Promoters haven’t paid the money, MOL has! So shareholders have paid 52% of 221 crores (in line with their ownership of the company).

1 Like

Where can we find this information?

1 Like

PROMOTERS DESERVE A STANDING OVATION FOR THE BRILLIANT RESTRUCTURING

(WHO CARES FOR THE MINORITY SHAREHOLDERS !!)

(this is my assessment of the restructuring; have taken some data from ROC; willing to be proven wrong)

The promoters of Meghmani deserve a standing ovation for the brilliant restructuring they have undertaken along with their Big 4 Advisor.

Briefly, Meghmani Organics (MO, a listed company) owned 57% in a subsidiary Meghmani Finechem (MFL), IFC Washington owned 25% in MFL and the rest 18% was owned by the promoters of Meghmani in their individual capacity. The restructuring results in giving an exit to IFC of Rs 221 crore, the ownership of MO in MFL remains at 57% while the promoters stake in MFL goes up from 18% to 43% from thin air with the promoters hardly putting any of their own money in the restructuring. The only funds they put in is to buy some stake in MFL is at a HUGE discount. SIMPLY BRILLIANT.

Lets look at the steps taken to attain this (calculation is confusing so details given in the end).

-

In 2008, MFL is formed with stakes of 57% by MO, 25% with IFC Washington and rest 18% by the promoters in their individual capacity.

-

In 2018, an exit needs to be given to IFC of Rs 221 crore. Ideally, one of the following should have taken place

a) MO pays Rs 221 crore to IFC and acquires their 25% stake. MO’s stake in MFL should increase from 57% to 82% while the promoters stake remains at 18%.

b) Promoters arrange Rs 221 crore and buy IFC’s stake. Promoters stake in MFL increases from 18% to 43% while MO’s stake remains at 57%

c) MFL buys back the equity stake of IFC. Shares owned by IFC are extinguished and equity stakes of BOTH, of promoters and of MO, in MFL goes up.

-

But there were other plans. Objective is to somehow increase the promoter stake in MFL with promoters hardly putting in any funds from their own pocket while keeping MO’s stake the same at 57%

-

In April 2017, a new company Meghmani Agro Chemicals (MACL) is formed as 100% subsidiary of MO. MO invests Rs 109 crore as equity in this company.

-

In October 2017, a Share Purchase Agreement is signed between MO and MACL to acquire a part of MO’s equity stake in MFL. This is being done so that after the restructuring, MO’s stake in MFL remains at 57% (will explain rationale later).

-

26th April, 2018: Promoters are allotted 50 lakhs new shares of MFL at Rs 30/share (allotment details attached).

-

27th April 2018: MO invests additional Rs 221 crore in MACL as Redeemable Preference Shares. This money is to be used to buy IFC’s stake by MACL.

-

28th April 2018: MACL acquires IFC stake of 25% in MFL for Rs 221 cr (Rs 125/share) (details attached)

-

It is now proposed to merge MACL and MFL. Shares held by MACL in MFL will get cancelled.

-

Post merger of MFL with MACL, MO owns 57% of MFL while promoters now own 43% stake (detail working below).

-

For the shares of MFL owned by MACL prior to the merger and which get cancelled on merger, MFL will pay Rs 211 cr 8% Optionally Convertible Preference Shares over 10 years.

-

It will further repay Rs 221 cr immediately as Non-Convertible Preference Shares for the funds it got as Redeemable Preference Shares to buy IFC’s stake.

ISSUES

-

Is it legal for promoters to buy shares in MFL at Rs 30/share when the book value of the shares is Rs 65/share? Not just that, two days later (on April 28, 2018), IFC sells its stake in the same company at Rs 125/share. The promoters make cool Rs 47.5 cr profit on their 50 lakh shares. Even though MFL is a private company, it’s majority owner is MO which is a listed company so all norms of valuation cannot be ignored.

-

Even if it is legal, is it ethical for the promoters to buy shares in MFL at Rs 30/share when two days later, IFC sells the shares of the same company to MACL at Rs 125/share?

-

The Rs 221 cr being paid by MFL to MO as Non-Convertible Preference Shares is anyway owed to MO for the Rs 221 cr it injected into MACL for purchasing equity of IFC.

-

Thus compensation for shares owned by MACL in MFL which are getting cancelled on merger is only Rs 211 cr being paid as Optionally Convertible Preference Shares. But shares owned by MACL in MFL are 3.45 cr shares which are worth Rs 431 cr based on IFC’s valuation of shares at Rs 125/share.

The best way forward is for the company to withdraw the merger scheme from NCLT. Let MO own 77% of MFL while promoter own 23% stake (promoter stake has gone up from 18% to 23% as they have been allotted 50 lakh fresh shares in MFL).

The promoters are being short sighted if not outright greedy. If the merger is cancelled, they any way directly and indirectly will own 61.5% stake in MFL (promoters own 50% stake in MO so indirectly will own 38.5% stake in MFL and 23% directly). With the approval of scheme, they will own 28.5% indirectly though MO and 43% directly i.e total 71.5%. Thus all this mess just to own an additional 10% stake in MFL. Clearly not worth it.

Some argue that MO should not be in a cyclical business of MFL thus should not increase stake in MFL beyond 57%. But that can be handled by listing MFL separately (no IPO needed) with shares of MFL given to existing shareholders of MO. After listing of MFL, let investors then decide whether they want to hold shares of MFL or sell them.

Another argument of promoters buying shares of MFL at Rs 30/share when IFC stake is bought at Rs 125/share is that promoters need to be compensated for bringing IFC in MFL, the risk they have taken in MFL and for building the business. But the majority owner of MFL for the last 10 years has been MO with its 57% stake while the promoters have only owned 18% directly these 10 years so majority of risk has been taken by MO and not the promoters. There is also a view that the right to buy MFL shares at Rs 30/share was given to the promoters in 2008 itself. But it is blatantly unfair to be given such a right.

It may not be wrong to say that Meghmani has become MAKE MONEY, but only for the promoters.

DETAILED WORKING

-

MOL owned 4.04 cr shares in MFL.

-

MOL forms MACL as 100% subsidiary. Injected Rs 109 cr as equity capital (Page 129 in the FY2018 balance sheet)

-

MOL transferred 1.69 cr shares of MFL to MACL for Rs 109 cr (at book value Rs 65/share). Consideration of Rs 109 cr paid to MOL through the equity injected in MACL. (Page 129 in the FY2018 balance sheet)

-

Promoters allotted 50 lakhs shares in MFL at Rs 30/share. Total equity shares of MFL increases from 7.08 cr shares to 7.58 cr shares (details attached)

-

MO injects Rs 221 cr into MACL as redeemable preference shares. This money is used to buy 1.76 cr shares from IFC at Rs 125/share. (mentioned in notes of half yearly Sept 2018 results) (attached)

-

Merger of MACL into MFL in progress. Shares of 3.45 cr of MFL owned by MACL (1.76 cr bought from IFC and 1.69 cr bought from MO) will get cancelled.

-

Post merger, equity of MFL will be 4.13 cr shares (7.08+0.50-1.76-1.69) cr shares

-

MOL will own 2.35 cr shares (4.04 cr it owned initially - 1.69 cr it transferred to MACL which get cancelled on merger) ie. 57% in MFL

-

Promoters own 1.76 cr shares in MFL (1.26 cr shares they owned initially + 50 lakhs allotted on April 26, 2018). ie. 43% stake in MFL

Meghmani 28 April 2018 IFC exit.pdf (286.3 KB)

Scheme Details 27th Oct 2018 clarification.pdf (296.4 KB)

MFL 26th April 2018 Share Allotment to promoters.pdf (367.8 KB)

Meghmani Sept 2018.pdf (881.8 KB)

47 Likes

Good work. …

Best thing is to get out of such company on every rise.

One small correction 1.69 crores of shares are transferred from MOL to MACL for which 109 crores are getting paid at a price of Rs 65/- per share and 1.76 crores of shares that were held by IFC were bought by MOL through MACL. In total Shares of 3.45 cr of MFL are

owned by MACL (1.76 cr bought from IFC and 1.69 cr bought from MO) will get cancelled. How much are they paying for these 3.45 crores shares - (211+109) crores = 320 crores i.e., Rs 92.75/- per share.

Kindly correct me if I’m wrong.

I did some simple calculation step by step and my analysis says that there is not much issue. The complication seems to be due to so many conditions and transfers of shares and money. Let me try to explain. I may be completely wrong over here, but please me if there is any error.

I may not take MACL’s role into consideration, because according to me has just acted like a middle man.

Lets talk about MOL and MFL only.

-

221 cr loan has been given my MOL to MFL, that would be returned by MFL at 8% interest in 2019. We all have no doubt in this.

-

Share allocation before allocating 50 lakh shares of MFL to promoters:

MFL has approx. 7.08 cr shares with valuation of 885 crore. i.e. per share at 125.

| Entity | IFC | MOL | Promoters | Total |

|---|---|---|---|---|

| Percentage share in MFL | 25% | 57% | 18% | 100% |

| Number of shares (approx…) | 1.76 crore | 4.04 crore | 1.27 crore | 7.08 crore |

| Value (approx…) | 221 crore | 504.45 | 159.3 crore | 885 crore |

- Now IFC is to be exited post which 50 lakh shares are to be given to the promoters at 30 Rs. Per share. So 221cr was paid to IFC.

So 1.76 crore share from IFC is available.

So after adding 50 lakh shares the per share price would be RS. 116.75 and the new evaluation would be like this:

| Entity | (shares of IFC after exit) | MOL | Promoters | Total |

|---|---|---|---|---|

| Percentage share in MFL | 23.22% | 53.29% | 23.35% | 100% |

| Number of shares (approx…) | 1.76 crore | 4.04 crore | 1.77 crore | 7.58 crore |

| Value (approx…) | 205.5 crore | 471.69 | 206.66 crore | 885 crore |

15 crores cash from promoter to MFL is also available (for the 50lkh shares @ Rs. 30 per share)

It is obvious that if 50 lakh shares are to be given to promoters the valuation of other shares would go down.

(it is a debatable topic whether giving 50 lakh share at 30Rs is ethical or not. However as the promoters claim, it is as per the agreement which was signed at the time of formation of MFL.)

- Now MOL has decided that it will not increase the percentage share in MFL more that 57%. So the question of dividing the shares worth 205.5 crore between MOL and promoters is out of question. So lets keep this 205.5 crore + 15 crore aside as cash.

| Entity | MOL | Promoter | Cash or cash equivalent | Total |

|---|---|---|---|---|

| Percentage share (approx…) in MFL | 69.53% | 30.47% | NA | 100% |

| Value (approx…) | 471.69 crore | 206.66 crore | 205.5 crore+ 15 crore | 885 crore |

In order to MOL have only 57 % we have to decrease the value of MOL:

| Entity | MOL | Promoter | Cash or cash equivalent | Total |

|---|---|---|---|---|

| Percentage share (approx…) in MFL | 57% | 43% | NA | 100% |

| Value (approx…) | 386.66 crore | 291.69 crore | 205.5 crore+ 15 crore | 885 crore |

| Comment | Value decreased by 85.03 crore | Value increased by 85.03 crore | Total cash is 220.5 crore |

This means promoter now owes 85.03 crore to MOL.

- Now what to do with the total cash or cash equivalent of 220.5 crore. The ownership of this is in the ratio of 57% with MOL and 43% with promoters

Owner ship of 220.5 crore

| 57% with MOL | 43% with Promoter |

|---|---|

| Value: 125.685 crore | Value: 94.813 crore |

So Ideally MOL should receive 85.03 crore from promoters and 125.685 crore from MFL. Which is approximately 211 crore.

Promoters would pay 85.03 crore from the 94.813 crore available.

And finally after the deal promoters would still have 9.78 crore cash.

Please note: I am a novice and not an accounting expert. So I have tried to calculate everything by doing some simple additions and subtraction. And based on this I do not find any ethics issue over here.

Please let me know if I have done any mistakes in calculations.

1 Like

Duranvskp, it does not matter at what price MACL bought the 1.69 crore shares from MO since the shares and the money moved between MO and its 100% subsidiary MACL. An analogy will be ‘if you have a pencil in one hand and money in the other hand, it does not matter what price the right hand paid the left hand for the pencil since both will ultimately remain with you’.

The Rs 109 cr injected as equity in MACL was paid back to MO on acquisition of MFL shares. See page 129 of the 2018 balance sheet.

So even though the transaction between MACL and MO happened at Rs 65/share, the actual market value of those MFL shares remains Rs 125/share (value at which IFC sold its shares).

2 Likes

I think you already assumed that the ownership changed to 57% and 43% , subsequently you are divinding the assets accordingly. At the time of transaction , ownership percentage would still be 69.53 and 30.47. So my understanding would be that you would need to divide assets by that much. You would see numbers change if you do this. Ownership would chnage to 57% and 43% only after the transaction happens, not before the transaction.

On a lighter note, the promoters made a cool Rs 47.5 crore notional profit when they acquired shares of MFL at Rs 30/share. They can afford to splurge a bit of that gain in increasing their holding in MO.

1 Like

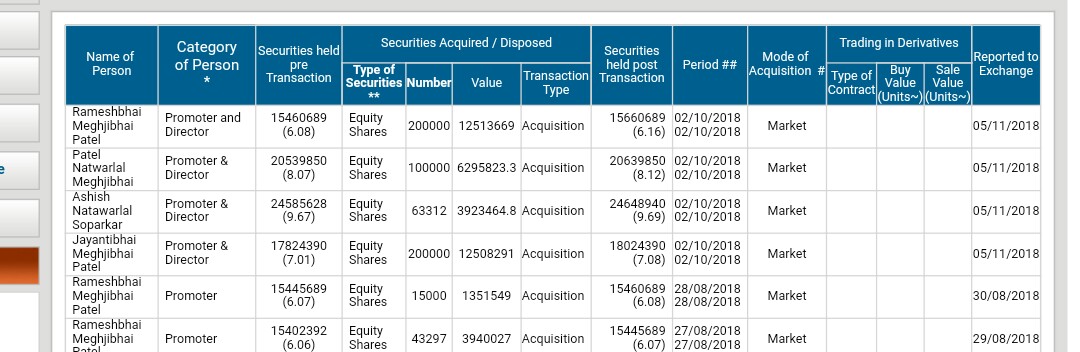

It was acquired in the period of 02/10/2018 - 02/10/2018. The same was reported to exchange today.

Promoters didn’t acquire today. Not sure why they didnt report this for almost a month. I see companies usually report this anywhere between than 3-10 days usually.

Did they know this problem coming and waited to use this message to push the beaten price ?

I think it is typo since 2nd October is a national holiday as well as trading holiday. I think they bought the shares on 2nd Nov.

1 Like

You are right. 02/10 is a holiday. I’m not sure about this transaction or typo. Just posted the observation

If total valuation is 370 crore and promoters 43% comes to 159.1 crore, then MOL stake (57%) should be valued at 210.9 crores (370-159.1). In effect, MOL should be paid 293 crore. No?

Do let me know if i have missed something.

The analyst call happened on 31st Oct and CNBC interview on 1st Nov. check what was said on 12th min in the call and 8th min on CNBC interview that NCLT approval is pending. Check NCLT Ahmedabad site and check for a order on 24th Oct 2018.

1 Like

Most of the people are looking at the current payment. This may be slightly flawed, IMHO. MFCL (MFL) is the unlisted company where most of the expansion is happening. Estimate the future sales and profits numbers to arrive at the valuations and then discount them to arrive at the suitable price. This should be added it to whatever payments that you are considering for the current capabilities of the company. Feel free to correct me if I am wrong.

Valuation analysis in companies/groups where decisions may be taken to shortchange minority shareholders hold little meaning. I don’t think anyone had an idea that a restructuring will be undertaken wherein promoter holding in MFL will increase from 18% to 43% with them hardly injecting any fresh capital. And that poor parent MOL will be left holding the same 57% shareholding in MFL.

On top of that, I don’t think anyone had an idea that promoters have warrants of MFL which will convert into shares at Rs 30/share (This was the pricing at which MOL, IFC and the promoters had injected equity in MFL in 2008 when the company was started!!). And one is not even sure whether promoters have more such warrants left to be exercised (if yes, then MO’s stake in MFL will go down further when they are exercised).

3 Likes

Such an informative discussion, I have a doubt, apologies if it’s too silly.

MFL has to pay 221 CR to MOL with8% interest in March 2019.

And 211 cr with 8% interest with in 10 years

My doubt is this can be paid from loan/debt or from their profits right?

If from MFL profit , 57% of net profit is still owned by MOL right?

Or if from debt, still MOL is also liable for 57% of that debt right?

Please correct me if my thought process is wrong

Q2 FY2019 conference call transcript:

http://www.meghmani.com/inv_rel/misc/Q2-FY19-Earning-Conference-call.pdf

The repository URL is:

1 Like

What a bunch of thieves these promoters are. It was cringeworthy going through the transcript. They did not give a straight answer to any single question asked on the whole MFL MACL thing.

Shouldn’t this be raised to SEBI and doesn’t this warrants strict actions to be taken against promoters??

4 Likes