Outcome of Board Meeting 22.06.2016

Manav Podar become Managing Director from 01.04.2017 to 31.03.2019 subject to approval in AGM

http://www.moneycontrol.com/stocks/reports/mayur-uniquoter-outcomeboard-meeting-3806981.html

Outcome of Board Meeting 22.06.2016

Manav Podar become Managing Director from 01.04.2017 to 31.03.2019 subject to approval in AGM

http://www.moneycontrol.com/stocks/reports/mayur-uniquoter-outcomeboard-meeting-3806981.html

I am particularly concerned about the increasing receivables and increasing inventories. Since the last 5 years there has been a steady but sustained increase from 16 days to 39 days in inventory and from 39 days to 51 days in receivables.

In March 2016 too, receivables have shot up to 72 days and inventories have increased too to 42 days despite flat sales growth.

Typical payment terms of auto companies should not exceed 30-45 days. Why this excessive receivables?

Normal receivable terms of most of the auto companies are 60 days and they hardly pay on time (from self experience!). So I would not be worried about 72 days days of receivables. Also as % of export goes up, it will tend to stretch receivables/inventory (depending on inter company transfer shown as sales or not) as many auto giants like GM, Ford etc expect the overseas suppliers to deliver JIT from local warehouse.

You must also remember that export auto business contributes less than 30% of the total business. 72 days receivables is for 100% of the outstandings.

In 5 years receivables have basically gone up 3.5 times whereas turnover has only gone up 2 times. At some point this must stabilise otherwise it is a bad sign.

Receivables increased in their wholly owned subsidiary by Rs.30 crs which was Nil last year. ARFy2016 pg no: 86. related party transaction segment.

Prashant

What was capacity utilization in FY2016 ? how many meters of synthetic leather company sold last year?

Prashant

anyone attended the AGM?? An update from the meet would be most appreciated. thank you.

Mayur to consider buyback

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=6b081648-1dab-4de0-a788-fc5a4dd4885c

Results out.

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/3C08C91B_1CD2_45DF_AAD2_D8F848E66948_150130.pdf

Decent results from Mayur. No buyback announced, which is a good decision according to me as the market is not right for buybacks.

Buyback announced–A proposal to Buy-back up to 5,00,000 fully paid up Equity Shares (Five Lacs) of the Company for an aggregate amount not exceeding Rs. 25,00,00,000/- (Rupees Twenty Five Crores onlybeing 1.08% of the total paid up equity share capital, at Rs. 500 (Rupees Five Hundred only) per Equity Share (hereinafter “Buyback Price”).

Right. Buyback announced. Maximum price 500 for buyback. Promoters intend to participate in buyback. I don’t understand the need for dividend in such a case.

Also news of resignation of Independent Director and Internal auditors.

Any source from where you got know that Promoters intend to participate in the buyback?

Internal Auditor change might be due to the rotation policy (will have to confirm).

I am not able to understand that why do promoters want to participate in the buyback? Somewhere this story is falling out.

Discl Invested

refer BSE website

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=de4c1a94-6ce8-4a95-b666-39b59ae26ce3

Buyback is just another way of giving back cash to shareholders. The buyback is for about 1% of the shares. This is similar to a 1% dividend. The advantage over dividends is that the company avoids the dividend distribution tax and promoters will avoid the surcharge as they receive large dividends. Hence participation of promoters is not really an issue.

Hi,

Does Anyone have annual report of Mayur for Year 2009, 2008, 2007, 2006 and so on .

If yes , Request you to send the report to my mail id : balajispice@gmail.com

Thanks

Anybody has any information or interactions with management about PU Leather plant of Mayur?

What is management focus on it?

If anybody has attended AGM of Mayur, please post your observations for the benefit of other value pickrs.

Q2 Result is not impressive. Revenues on decline and marginal rise in PAT.

Is Mayur loosing steam due to non-clear growth plan and family issue in company governance?

Some observations from annual report 2015-16 and comparison with annual report 2014-15

On setting up the new plant

AR2014-15

Company is talking about setting up PU plant and 50% increase in capacity.

AR2015-16

Same PU plant and same excuse for not setting up the plant after a year. Looks like company is not serious about this investment.

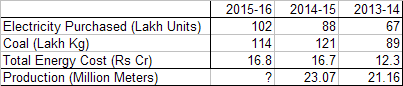

On volume of production

AR2014-15

Mayur is one of the largest manufacturers of synthetic leather in India having an installed capacity of 3.05 million linear meters per month. The production during the Financial Year 2014-15 is 23.07 million linear meters as against 21.16 million linear meters in Financial Year 2013-14.

AR2015-16

No mention of volume of production anywhere in the AR. Atleast I didn’t find it. If anyone has, please post. AR2015-16 PDF is not searchable as well. I am guessing production is down so they did not mention it.

Guessing from energy consumption numbers, volumes could be flat to down.

Their existing capacity is utilized about 64% (3.05 m meters per month vs annual production of 23 m meters) This could be the reason why they are not so keen on setting up new PU plant.

Given the stock valuation, a flat to declining production is not expected.