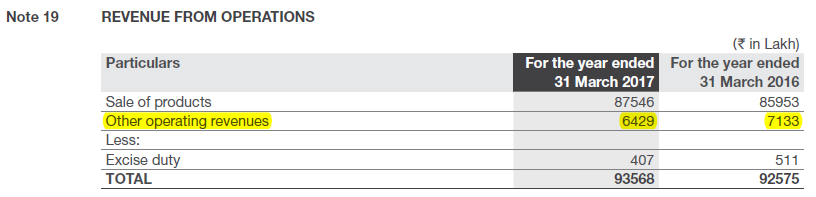

I noticed a large Other Operating Revenue under revenue. It is as much as PAT.

Source: 2017 Annual Report

Its been there for many years. Any idea what is that? Is it job work charges or franchise fees? No detail are available anywhere and amount is material. Annual report is full of grand plans and short on specifics.

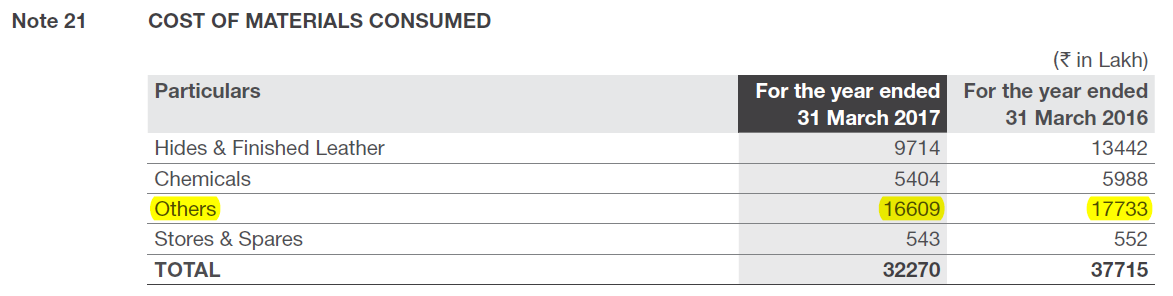

I also have a question about their costs. Here is a screenshot from 2017 AR.

Source: 2017 Annual Report

Any idea what is this Others cost? It takes up 50% of raw material costs. Also, why Hides & finished Leather cost is going down 28% when sales are growing? If you consider cost of Hides & Chemicals as the actual RM cost, gross margin works out to be 85%. Only super premium brands have such high gross margins.

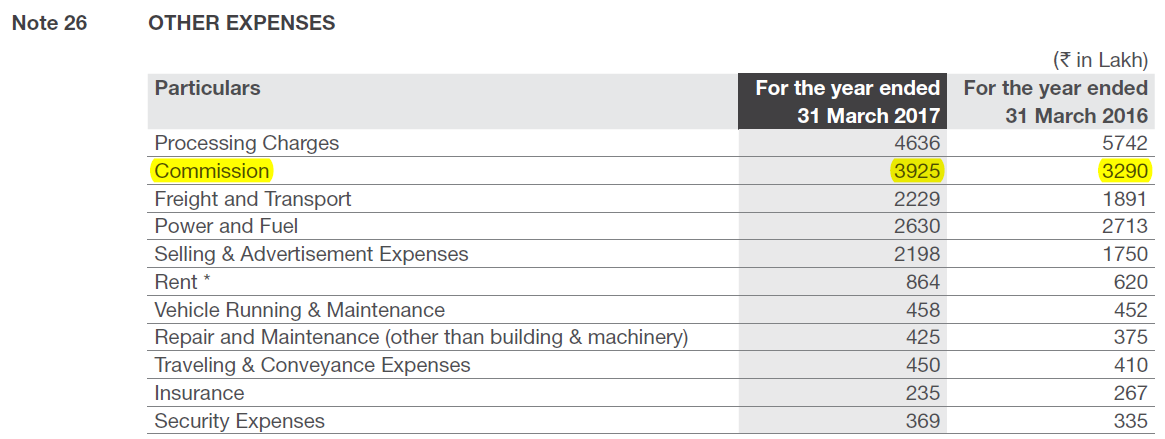

As already pointed out by other members here, guarantee commission is same even when guarantee amount has dropped.

Source: 2017 Annual Report

Overall commission expense is also growing much faster than sales.

Source: 2017 Annual Report

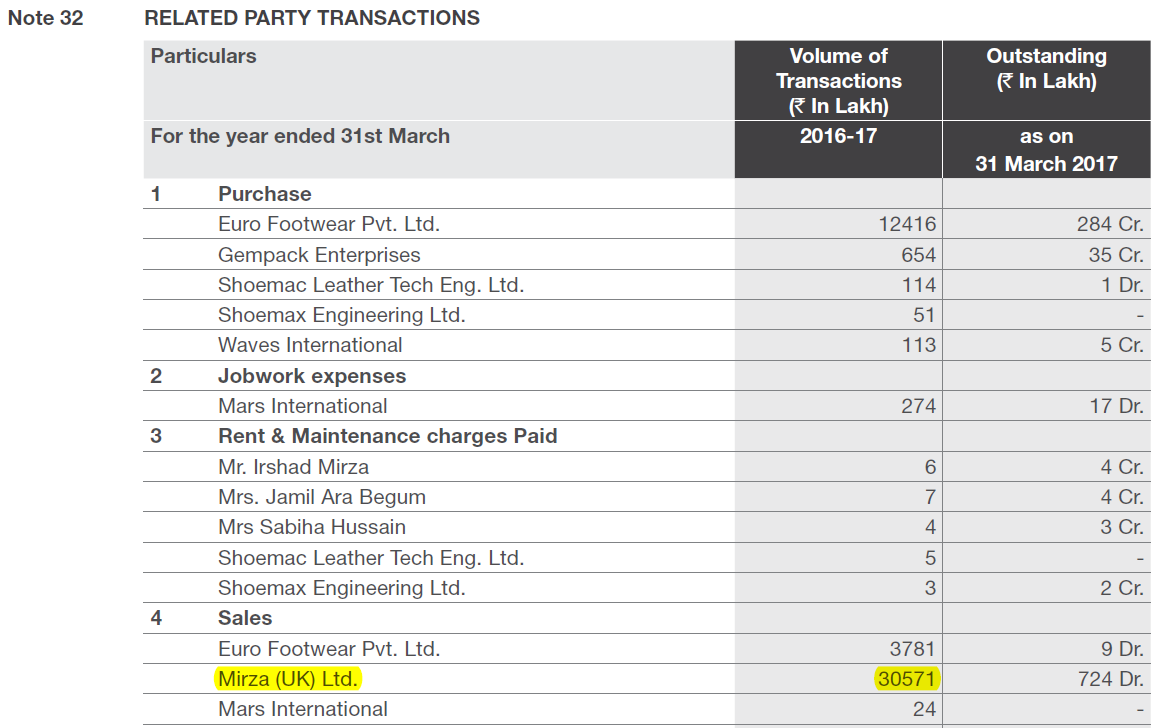

A large amount of sales is going to Mirza (UK) Ltd.

Source: 2017 Annual Report

33 Likes

On leather shoes, something struck me now. I have used their red tape leather shoes and quite happy and also checked with few users in North in circles and got very good feedback. But then this thought - if you see 10 years back companies like TV’s, Infosys . Wearing leather shoes , formals etc was good corporate manners but I think the corporate India is evolving due to millennials and I think in many startups it is cool to not wear leather shoes but other forms of shoes. After coming back to tech sector post working in mgmt profiles, I realise that my purchase pattern of shoes has changed on similar lines as there is no obligation to wear leather shoes in most companies. So, I keep 1 pair and use very less on specific occassions. Less use means longer replacement cycle. I am not sure if there is quantified number and may be we should check nos across companies but there could be case of partly product line expansion to expand business as well as self cannibalization . If they do not do some one else do. Cultural changes are slow to happen but they are more destructive if not handled

@Yogesh_s have found this family count issue with many companies. Infact, in many everyone will be given equal salary n equal salary raise . It also dampens motivation of any external employee. I remember reading an AR where wife of promoter was CSR head and her annual salary was higher than overall annual CSR spend

4 Likes

Amount of hard work & wisdom in Yogesh’s posts are just amazing. Thanks for your time & heart. Much obliged.

2 Likes

Posted about cultural disruption n next thread read this article what co-incidence. I think this would be equally valid for leather shoes . However, my initial feel was self cannibalization could be a way to overall market expansion but looks like electronics industry is doing it better than apparel fuelled by cultural changes

https://www.bloomberg.com/graphics/2018-death-of-clothing/ 2

1 Like

Will attempt to elaborate my views on some of the points here -

-

Salaries going up - this has to be seen in context of the Genesis footwear acquisition. Prior to the acquisition Genesis was taking RM from MIL, using skilled labour to convert this into end product and selling this back to MIL (Genesis was a 35% EBITDA margin business which promoters were happy milking till 2016). Thankfully they have amalgamated Genesis into MIL, hence the processing charge has come down since 2016. Bottom line is that the trend of Salaries + Processing charges as a % of sales is a more realistic picture, this was covered in one of the conf calls as well

-

Promoter guarantee, guarantee commission & high promoter salaries - My first reaction was that this is not something I understand and am surely not comfortable with. Looks like the guarantee commission and promoter salaries will only scale with sales, I left this as a risk I have to live with. Promoter salaries given that there are so many of them is very high, in fact the highest I have seen so far across all of my investee companies

-

Issue of a weak BoD - One look at the profiles of the BOD and one can say that Irshad Mirza towers above all of them in stature. The directors appear to have been picked based on friendliness/familiarity with the family and not based on standards of corporate governance. In case of something going bad none of the independent directors have the stature to keep things in order. Overall I rate the corporate governance as weak. In fact Irshad Mirza was doubling up as the CFO signatory as well, it does not get weaker than this. However I see the AR and conf call messaging and the Genesis amalgamation as positive steps that are slowly being taken - this is my personal opinion and one can debate this

-

Other operating revenues - I remember this as the export incentives that they receive, once can see export incentive receivables tracked under current assets

-

Increase in commissions & ASP - Am happy to see that this is finally going up, this shows that they are finally playing ball and incentivising their trade channels. Also see this in context of what the industry averages are - Relaxo spends 6%+ on BTL and almost 3.5% on ASP, MIL is currently at 5% and 2.5% resp, Khadims is at 3.5% on ASP and minimal on BTL since they are primarily a distribution house. MIL spends on BTL and ASP have spiked since 2013 - BTL was 3.3% in 2013, ASP was 1.7% in 2013

-

Large amount of sales to Mirza UK - Mirza UK has a set of local UK directors in addition to some of the promoters being on board. They have bank facilities from HSBC and RBS in place, the entity has approx 60 Cr of net worth with 30 Cr+ in cash, net profit of approx 8+ Cr appears to be getting generated annually. One can see company details here https://companycheck.co.uk/company/02802325/MIRZA-UK-LIMITED/companies-house-data, looks to be a genuine entity with a large warehouse in the UK which is being used for bulk breaking and supplying to the large retail chains.

6 Likes

Promoters have indicated that the guarantee commissions will not go up and stay at these levels- on growing operating profit levels- this component (as a %) would keep on decreasing.

Finally this is still a family-owned business and irrespective of their contribution, different brothers would want reasonable compensation- Obviously, this is far from good corporate governance but we have to consider that legally they can pay-out around 10% of PBT as director compensation and till now they have largely adhered to that limit.

1 Like

Why is Mirza (UK) a related party and not a subsidiary of MIL? How do we know if transactions between Mirza (UK) and MIL take place at arms length? This is important in the context of overall weak corporate governance standards at the company. Same question with Euro Footware.

Form AOC-2 in the annual report shows that transaction with Euro Footware is approved by the board but not Mirza (UK).

4 Likes

Compiling data from ARs, shows some interesting trends

| Revenue by Geography | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|---|

| International | 48386 | 50587 | 70732 | 69171 | 65068 | 51787 |

| Domestic | 15987 | 20148 | 21167 | 23701 | 28588 | 45421 |

| Total Revenue | 64373 | 70735 | 91899 | 92872 | 93656 | 97208 |

The topline has been flat since 2015, thats really when changes start happening in the co, uptil 2016 the co was chugging along doing business at the international to domestic ratio of 75:25, but post 2016 - revenues from domestic business have been excellent and now about 47% of the business comes from domestic. Due to the high base of the international business , the combined impact on the revenue has been muted - but as the domestic revenues grow the impact on revenue will gather pace and approach the growth rate of the domestic business.

| Revenue by Geography | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|---|

| International | 75% | 72% | 77% | 74% | 69% | 53% |

| Domestic | 25% | 28% | 23% | 26% | 31% | 47% |

| Total | 100% | 100% | 100% | 100% | 100% | 100% |

During this period when the international business was 75%, the RONW was good and averaged about 17%, In the last two ( 2017 & 2018) years it has averaged about 14%

| Item | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|---|

| PAT | 4345 | 4337 | 5116 | 7809 | 7120 | 7841.22 |

| Net Worth | 25129 | 28656 | 31247 | 44562 | 50364 | 57179.18 |

| RONW | 17% | 15% | 16% | 18% | 14% | 14% |

The co has reported segment info by Tannery and Shoe - which are the two main operating divisions of the co, and breaking up the return ratio further , one can see that the tannery division doesn’t contribute anything significant to the overall profitability of the co and has over the last 6 years of info that i have looked at - has contributed 0.7 % to 1.5% on an average to the RONW.

| Item to NW ratio | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|---|

| A -Tannery PBIT | 0.8% | 0.7% | -1.9% | 1.3% | 1.2% | 1.4% |

| B -Shoe PBIT | 46% | 42% | 51% | 40% | 33% | 30% |

| C -Unallocated PBIT | 0% | 0% | 0% | 1% | 0% | 0% |

| D -Interest | -13% | -11% | -13% | -7% | -5% | -4% |

| E -Unallocable exp | -9% | -8% | -11% | -9% | -8% | -7% |

| F -Tax | -8% | -9% | -9% | -8% | -7% | -7% |

| (A+B+C+D+E+F) RONW | 17.3% | 15.1% | 16.4% | 17.5% | 14.1% | 13.7% |

As expected ,all the heavy lifting has been done by the Shoe division which in the export intensive days was contributing as much as 51% to the RONW. In the new 2018 scenario however it currently contributes to 30% , another 1.4% is through tannery and the remaining expenses like taxes, interest and Unallocable expenses (Unallocable expenses would be HQ corporate expenses) takeway 18% - leaving shareholders with a return of 13.7% net on the funds invested.

Of particular note are unallocable exp which i assumed to be corporate HQ expenses that have been a drag bringing down the return by 7-8% - which is significant as its more than the interest cost or the tax they are paying.

Excluding all the corporate excesses, the tannery division continues to be very expensive to maintain and run.

| Share in Assets | ||||||

|---|---|---|---|---|---|---|

| Division | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Tannery | 29.5% | 31.3% | 29.6% | 28.0% | 26.5% | 22.1% |

| Shoe | 65.9% | 64.9% | 66.9% | 68.1% | 69.6% | 74.5% |

| Unallocated | 4.6% | 3.8% | 3.5% | 3.9% | 3.9% | 3.4% |

| Share in Revenue | ||||||

|---|---|---|---|---|---|---|

| Division | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Tannery | 12.0% | 11.8% | 13.3% | 11.5% | 9.8% | 7.1% |

| Shoe | 88.0% | 88.2% | 86.7% | 88.2% | 90.1% | 92.9% |

| Unallocated | 0.05% | 0.05% | 0.07% | 0.32% | 0.09% | 0.04% |

| Share in earnings | ||||||

|---|---|---|---|---|---|---|

| Division | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Tannery | 1.6% | 1.7% | -4.0% | 3.0% | 3.7% | 4.3% |

| Shoe | 98.1% | 98.0% | 103.6% | 95.4% | 95.8% | 95.4% |

| Unallocated | 0.3% | 0.3% | 0.4% | 1.6% | 0.5% | 0.2% |

In 2018, the tannery operation consumed 22% of assets, contributed to 7% to the topline and 4% to the bottom line. In 2013, that ratio was 30%, 12% and 2%.

Mirza has a great tannery operation but it consumes a lot of capital, is running at a low capacity and clearly is a concern area and one of the reasons why Mirza has decided to expand Red Tape branded leather domestically is to improve its contribution to the overall operations & its showing here. Share of the tannery operation in the earnings while low , has improved to 4.3% in 2018 from 3% in 2016, since they decided to expand domestically further.

A further look at the margins, underlines the improvement in the tannery operation that has taken place. The improvement in the capacity utilization brought about by the expansion has improved its operating margins from 3% in 2016 to 11% in 2018 - however margins in the shoe business have roughly remained the same over time.

In my view, going forward the margin expansion, will be driven by the improvement in the tannery operation and that really is the thesis - i.e the asset turnover will be driven by the volume in the shoe division while the margin expansion will come from the tannery division

| Margins ( before interest, tax, corporate hq exp ) | ||||||

|---|---|---|---|---|---|---|

| Division | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Tannery | 3% | 3% | -5% | 5% | 7% | 11% |

| Shoe | 21% | 19% | 20% | 22% | 19% | 19% |

The tannery + shoe combo makes for an interesting thesis and one that needs to be validated by results in the ensuing quarters.

As per concall - I think the debt levels is going to be roughly 340 cr in fy19 , so the capital invested in going to increase quite a lot however, with my revised understanding of whats at play here i think that the return ratios will revert back to their original 17% levels.

Best

Bheeshma

I have attached my workings should anyone want to have a look Mirza.xlsx (20.7 KB)

10 Likes

We need to keep in mind that MIL started with tannery operations, then got into shoe making as a natural extension. This is how most shoe makers in that region of India started and is not very surprising. Margins are the highest where value addition is the maximum, hence MIL has been concentrating on becoming a footwear maker over the past several years as opposed to expanding tannery operations as well.

In my opinion the integration into tannery does some value add but is not a strong differentiation by itself. Look at the Metro shoes story, 1100 Cr topline and 90 Cr bottom line with 20% growth in store count, Sales and PAT over the past several years at 30% ROCE. They do not own a tannery, they did not even do design in house and have only started recently. What the tannery brings to the table is access to a talented pool of craftsmen and raw materials - gross margins will be higher due to in house tannery but by itself not a strong factor in my opinion.

We also need to see that the newer product lines are all being launched through outsourced manufacturing - Bond Street, women’s range and sport shoes. These will not call for investment into gross block and will need high working capital initially. Hence fixed asset turns will anyway improve here, what we will need to track are total asset turns which will show a dip over the next few years since the investment into channel capex will take time to show up in sales and bottom line.

The question that in my opinion are critical are -

-

What is the length of the runway available to MIL to scale the domestic business at 30% over the medium term? Can we get to a stage where MIL opens 30-40 stores every year from here and can do approx 3-4 Cr of incremental sales from each store after the initial 12M period?

-

How does MIL manage the trade off between higher working capital needs and higher growth? Will they chug along at the current rate and keep expanding their balance sheet as long as 15-20% earnings growth is delivered? In that case we have a story where EPS growth is a given but ROCE will be around 15% and ROE might be lower - if so how will the market react?

The basic economics of the business are very good in my opinion, look at the string of healthy operating cash flows from 2010 through 2017, MIL was free cash flow positive in 4 of the past 5 years due to which they were able to reduce debt levels. From 2018 onward this story has changed due to the heavy channel investments.

If the management can figure out the right mix where they can grow earnings by 15% without dropping capital efficiency, we may have a very interesting story on our hands.

@Yogesh_s - Valid point, one which I have do not have an answer to. I am just going by the willingness of the management to do regular conf calls, take the effort to communicate their business pivot through the AR’s over the past few years and the Genesis amalgamation as initial positive developments in the corporate governance journey. Overall there are issues with corporate governance but I am comfortable building in some buffer into valuation and moving on with things

5 Likes

Here the story in very simple terms:

-

The management improves their corporate governance issues, whatever there are now, and the market recognizes it along the way and rerating happens along with other highly valued businesses in the same space.

-

Mirza developed a brand from scratch REDTAPE and market gives rerating depending on the brand pull and it’s value as the domestic business keep on increasing its share.

If point 1 does not improve then it will continue as it is like any other family business and market will ignore it.

PS: I have been using these shoes more than a decade, because of quality and thinking it’s a overseas brand till couple of years back and was surprised owners are family run Mirzas. I use very roughly and they last minimum 12 months and buy whenever I come for vacation to India. Their shoe quality is second to none what ever I have seen in middle east countries.

2 Likes