This company is one of the scrips where i am waiting to take position and average in this market correction…

I already have a minuscule allocation to it as a disclaimer…

SO in this regard, i am saving my notes about the company in this thread…

Addition and criticism requested from all members…

the company is involved in pvc leather segment mainly, with planned expansion into polyurethane leather as well…

PVC segment caters to the following industries…

1.footware 2.automotive oem and replacement market 3.furnishing 4. apparels…

Traction in the footwear segment with 15% CAGR between FY12 and FY16 led to significant volume growth in MUL’s footwear segment. Demonetisation and GST implementation

in FY17 led to muted growth in the footwear industry.The management is of the view that the growth opportunities and value addition is more in the auto space and it aspires to explore that more , rather than footware segment whose growth is projected to remain stagnant to moderate… the unorganized sector in foot ware which continue to constitute 70-75% of the market share , continue to be competitive even post gst…

The customers that the company caters to in the foot ware segment are-BAta , Relaxo, PAragon, Liberty, Action and VKc…

The disruption impact that GST has had the most is in the furnishing segment, as this is a B2C business and this might take some time before growth can be expected…

Nevertheless, the company has expanded distribution in the furnishing segment in delhi, surat, chennai, indore and kanpur in fy18…

The automotive segment continues to be projected as the growth driver in the mix, where the customers are all the well known auto brands were are familiar with…synthetic leather is the main key raw material in the automotive seating industry.the customers in the auto sector are either throguh auto OEM or the auto replacement dealers[the pricing power in case of replacement is higher as it is a sector which is driven by design innovation] .In this regard the company has planned and in the process of execution of a Mysore plant expansion, where there is strategic value addressal regarding the auto sector mainly… the customers which they supply are mainly concentrated in the south, so supplying from the jaipur plants has 2 main issues, 1.freight costs and 2. transit time [typically 1 week now, to reduce to only 4hrs], both of which can be mitigated by starting production line in the south- not only the business volumes have more potential to grow, but also scope for margin improvements as the costing includes the freight charges…

the export market in the autospace is also a focus of the management where there is better value adding than domestic, plus with a depreciating rupee can help to offset the raw material pricing pressure…

In terms of market share in the auto seating space, the domestic oem market is sized at 33million linear meters annually of which mayur has 9% share, the domestic replacement market is sized at 49million linear meters, mayur has 16% share and in the auto oem export market which is sized at 122million meters mayur has only 2% share…

the jaipur pvc plant-

situated in jaitpura and dhodsar ,rajasthan

installed capacity- 3.05 million linear meters/ month

includes 6 production lines

capacity utilization - 85% [max possible 94%]

Machinery for the 7th line has been ordered already, adds 0.5million linear meter/month , which is planned to be installed in q2-q3fy20 …

the mysore pvc plant-

land acquisition pending [to be completed within expected 7-8months]

planned capacity 0.1 million meters/ month [1 line as of now]…

Planned expansion to total 5 production lines, as of now, machinary for one line is planned to be transferred from the Jaipur plant and rest as growth and demand picks up, transferring of the machinery will take another 2 months … mysore plant is expected to come online by fy21…

The Mercedes opportunity-

Mercedes had 2 synthetic leather suppliers Hornschuch and Benecke-Kaliko. In June, 2017, Hornschuch was merged with Benecke by the parent company Continental to form Benecke-Hornschuch Surface Group, leaving Mercedes vulnerable to a single-source for its synthetic leather supply.

MAyur was on in consistent attempt to grab the opportunity here since FY14, it

is only post the Benecke-Hornschuch merger that Mercedes has started working toward this direction…Mercedes has already conducted 2 rounds of VDA standard inspection in mayur’s facilities invAugust and November, 2017. the November audit composed of 9 membered team from germany conducted the process for 3 days and issued a yellow signal indicating requirement of a few modifications [only on operational front].the management expects the next round of inspection in Sept-Oct 2018, which is going to be the final inspection. The management expects orders to come in after 3-4 months of approval.

The management hesitates to mention the opportunity size in numbers, in q1 fy18 concall Mr.BAgaria mentions it as “huge”, but in one instance a figure of 150-200cr of revenue generation within 2 years of operation was mentioned to be possible by MR. S.K Poddar starting with 5-7% of the current topline [roughly 30 to 40cr of additional topline to start with]… the ebitda potential is 40% in this venture…

What this Merc venture does for the company is it opens up the door to European export market specially the luxury segment- other 2 major VDA member carmakers BMW and

Volkswagen.

capex planned in the pvc segment in fy19 is 35-50cr.

In us auto export segment 5 new projects are being examined where mayur is scheduled to send sample for testing with customers such as Forde and Crysler , for which the management is hopeful to generate orders soon…

post these export order acquisition , the export revenue can form 35% or more in the mix…

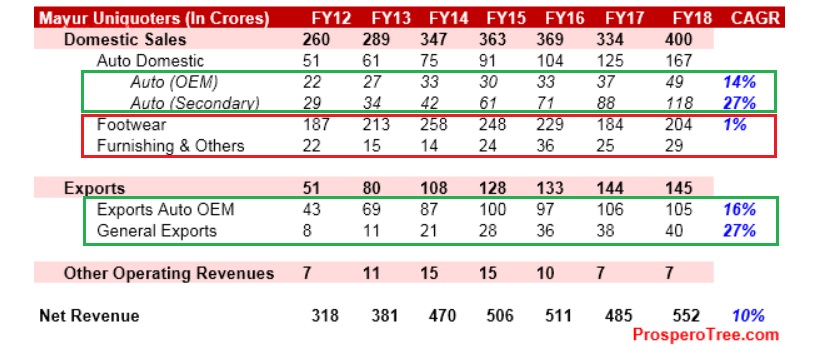

HIstorically, the comany changed its product mix by increasing share of exports sales from 17% to 27% in overall revenue between FY12 and FY18

the indian synthetic leather market is 50% comprising of organized players including Jindal Coaters, HR Polycoats, Polynova industries, Jasch Industries, Royal cushion venyl products ltd, MArvel ltd. The organized player market share has increased by 10% in last 5years, while mayur’ domestic sales grew 100.6%, from 254.25cr[total-317.39cr, export-17%] to 404cr [total-552.22cr, export-27%]

The Pu opportunity-

Globally the synthetic leather market is expected to grow at a cagr of 4.2% from 36.2 billion usd to 56.3 billion usd from 2017 to 2027

Amongst which the Pu leather industry [highest growth expected]is expected to grow at 7.5% cagr from 2017 to 2025 according to reports. Globally, the main growth driver in this segment is the penetration into the auto industry…Grabing the overall market share from Ethyl venyl acetate [EVA] and Poly venyl Chloride[PVC]…

In india 95% of the Pu leather consumption is import source driven, China forming majority of the supplier.Pu has certain disadvantages where the most important one is the shorter life span of Pu compared to Pvc and fast disintegration on storage if the quality of the material is not up to the mark.With high possibility shift of the leather preference from PVC to PU where ever applicable, the main challenge for the OEM and dealers is to maintain inventory in Pu .The chinese suppliers do not guarantee the quality of the supply and the businesses are reluctant to foray into the Pu segment as yet due to this issue…This is a situation Mayur believes they can exploit , not only grab the import market share but also assure quality to the customers… Mr.S.K.Poddar once in a recent call mentioned they are even attempting to address the DGAD to impose duty on Pu imports from china…

Pu leather is used in auto space [can act as a replacement option to pvc] and also footwears , but here the outersole is made up of pu and the insole of pvc leather…

Coming to the plant…

the plant has been planned at Gwalior , MP for which the land has been acquired, no environmental clearance has been required as this is a purchase of gov land…the machinery has been ordered [imported from china ironically] and the production is scheduled from 1st april 2019… CApex plan-100cr [70cr in fy19] [20% financing from debt]

the land acquired can accommodate maximum 5 production lines, construction is underway for 2-3 lines and they plan to start with 1 line with a capacity of 0.4 million liner meters/month…

for EBITA breakeven they believe 1 line’s full capacity utilization annually will be sufficient …

on an average each line has a potential to generate roughly 120cr of revenue…

with a maximum revenue generation possible from this plan being 500-600cr annually at full capacity in about 5 years time…

The margins in the Pu busniess which can be expected has not been mentioned my the management and they feel initial 1-2years there might be drag on the gross margins until they grab significant market share in this space …

the pvc-pu dilemma in the long run - with paradigm shift from pvc to pu leather, domestically there is a dynamics that is confusing to me… The unorganized sector is shifting to pu already which allows organized players to grab more market share in the pvc space, yet, the overall industry is actually shifting towards pu as a preferred synthetic material for leather…the again the management mentions in the long run, the pvc segment of their business is not going tobe disrupted as they believe there is significant demand growth still possible in the pvc auto space mainly.Where as the customers in the organized space in the pu segment would be more into quality of the product hence the competition form the newly shifting unorganized pu industry would be a worry for mayur’s foray into the pu business…

Margin and Raw materials-RM- 1. majority is chemicals 65% , of that pvc resins constitute 40-50%- all are heavily crude dependant…

2.Fabric- 30% mayur has a backward integrated unit to source this portion of the raw material and plans to expand the unit to match the increased production volumes …in addition to loweer input cost this backward integration led to a reduction in product development time from 2-3 months to 3-4 weeks.

3.release paper- 5% reusable

With crude the chemicals portion of the raw material has definitely firmed up to the tune of 26% in past fy18…

FRom mid june reliance has further hiked pvc resin prices by rs.1000pmt

[a good source to track the resin prices

292 Ril Revised Prices – Resin Agency Llp]

In comparison the company failed to pass on the raw material price hike to the customers in the auto segment throughout the year and all other segments in most part of the year, the last price hike was about 5% back in april, 2017 that too only to the footware industry…

in export segment rupee if remains depreciated can offset the RM price hikes…

Quite surprisingly, inspite of the inability to pass on the RM price pressures, the company maintained the EBITDA and the PAT margins with stability…The management attribute this to their prudence in doing business mainly in regard to the product mix which held the margins to stable state…

This year how ever further increase in raw material prices and the depreciation coming in the next financial year form the 2 new plans, would definitely put pressure on the PAT margins even more…

No plans have yet been disclosed to do further price hike as of now…

Then again, after the mysore plants comes operational and the export orders from europe and us gets added to the mix along with the knitted fabric capacity to meet rising volumes, have the potential to have positive impact on the margins fy20 onwards…

Topline-

Revenue split fy17 vs fy18

export sales- 144cr vs 148.22cr

export volumes- 40 lac meter vs 42.77 lac meter

export split-

fy17- auto oem-106cr and general export-38cr

fy18- auto oem-108.47cr[22.26lac metre] and general export-39.74cr[20.51lac metre]

domestic revenue split-

fy17- auto replacement+OEM-120cr , footware-180cr , others-76.3cr

fy18- auto replacement-117.35cr[80.13L metre] autoOEM-49.28cr[26.43L metre] [auto total-166.63cr, 39% growth yoy] , footware-208.35cr[94.92L metre, 15.75% growth yoy] , furnishing-10.02cr[6.09Lm]others-19cr[23.26Lm]

total production volume[E+D]=273.59Lmetre

MAnagement guidance of gross volume growth of 10-15% in fy19 with no coment on the margin expectation…

Risks to note-

The competition form the unorganized players and the chinese imports remains key risk of gaining market share at reasonable margin of operations in the pu business…

The pu plant was earlier expected to start operations from fy19 itself, which has now been delayed due to mainly strategic reasons to fy20, further delay might occur

THe pvc plant at mysore is still a year atleast to get started, the land to be still acquired which already the company mentions atleast 7 months are required, then there are transportation of machinary from the jaipur plant, operation startup might be delayed again due to any reason in the whole process , should be kept on radar

the rising resin prices on the back of crude is a concern , while at the same time the inability to pass on the RM pressure in the domestic market

THe rupree if starts appreciating might lead to further pressure on the export margins…

Mr. Suresh Kumar Poddar already 70yr plus age, whos position to be taken up by the son in law in future may be, since the son manav poddar has resigned from the board after a span when rumors were going on regarding rift b/w the promoters…the son in law, Mr Arun Kumar

Bagaria B.Com. (Hons)& MBA from University of Strathclyde

Graduate Business School, UK & has been in the company since 2007.

Another key personnel is Mr. Ramdas Acharya [senior VP tech. div.]who is also 70yr old with 30 years’ experience in the US synthetic leather industry, specializing in the automotive OEM Segment. Ex company – Uniroyal Engineered Products.Chemical Eng.,Msc. , MBA from

Michigan StateUniversity, USA

There is definite risk regarding future key person with significant experience about the industry…

The final audit of Mercedes in H2 this year, is significant, disapproval will not only set back the growth opportunity that is being sought, but also will deter the potential approach to other customers in the european auto space at least in the short to medium term.

Overdependance on auto[increasing now] and footwear space.

The potential foray into the Pu leather industry , the cash cow in the form of mercedes orders and open up of the European auto leather industry , further exploit of the southern market scene via the new mysore plant , more backward integration with the fabric unit and further expansion in the pvc production lines, projects mayur into the next phase of growth… Possibly materializing from fy20 onwards with a fy19 topline growth expectation of 10-15% and observation period where in the progress on the new plant and the final merc audit results…

The market seems to be factoring in all the growth and has a chart where there are signs of wyckoff reaccumualtion and the start of the wave 3 within a wave 3 of the Elliott waves…

the technical picture has been posted in the TA thread…Bull therapy 101-thread for technical analysis with the fundamentals - #304 by Capsule91

Disclaimer… invested, planning to allocate 10percent of the portfolio to this stock on correction…