I realize 4500 can be misinterpreted for max stake. Thanks for pointing . Let me correct it

1 Like

My notes from Q3 FY 18 concall -

Management commentary

Lackluster QTR - Lukewarm - This is one of results and confident will not recur. Reasons

- Regulatory interventions

- Adverse conditions (pitampura closure, shalimar bagh license suspension for 12 days and rub off effect - main reason for depressed revenues)

- Suspension of cashless insurance by PSU insurance

- Regulatory Price control (stents and knee implants)

Growth - 9% in revenue

- 25% Oncology - leading

- Liver Transplant showing good traction - 200 surgeries

- Preferred channels outpace overall growth

- 15% Walk-in

- 22% International - expansion of upcountry channels (plan to accelerate G here); 4% is International here

EBITA decline of 7% on account of above reasons - Actually, 37% Growth in EBITA on adjusted basis for 9M discounting the above effects

Cost savings: 56 CR already realized (45% in personal, 30% Material, 25% indirect)

New bets (Total 3) - Done fairly well

- 2.7x increase in monthly revenue run rate of pathology (Current 1.2cr a month)

- Max at home - 2.9x increase in revenue (7 to 19cr)

- 11 product lines have been launched in last 16 months - integrated in digital platforms

- Oncology Day care center doing well - revenues grown 3x. Second day care in Gugaon going on. Initiated a search for 3rd one in Noida

Max Bupa

Business conitnues its growth

- 26% growth in GWC (now 505 cr)

- New sales on bancassurance has grown 100%!!

- 30% increase in renewal price

- Net Loss of 10 cr, near the break even at EBITA level

- Innovations

- Health Kiosks - placed at hospitals

- Gone digital - “Go active” concepts

Antara

Dehradun is a greenfield project (109 units sold). Strategy changed going forward

- Growth will be moderate

- Only asset light models - No Green Field projects

Working on opportunity where capital outlay for 2-3 yrs will be ~39cr for a project of ~700cr (Land and building by developer - SW will be provided by Max (expertise and model around senior living)

Brief Highlights for Q3’18

- Hospitals

- MSC gross revenues - 10% to 703 cr

- EBITA at 56cr declined about 11% YOY in this QTR

- Max Bupa

- GWP grown 27% to 128 cr

- 27% growth in renewal

- 23% growth in new sales

- Net loss has been contained at 5 cr compared to 9 cr the prev Year QTR

- Antara

- 109 units sold in Dehradun (50 residents moved into community)

Summary

- Max healthcare charting a profitable growth path

- Flat growth for next 12 months - due to reg headwinds

- Plan to Increase bed capacity - 5500 beds

- Max Bupa - Growth acceleration From 25% - strategy is robust

- Antara - pursuing and explore the growth oppurtunity in asset lite model

Q&A

Q: Recent revision of Stent prices (~5%). whats the impact in revenue and EBITA margins

A: Revenue will come down by 80L to 1Cr - Monthly run rate. There will be no impact in EBITA/margins

Q: Bupa - Sharp jump in claims ratio, why?

A: Due to compensatory factors - low Sales growth, Airborne and new kind of diseases. Claim rations forecast to be same

Q: Antara: whats the capital exposure planned?

A: Operator model - Asset lite model. Will limit to 39Cr (50% upfront to kick start). Risk is major on developer

Q: Whats the timeline for profitability?

A: 20-25% IRR project. Differentiator is low price premium and best model from Max serices.

3 years to deliver the project - FY2021

Enough Risk mitigation built in - much smoother and no capital spills

-Total 500 units - 3 phases of 170 units each.

-Fully REDA compliant

Q: Modicare benefit and leverages possible?

A: Too early - details are unclear. need to do detailed work over 1 to 1.5 months to come out with more info. excited about it. Will look at the entire model based on the pricing they opt for. This is state level structured

Q: 10-11% EBITA model is not a good one for medium to long term

A: Going thru difficult phase. Regulatory uncertainty causing this

Med to long term will improve 100-115 bps on margins expansion. On long term will get back to 15% margins

Q: Update on stay order for shalimar bag?

A: Stay order till April 12. will take a while to get over

Hospital is back to operational and at 80% occupancy

Q: Suspension of cashless insurance from public sector?

A: GIPA body going thru tough negotiations - more a stance based on max desire

Temp suspension and back on volume at much better rates. Back in business

Q: Comparable EBITA adjusting for one off. how much this amount to?

A: YOY grown EBITA by 37% after factoring in the impact of regulatory (YOU headline shows 9% degrowth)

Q: Did you increase the procedure price for compensating on cpa on stent prices

A: Did a partial increase. because Govt. is looking at this carefully so not totally recouped by increasing the procedure costs.

Q: Whats the timeline to increase the pricing?

A: This is reset, so not possible to recoup the entire loss. only some can be done and other is a re-set

Q: Has there been pressure on the stunt supplier? are you getting a better cost on different or substitution?

A: Govt is controlling trade margins as well. Also patient care is more imp and cannot optimize. we are looking at other process refinement and cost reduction actions to protect the EBITA margins rather than playing around with the price because that will defeat the objectives of Govt.

Q: Who will be major supplier for stents?

A: variety. Abet, medtronic etc. pricing is similar

Q: Normalized margin fir max health care. mid to high teen possible? is the long term been pushed back by how far to achieve this?

A: Long term been pushed off by couple of years. perf to be in similar ball part for next 1-2 years.

Overall cost to industry is 24 months (12 months passed, another 12 months need to wait out to come back to earlier growth levels)

Confident of delivering 100 to 150 bps margin

Q: 13.5% margin is possible by FY19?

A: We actually plan to use FY19 as reset and prepare for once and all - do not want to fall back to same position as current by course correct proactively

Do measures like: Plugin revenue leakages due to patient outflow, fix the leakages in trade margins around devices etc next 12 months and go from there

Q: You still managed to grow at 8-9% even with this headwinds. Will the underlying growth be strong?

A: yes, after a year of reset we can manage

Q: What are the cash level at holding company

A: 150 cr+225 from warrant = 375 cr cash available

(3.75% acquisition replenished the cash by giving warrants to the sponsor). we have enough liquidity available to take care of future needs

Q: Whats the net debt at max health care level

A: 1200 crs

Q: Strategically looking ahead - How do you plan to unlock value

A: Currently 2 schools of thought around this

- Current structure is not conducive for proper value reflection

- We look at everyone in the world - payers are becoming provides and vice versa. we plan to disrupt it. we have Payers and providers under same house. we will discover appropriate value here

Q: Ruboff impact of Shalimarbag lic suspension. what is the timeline to normalize?

A: Will take a few months. as of now, Delhi experiencing viral outbreak lot, due to this mix has changed so the revenue growth should be back on track

Q: why do we see a Divergence in new and old hospitals margins?

A: Growth is coming from relatively stable margin hospitals (Saket, Shalimarbag) - this is where the lever is

Q: Micro perspective: how do you deal with disconnect between Govt. and people perspective of super normal profit of hospitals but the reality is 12 to 13% margin.

A: This is actually media view. we are trying to put 2 points

- Generally they are not looking at holistic picture - they are seeing fragmented view.

- Cost of delivery in Govt is actually far more - they have the benefit the land and other infra which is provided by govt

Q: Antara: Is the scale up planned after the first asset lite model?

A: yes, we are moving in pilot model. nothing much planned beyond it.

If this succeeds, then we plan to do one project a year. as the projects increase the capital intake will not be high as this is asset light model and eventually come to break even and will see profits forward.

Q: Maintenance CAPEX 2.5 to 3% of top line… is it completely capitalized?

A: yes, completely capitalized

Q: How will the CPAEX number change in future… currently Max number is very low (50% of segment)

A: This will depend totally on the kind of care - secondary/tertiary etc… so we need to compare with right clinical specialty. we are currently quite robust in spending

Q: Is growth planned outside of NCR, may be based on licensing?

A: Yes, we are discussing in other cities. owner model, OPD model etc…

Q: Delhi act. how will it be impact?

A: Its been a mixed bag. in WB it was stringent. Karnataka was quite alright. will impact drug consumables margins, unlikely it will cap procedure margins.

Q: Adverse claim ration due to what?

A: we have a business plan being worked out. so we will know the stability plan.

Claim ratio in 50’s is a fantastic number.

we do not blame the B2B space. we plan the B2C space - we plan to manage this

Q: we are actually not competing with other areas (standalone) where as other companies are having mix of models but showing good claim rations. so why our ratio is not great?

A: At current rate - Break even happening in FY2019. its a Growth vs break even trade off. we are growing at 25% where as some guys growing at 40% - so we have a staregic plan being worked out to accelerate the current growth - we will provide a clear picture on this next QTR

Q: From long term perspective will you look at the trust type real estate model? instead of the current rental models.

A: Not at a stage where the business is matured to take on asset heavy models. over the medium to long term we will think about real estate trust type opportunity.

Since your value is driven by EBITA, we cannot sacrifice here and not in that stage

Q: flat growth for next 15 months due to pre-emptive measures. do you say that without the headwinds we should have good growth?

A: Voluntary re-calib. Across industry also we are seeing others doing the same.

11 Likes

Thanks for the notes, Sudheer.

This qtr was expected to be poor due to 12 day closure. Also, a lot of business headwinds all happening at the same time is resulting in poor operational performance. Despite that, revenue growth in healthcare segment is remarkable.

Max Bupa is doing well on GWP front; mgmt reiterated their commitment to attain break-even by 2019E, which is good. I believe one can see a hockey-stick sort of growth in this vertical in next 3 years. Of course they have to manage their claims ratio properly. They said it is a trade-off between growth and profitability at the moment. They have muted (25% growth), and are focusing more on attaining break-even.

Antara, well nothing to say as of now. They even don’t add a single slide in their presentation for this vertical. As many boarders pointed out above, this is poor capital allocation.

At current market cap of 2700 cr, Max India looks pretty decently valued assuming recent takeover talks for MHC. Management clearly said next year is going to be muted, and thus the stock is correcting. Who wants to block their capital for 1-2 yr in bull market! But for anyone with patience, this is a strong business with very good capabilities. Once recent regulatory hurdles settle off, we will see better numbers on MHC front.

any idea how you would value the Max Bupa and the hospital business? there were also talks of a deal in Max Bupa?

Please go through the whole thread. Valuation has been discussed couple of times already.

1 Like

@Mridul @rupeshtatiya @hitesh2710 @desaidhwanil Any take on promoter pledged shares ?

http://www.moneycontrol.com/news/business/markets/top-20-stocks-that-saw-increase-in-promoters-pledged-holdings-in-q3fy18-2511817.html

Disc : 2.5% allocation done in last 1 month

News update:

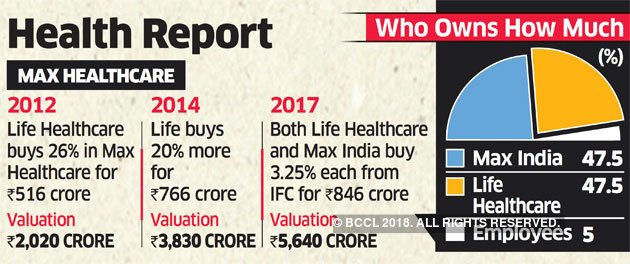

Max India looking to buy out its equal JV partner’s (Life Hrealthcare, SA) stake in Max Healthcare Institute.

1 Like

These are usual pledges “security for loan”. As share price has tumbled almost 50%, additional pledges are supposed to be made to secure the same loan amount.

1 Like

Went through Q3 FY18 concall. Got a felling that these guys are shifting the goal posts of all three verticals every qtr. MHC is in mess due to regulatory headwinds, which are expected to continue. For Bupa, when asked about guided break-even in 2019, they changed their stance that if the claims ratio does not go down, break-even might not happen in 2019. Antara, they are not even disclosing numbers and have now shifted this to an asset light strategy where returns will be after 2021.

They have said that maintenance cost for MHC per year is 2-3% of revenue. So is this business ever going to make any real money (cash) in long run? I doubt. I understand this is a capital intensive sector but the “assumed” pricing power isn’t just there. One discussion in concall exactly hovered around this point that people think hospitals are making abnormal profits, while if you look at the numbers, they are hardly sustaining or generating cash.

REITs were discussed but management said they don’t want to lower their EBITDA further by bringing rental expenditure (opex).

On Bupa, they have always said that there is a trade-off between growth and profitability. In order to attain more growth, one has to take a hit on profitability.

Overall, there is nothing happening here in next 12-18 months. There will be more pricing pressures, more regulations coming in, debt cost rising, debt piling up to 1200 cr now. I have been optimistic about this in long run, but just reviewing my stance on this one as despite having good capabilities, this business will remain capital intensive and seldom is a chance they will generate free cash.

I am optimistic about Bupa, but constant shifting of goal posts does not help.

Disclaimer: Invested. No transaction in last 3 months.

3 Likes

Valuation-

Fortis -

![]()

Had missed this 3 months old article

https://economictimes.indiatimes.com/industry/healthcare/biotech/healthcare/radiant-looks-to-buy-max-healthcare-stake/articleshow/62423073.cms

Disc : Invested and accumulating

Found one positive article on max bhupa

Blockquo Asked about the competition they might encounter in Gurgaon, a spokesperson for the company said there was a “huge gap in the number of patients and the number of beds required”, in the city and there would be “no competition” as it expected continued flow of patients.

There is lot of transactions going on in healthcare companies. Although I initially bought Max India only for Health Insurance, I am not able to understand is Healthcare a good long term investment from India perspective? With companies struggling to make profit, investing in best doctors, research and equipment will add to the woes, perception issue is another thing.

One thing I am not able to understand is why some big PE firms are on the buyer side. Apart from current low valuation, what other good they see in healthcare companies as long term investments that we are unable to see?

As per Vijay Kedia " The worst time for a sector is best time for an investor" or as per another saying “Buy at the time of maximum pessimism”

Healthcare penetration is very low in India and growing population, urbanization, changing lifestyle, increasing air/water pollution etc all points out to long runway for healthcare sector in India. Big PE firms want to use this temporary (may last for another year or two) pessimism to get entry at a good price and exit when optimism returns to this sector. That’s how all great investors make money.

But market can test your patience and this sector can provide lackluster performance for much longer period than anticipated. So investing in such contra themes is for the bravehearts!

1 Like

Completely agree…just for sake of understanding contrarian and sector down…how do we compare current down sectors say Healthcare, Telecom and Pharma…I feel pharma has structural issues and lot of ambiguity as who will be winner…telecom and Healthcare seem somewhat similar…demand is intact but business model needs reinvention…big question…will new business model ROE and cash generation good enough for long term investors…PE investors apart…my confidence came from Mr Burman and Munjal showing interest in Fortis and Analjit Singh willing to buy remaining stake of Max from South African firms…

The issues for each of the sectors mentioned by you are different. For healthcare sector, it is more about regulations and govt interventions. For Telecom, it is about competition as well investments required for technology upgradations. In case of Pharma, it can be split into two types of companies - Domestic focused have issues similar to healthcare sector whereas for exporters, it is more about quality ( USFDA inspections) as well as pricing power erosion (mainly in US). Trade wars add bit of confusion on top of it for pharma exporters.

Hence for each of the respective sectors to come back to its “prime” will be different. It looks like Pharma have started turning around after few years, but may take few more years to return to glory. Telecom sector will gain its importance when pricing power returns post consolidation. I guess pessimism may continue in healthcare for at least another year due to elections. But it may offer the highest reward in the 3-5 years perspective if entered at right time in right stock.

2 Likes

In cities, healthcare penetration is better than USA. Doctor population ratio in Delhi and Mumbai is higher than USA.

Waiting for a cataract surgery or hip replacement surgery under NHS in UK is 6 mths to 2 years. In India, you can get it next day.

In US, it takes a month to get specialist appointment. In Indian cities, it takes 2 hours.

Healthcare penetration is very low in rural areas. And I don’t think that is an addressable mkt due to very low population density and very low incomes.

Also, the industry is very fragmented. There are thousands of standalone unlisted hospitals. Govt hospitals is another competition.

Pricing power is very poor. Also, very capital intensive industry.

4 Likes

Open offer hopes fuels Max India’s price rise. The reason for the sudden spurt in price was clear when it was announced that SEBI has rejected the promoters request for exemption from open offer following shareholding rejig in 2016/17. So will there be an open offer or will Max promoters appeal again ?