I’ll give a shot.[quote=“Surender, post:41, topic:8233”]

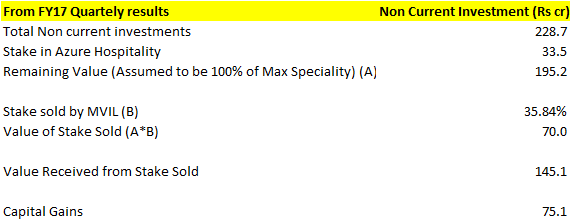

How the Net Capital Gain is 75 Cr?

[/quote]

Basically it’s Asset - Liabilities, wherein some assets are taken at market value/fair value and rest are taken at book value.

It remains to be seen which liabilities that were deducted from asset of MFSL to arrive at valuations of 196.45 crs. And also, whether market value of land bank(if any) was taken into consideration while arriving at valuation of 196.45.

Assets (Issue: Market price of land taken?)…554 crs

(-) Liabilties (Issue: only 82.84 crs clear liability visible)…357.55 crs

= Net Assets of MFSL …196 crs

(-) Valuations at which shares were sold… 405 crs

Premium at which shares were sold…209 crs

Shares sold to Toppan = 35.84%

Gain Realised = 35.84% of 209 Crs = 75 Crores

It is to be noted that no gains would have arise due to issue of fresh shares at a premium. So whole of gains should be from stake sale of 35.84 %.

I think it may not be possible to figure out exact calculation as it will mean estimating fair value of MSF which as @UtkarshP is suggesting is based on assets and liabilities of the company and stipulated regulations for calculating capital gains. However, it looks not so relevant to me, as it is more of accounting number. More important to me is the total enterprise value that Topan has paid for. That indicates, the value of MSF, representing IV of the subsidiary.

I am happy to see significant development on Rear estate front. I think in couple of years, we can see some numbers from this business - and some exits from Max I which again will (hopefully) accrue lot of gains to MVIL.

Does anyone have the link to latest interview of Sahil Vachani with Et now??

It was a special show , don’t remember d name n it was to be broadcasted on aug 20.

Based on my experience with past India Inc 2.0 interviews on ET Now, You tube video gets posted 2-3 weeks after interview gets aired. Similar thing happened after interview with Tara Singh Vachani on same show

On consolidated PBT level quarterly results looks quite impressive. PBT has gone up from 14 Lacs to 2.24Cr (YoY) and from loss of 32 Lacs to profit of 2.24 (w.r.t. last quarter)

Optically results looks bad due to big differed tax provision in this quarter turning PAT in loss on consolidated level. But I think bigger issue is sales degrowth of 5% in the quarter w.r.t. to last year and 2% w.r.t. last quarter. So need to watch for next quarter to understand the underlying issues of sales degrowth.

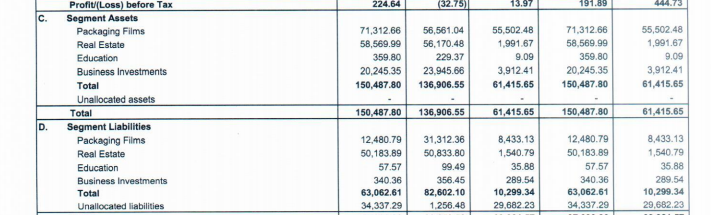

Hi Kitam, I got this number from the Q2 financials of the company. The total segment assets are given as below:

Packaging: 713cr

Real estate: 585cr

Education: 3.6cr

Business Investments: 202cr

You might be correct that their investments in Azure and Nykaa are 88cr. I think they have also included their current investments in mutual funds etc (INR 112cr) as well in business investments. This can be cross checked from their balance sheet as well which shows current investments of INR 120cr.

A update from max venture wherein max venture Wholly owned subisdary Wise had agreed to refund of 245 Cr to Piveta a private company owned by Analjit singh & family for cancellation of contract which have been signed effectively between wise and piveta that piveta will purchase .6m sqft area. Some advance seems to have been received by Wise vide this agreement which was not disclosed in this update.

Anyone have any idea whether this deal is good for shareholder of max venture or a typical case of related part transaction wherein private entity of promoters are winner in this deal?

As far as i understand from the postal ballot, MVIL’s subsidiary Max Estates is purchasing the land and development rights for construction of Max Towers from a promoter group entity Piveta for INR 245 cr. There is no way for us to figure out if this is a reasonable price. Although, the valuation has been done by KPMG and CBRE.

But still it leaves a lot of discretion with the promoters and we will have to trust that management is doing the right thing for the shareholders.

I think as per the above announcement sublease of the land was already with wise and 90 crore invested by max estate as per the announcement will be used for development of commerical area. Then for what this 245 cr will be given to piveta and in addition to it whatever advance wise had received from piveta also need to be returned to piveta. There are lot of question here even though managment tried to explain things in todays update/postal ballot.

By purchasing the stake in Wise, Max Estates has stepped in to the shoes of the builder. Piveta had an agreement with Wise to purchase some 519,000 sq ft of built up space, which it wants to cancel through this resolution. Out of this it already sold some spacce to Max Financials for 140 cr and Piveta has an obligation to deliver thesame, this obligation too is sought to be transferred to the builder, i.e. Wise. Piveta must have spent a certain amount on the project which is sought to be recovered from the valuation. The payment to be made by Max Estates is Rs 245 crs and Piveta has already received Rs 140 crs from Max Financials, i.e. total Rs 385 crs. It needs to be understood if Piveta has made any profits on this transaction. One would trust that the valuation would have taken into account current market prices, amount spent by Piveta and amount further required to be spent by Wise in arriving at the number of Rs 245 crs.

Is debt missing from this equation?

If yes, it becomes fairly valued as soon as debt of ~ 330 Cr. is considered.

A note from ICRA gives some details regarding the same “The project is envisaged at a cost of Rs. 840.0 crore. As of the end of August 2017, PEPL has spent Rs. 683.0 crore. The same has been funded through Rs. 419 crore of debt, customer advances of Rs. 140 crore against sale value of Rs. 140 crore from group companies and balance through promoter contribution.”: https://www.icraresearch.in/Credit_Perspective/DownloadRationalFile?RationalId=62918

If above note from ICRA is taken on face value, PEPL has spent 683 crore but sold it to WISE(i.e MAXVIL) at 385 Cr( 245-Cash to be paid+140-Liability)…I am sure that above thinking might be wrong as it’s Too Good to be true?