Since the company is listed on SGX as well, there were couple of queries submitted by SGX investors to which the management replies are as follows:

3 Likes

Interview of Mr.Ashish Soparkar conducted on 15th June, 2018:

The key points that I have taken notes of from the interview are as follows:

Agrochemicals:

-

15-20% growth - internal target

-

70% export, 30% domestic

-

reduced cost of energy, employment, banking interest, reduced our working capital need so margins will improve here upon

-

current capacity utlization -70%, target is 80% this year.

Basic chemicals:

-

Caustic soda prices are still good to maintain decent margins.

-

chlorine prices are zero/+ve this will improve margins in basic chemicals business which were -ve previous years.

-

target for basic chemicals is 750 crore because of high ECU and chlorine prices

-

CMS plant will be available only for one quarter

Pigments:

- 15% is bottomed out, we are trying to improve out margins from 15 to 17%.

6 Likes

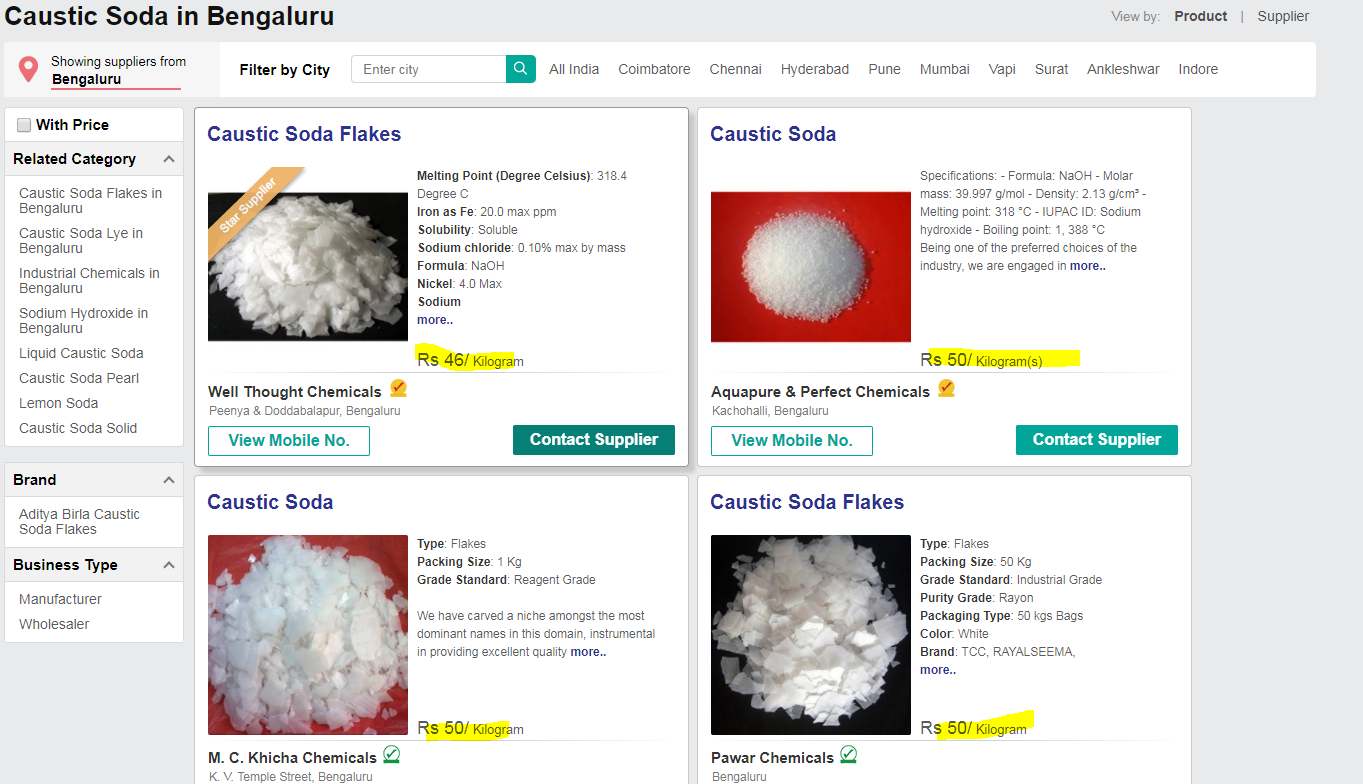

I was trying to find out if their is any decrease in caustic soda prices. As per below screenshot they are selling around 45-50 rs per kg. Seems thier is not much decrease in the caustic soda prices and we may see similar margins at least for Q1 also. In Jan 2018 , caustic prices in US sport markets were around 581$ per ton (approx 39 rs per kg) as per below article. So their do not seems to be much change here.

which are the other major raw materials or products they are highly dependent on in agro chemicals and pigments ? Can anyone please tell me ? I would try to search and get more information.

I dont have much understanding of Chemical business and pricing, So above info may be right/wrong also. Please feel free to correct me if you differ with my views.

1 Like

In their concall dt 28.05.2018 they have mentioned as below regarding the ECU realisation of Chlor alkali division:

“I will tell you, under chlor-alkali we consider only caustic and chlorine, rest are the chlorine derivatives and that is the separate industry altogether, alright. And chlor-alkali we believe the price would be in the range of 35,000 to 40,000 this year. It is very difficult to forecast being a cyclic industry what is beyond the quarter, actually. But this year on an average we can believe it will in the range of this one.”

Annual report 2017/18 on the link below

To view / download AGM Notice, Annual Report, Proxy Form & Attendance Slip

1 Like

Shareholding Pattern of Top Ten Shareholders (Other than Directors, Promoters and Holders of GDR and ADRs)

Name of Shareholders Shareholding at the beginning Cumulative Shareholding at the

of the year – April 01, 2017 end of the year- March 31, 2018

No. of Shares % of total shares No. of Shares % of total shares

of the Company of the Company

DBS Nominees (Pvt.) Limited 22653600 8.91 13623540 5.36

VLS Finance Limited 7500000 2.95 6230000 2.23

Gadia Naveen Vishwanath 2869250 1.13 3140100 1.23

Emerging Markets Core Equity 135346 0.05 1502232 0.59

Portfolio

Dolly Khanna 1020665 0.40 939652 0.37

ICICI Bank Limited 597685 0.24 892656 0.35

VLS Capital Limited 1795646 0.71 790611 0.31

Angle Broking Private Limited 629901 0.25 728350 0.29

Goldman Sachs (Singapore) Pte. Ltd. 1316810 0.52 24922 0.01

Ashmore Sicav Indian Small Cap 798137

Marque Investor Dolly Khanna continue to hold Meghmani .

She has reduced her holdings, and historically Khanna’s have reduced their stakes slowly and over a period of time. Hope it is not the beginning of the similar phase in meghmani

Hi Raj_A_A

Will you be able to share the link of the latest shareholding pattern shared above.

Regards

Pawan

The next key trigger for growth in Basic Chemicals will come from their expansion in Chloromethane, Caustic Soda Plant and Hydrogen Peroxide. For which, In page 32 of the AR in Management discussion and analysis they have mentioned as below

"Last year, the Company initiated a landmark capex plan involving Rs. 6.4 bn of investments in Basic Chemicals. With the Company already operating at very high utilisation levels, this project is expected to be a major growth-driver going forward. The capex, which involves three projects, progressed as per plan during the year. The First Project of Chloromethane (CMS), with three coproducts i.e. Methylene Dichloride (MDC), Chloroform and Carbon Tetra Chloride (CTC), is expected to be commissioned by December’18.

This is to be followed by the Second Project related to expansion of Caustic Soda by 300 TPD, and Third Project,involving setting up of Hydrogen Peroxide plant of capacity 30,000 MTPA. Both of these projects are expected to be commissioned by June’19"

Again in Page 39 of the AR they have mentioned as below

“The Company’s planned capex of Rs. 6.4 bn involving 3 projects are in-line with its strategic intent of expanding the chemicals business. The First is the CMS project of 40,000 MTPA which will produce MDC, Chloroform and Carbon Tetra Chloride. This is expected to be commissioned by December’18 and add Rs. 1.2 bn of revenue post full year of operations.The Second Project involves 50% capacity expansion of the Company’s Caustic Soda plant to 2,71,600 MTPA and increase the Captive Power Plant capacity to 96MW from 60 MW now. The Third Project is to set up a Hydrogen Peroxide (50%) project of 30,000 MTPA capacity. Expansion of the Caustic Soda and Hydrogen Peroxide projects will involve Rs. 5 bn investments and are expected to be commissioned by June’19.”

Industry outlook in Chairman Speech also looks promising,

-

Global Pigments is expected to grow at a CAGR of 4.1% between 2017- 2023 reaching $27.6 bn by 2023. Indian pigment sales have been growing at a rate of 13-14% over the past five years. This growth is driven by boost in exports. Capacity utilization in the Pigment industry has been only 67% which shows that there is a great potential of increasing the production and business in this industry.

-

The Global Agrochemicals market is likely to grow at a CAGR of 4.1% from 2017-2025, crossing $309 bn by 2025. Growing population, declining arable land and increasing pest concerns are driving the Agrochemicals market. Demand for Agrochemicals is the highest in the Asia Pacific (APAC) region (53%). In FY18, Indian Agrochemicals performed better than FY17 due to a good monsoon.

-

Global Chlor-Alkali market is expected to grow at a CAGR of 5.3% to 5.9% to reach $125 bn by 2023. Increased exposure of different end-user areas, such as Glass, Alumina, Vinyl, and Water treatment etc. are expected to boost demand. The Indian Chlor-Alkali Industry is poised to grow at a CAGR of 6.5% during 2017-2022. Major consuming industries are Soaps & Detergents, Pulp & Paper and Textile processing. The fact that products of Chlor-Alkali industry find increasing use in daily products shows the potential for growth of this industry.

Risk due to Interest rate change is given in page 196 of AR in consol FS notes which as per simple mathematical calculation, rise of 100 bps i.e 1% in interest cost could impact Rs. 304 Lakhs as P&L hit and Rs. 199 L as hit in reserves in other equity.

Another risk of forex exposure, in page 195 indicating strengthening of USD by 3% could impact the P&L by Rs. 98 L and Rs. 64 L hit in reserves.

Both the above are as at 31.03.2018 numbers. Hence due to the above change, the hit in P&L in consolidated numbers during FY 18-19 could be about Rs. 500 Lakhs in P&L and Rs. 300 L in equity.

Both put together is 3.36% to FY 17-18 PAT and may be around less than 2% of FY 18-19 PAT. Which should be manageable and not much of concern

In page 129 and in page 201 of AR, in events occuring after balance sheet date, it is mentioned that the company through its wholly owned subsidiary meghmani agro chem pvt ltd has acquired shares of 24.97 % meghmani finechem Ltd which is their caustic soda business.

During FY 17-18, the profits attributable to non controlling interest in their consolidated P&L was of Rs. 6660.53 L which is 42.84% of meghmani finechem (see page 198 of AR). Out of this 24.97% or 42.84% will further get added to the PAT of Meghmani Organics, which at FY 17-18 P&L is Rs. 3882 L which is more than 15% of PAT of FY 17-18. Thus for FY 18-19, due to this acquisition, the PAT will go up by about 20% which is very positive.

Hi Kush,

The above info is culled from AR 2018 which is avlble in the previous posts. Latest shareholding as on 30 6.18 is yet to be published.

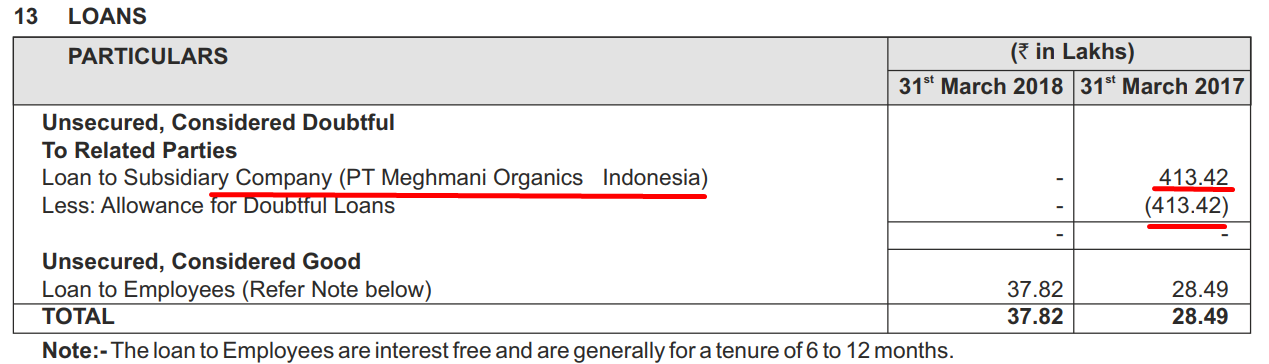

Nothing serious , I observed the company has given Loan of 4.13Cr to its subsidiary(PT Meghmani Organics Indonasia) and now it have put that in Doubtful loans and given provision, Why this loan is doubtful, is the company not able to recover its money from its own subsidiary(Is it allowed)? And why they are giving loans to the employees at Zero interest?(Given in foot note)

1 Like

The subsidiary was opened in Indonesia way back in 2009 for distribution of its branded AGro products. In such Market development initiatives, In order to penetrate a new market usually companies supply the distributors with some minimal inventory/goods with long credits and/or “pay as you sell” model. The parent usually loans the subsidiary some money which is sued for buying minimal inventory and marketing expenses. Quite often these initiatives fail (because of competition/poor performance of sales employees etc).

http://equitybulls.com/admin/news2006/news_det.asp?id=61274

For second point: Its practice in many good companies to provide short term loans (interest free) as prudent HR practices. At Least they are not like ESOPS which are EPS dilutive and have significant impact being perpetual and high terminal value.

7 Likes

The Q1 Result will release on 8th Augest.

Need help in understanding the below:

As per my understanding, the pigments & agrochemicals segment is under Meghmani Organics Ltd. (Standalone) & Bulk Chemical segment is under Meghmani Finechem Ltd (Subsidiary)

As per Management, the current 640 crs capex plan is for caustic soda & hydrogen peroxide (500 crs) + CMS (140crs) businesses all housed under MFL.

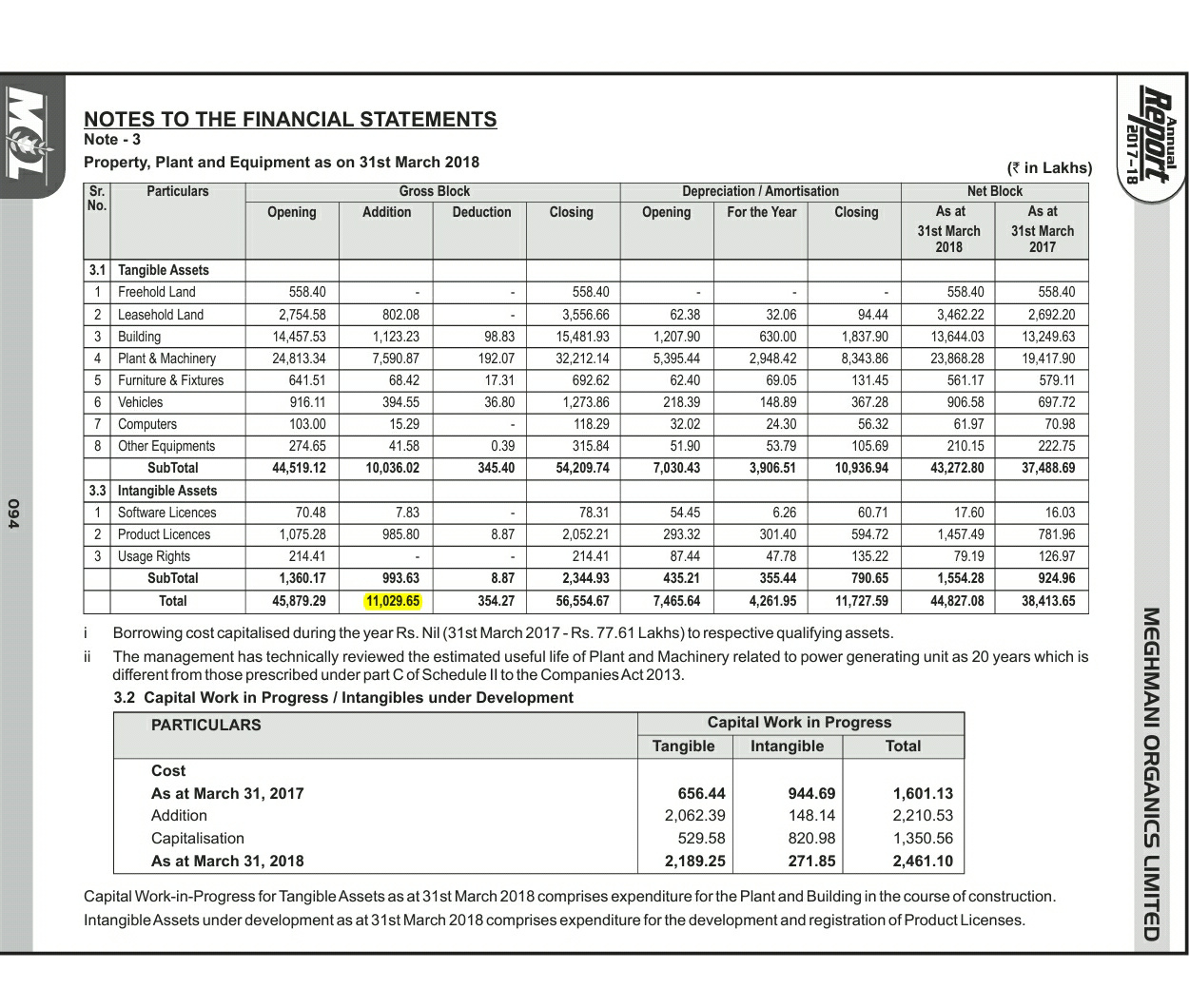

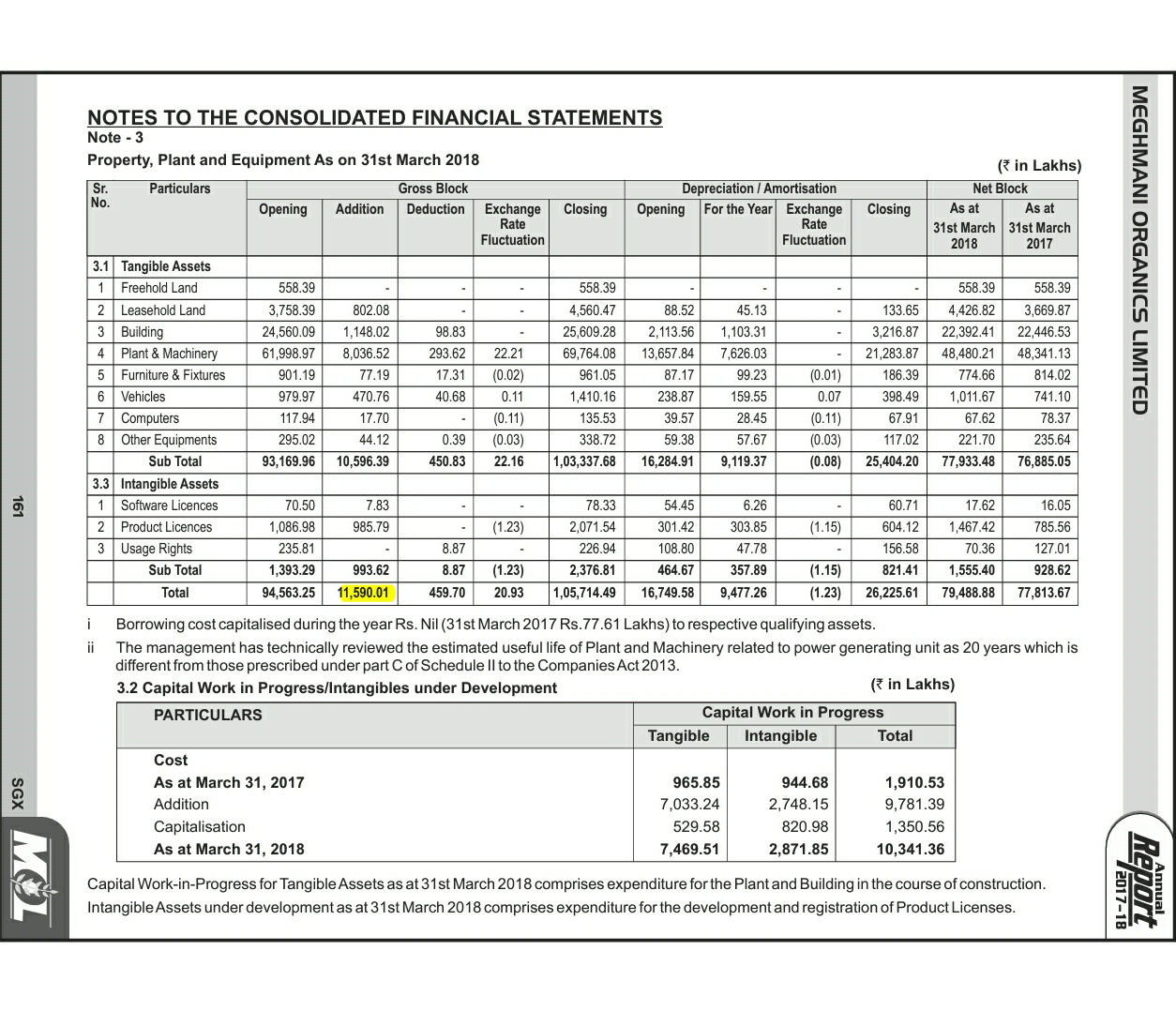

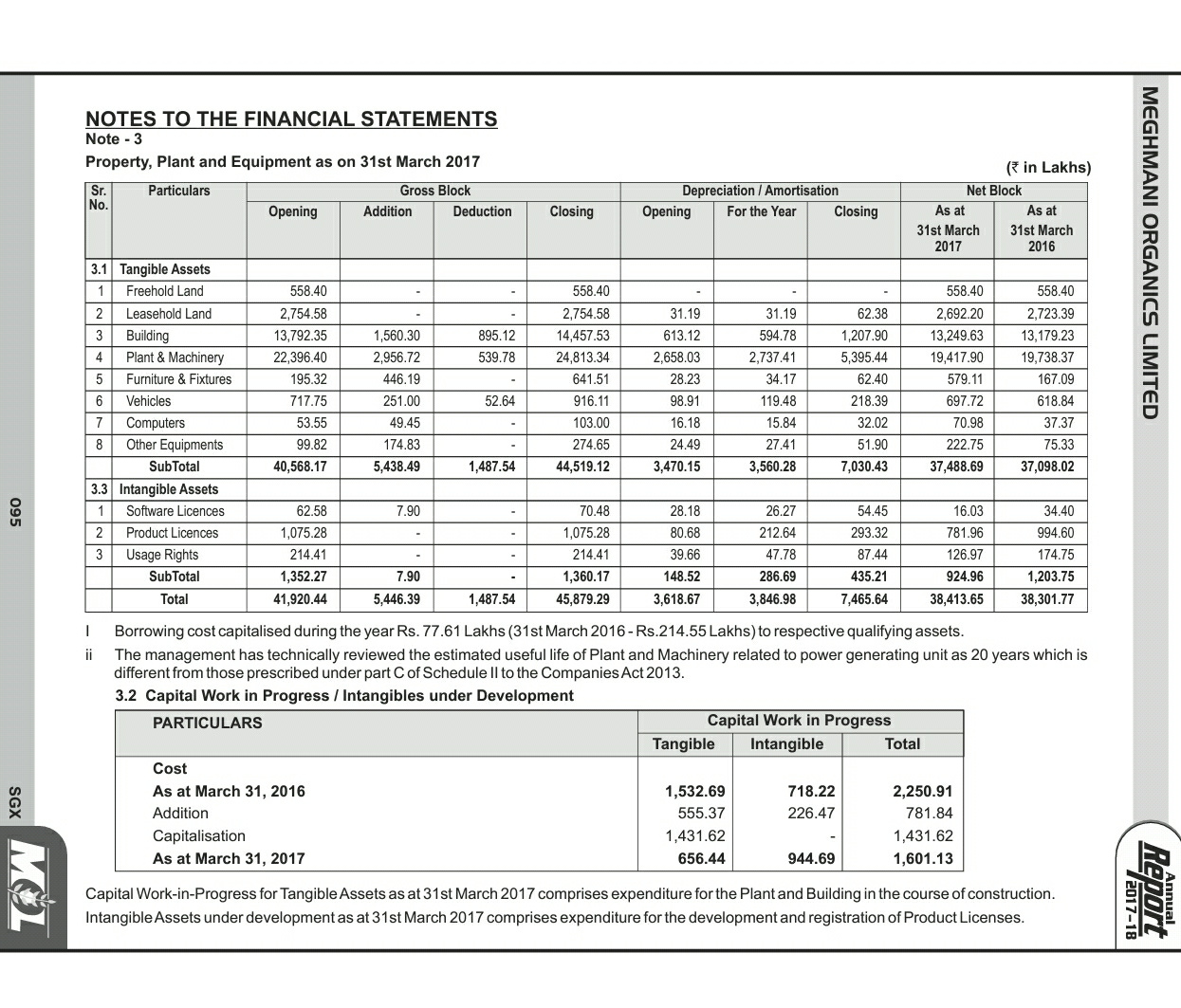

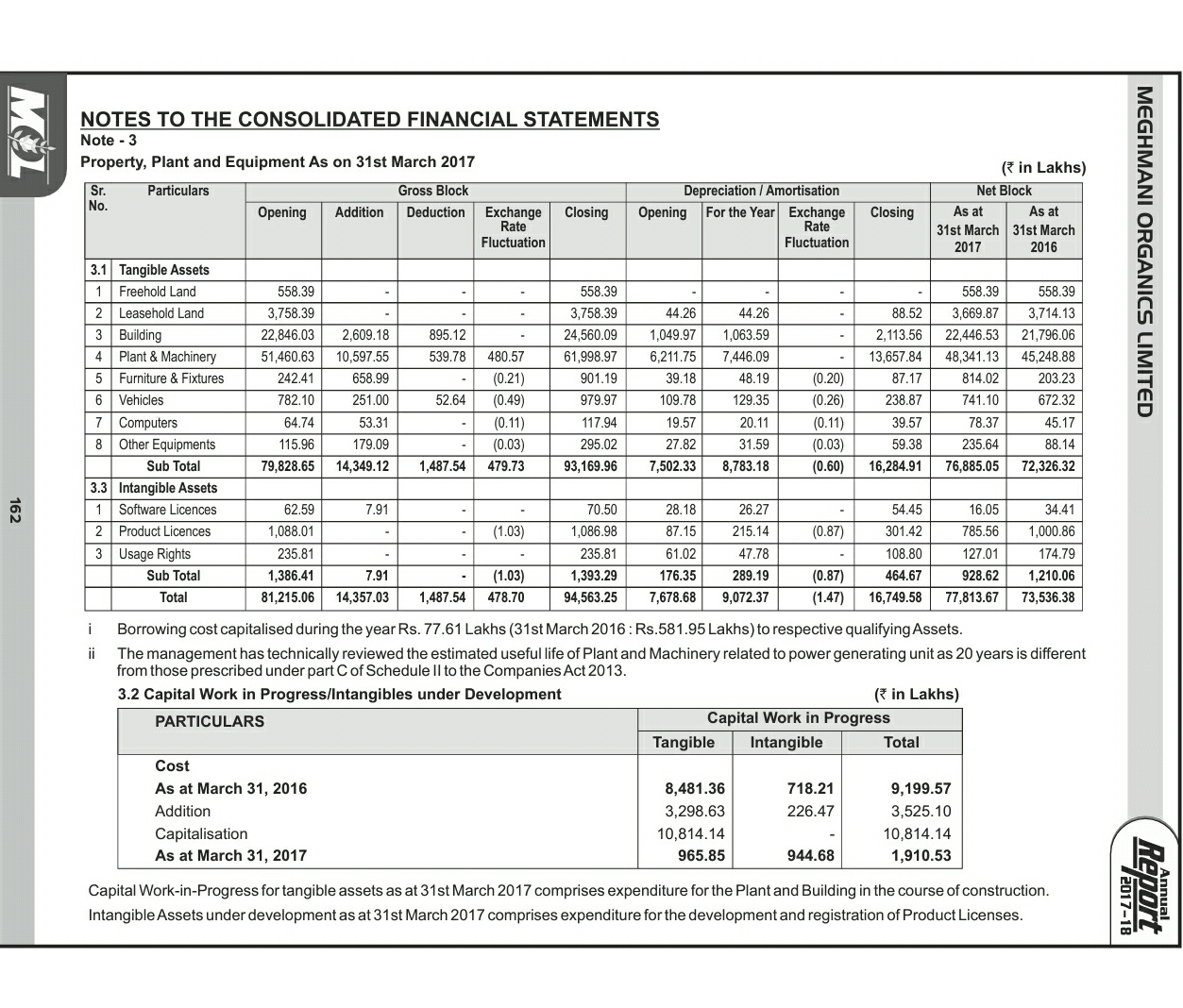

When I look at the FY 18 AR — under MOL standalone financials there is addition of 110 crs in the gross block & under consolidated financials the addition is of 115 crs.

For FY 17 the capex is 54 crs in standalone books and 143 in conso books

What I am not understand is that if the capex plans are for the bulk chemicals division (MFL) then why is there so much capex being done in the standalone company and practically no capex in the subsidiary in FY18.

Can there ever be a case where the capex for a subsidiary can be done in the holdco?

Please correct me if I am wrong somewhere.

Q1 Results

The next board meeting of Meghmani Organics is to be held on August 8, 2018 for Quarterly Results

https://www.moneycontrol.com/company-facts/meghmaniorganics/board-meetings/MO04#MO04

1 Like

You can refer following thread on various Chemical prices, which includes Caustic Soda as well

I did search to find out immediate competitors of Meghmani organics in moneycontrol looks like it’s giving almost all the chemical companies list where as i’m intrested to find out the immediate competitors of Meghmani and the business advantage of it’s peer’s. Any idea’s/help would be appreciated.