I was commenting on Max ventures in that sentence. But I am positive about all 3 demerged entities.

Disclosure - I hold positions on all 3 entities and continue to add more so my views could be biased.

I was commenting on Max ventures in that sentence. But I am positive about all 3 demerged entities.

Disclosure - I hold positions on all 3 entities and continue to add more so my views could be biased.

More investment from Promoters. I liked the fact that promoters are buying warrants almost at market price and not at a discount which is normally a practice. Speaks a lot about corporate governance standards of this group

Max Financial Services tanked yesterday on unconfirmed reports that HDFC Life might go ahead with its plans of IPO.

In this interview with ET Now, Tara Singh Vachani explains the concept of Antara - Senior Living - a venture under Max India.

As India’s income level goes up, those who can afford would be willing to pay for quality of life post retirement. Antara is bringing many western concepts like “life time leases” where the apartment is leased to the customer but customer can not “will” it away to its legal heirs after his/her death. But appreciation in the price of the apartment will be passed on to the legal heirs.

It can be a game changer for senior living in India if executed well and real joker in the pack for Max India shareholders.

Disclosure - invested prior to demerger and continues to add more

Max India results are out

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/8b67eaf0-816b-48f5-92e5-eb8b28024f76.pdf

Income up by 18%, Loss gone down by 50%. Health insurance business turned profitable for the quarter. Antara Senior Living continues to remain a drag but that should be as per plan.

I think it is moving in the right direction.

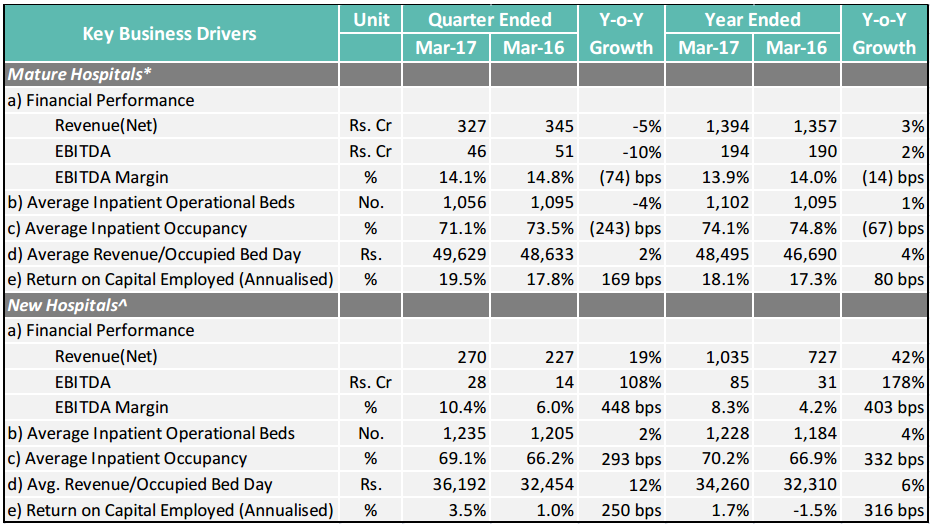

Above data indicates clear deceleration in trends at mature hospitals.

@Marathondreams indeed at the operating level health insurance has turned around. However the net loss of Rs. 12 crore for the quarter is higher than the Rs. 4 crore loss for the full year. I wonder what contributed to the bigger loss in 4Q. I also note that claim ratio has now risen to 59% in 4Q.

Overall I feel results are mixed at best. However the stock was already down 5% yesterday, so might not react too negatively today.

Disc. Invested and might look to add more over a period of time.

I agree with you that mature hospitals are showing “fatigue” but I am more interested in insurance and senior living businesses. If you look at investments and returns, you could clearly see that although investments in all 3 - hospitals, insurance and senior living, is almost the same, only hospitals are giving returns as of now. I expect senior living to show returns from 2018 and insurance from 2019 onwards. So this stock has long way to go but would need patience.

Max Life is part of Max Financial

Key highlights of the Q4FY17 concall:

Max Healthcare (hospital business)

Funding for Saket hospital’s stake purchase (of remaining 49%) has been tied up with IFC for a debenture of Rs.500 crore at 10.50% rate of interest. The NCD will have a tenure of 15 years with moratorium of 2 years and very low repayment for the next three years. Majority of the repayment will start from FY22 onwards.

Mature hospital’s revenue de-grew because of few major reasons and many of them were temporary in nature: Some of the orthopedic facility was shifted from mature hospitals to new hospitals which led to some of the beds being not available, Pitampura hospital stopped inpatient facility and converted to OPD and day care center, demonetisation continued to impact the business especially in the early part of the quarter, mild winters in Delhi also had an impact on the revenue and some impact was seen from cap on stent prices. Pitampura was converted to OPD and day care center as although the hospital was contributing to the topline growth, the profitability was pretty low there. The hospital is in a mall and was constructed by joining few shops and hence its inefficient. Furthermore, the Shalimar hospital is 10 - 15 mins away from Pitampura hospital and will cater to the patients of Pitampura hospital.

Profitability margins of the mature hospitals was also impacted because of regulatory impact like price cap on stents and rise in minimum wages by Delhi government. Some of these impact will be passed on to end customers. The yearly impact of these regulatory changes is expected to be around 45 crore which will be offset by Rs.60 crore cost saving the Max Healthcare is targeting during FY17 (Rs.50 - 60 crore cost cutting during FY16 as well). The profitability of the new hospitals continues to increase.

Max Saket, the flagship hospital, has received Joint Commission International (JCI) accreditation which is expected to increase the international business going forward. International business is currently contributing 10% to the overall revenue while institutional business is contributing 21%. Management plans to increase the international business to 14 - 15% of the total revenue while cutting the institutional business to around 14 - 15% of the total revenue. The company has also set up 5 offices in Kenya (Nairobi), Nigeria, Bangladesh, Myanmar and Iraq. Two of these offices have been opened directly while three are through intermediaries. Liver transplant has big demand in these countries.

Updates on new initiatives - Liver transplant surgeries started from February, 2017 and the hospital has already done 35 surgeries till date. On the diagnostic front, 320 B2B ties ups while B2C was launched in Q4. Business of Rs.75 lakh per month being contributed from it currently. Oncology day care has turned PBILDT positive from Q3 of this year. Robotic surgery have also started at our Saket hospital which is mostly used in oncology, urology, gynaecology and one more segment.

Capex plans: Rs.1.10 crore cost for setting up new bed (most probably referred to brown field expansion) while 3% of the revenue is the maintenance capex. FY18 capex is expected to Rs.800 crore including purchasing of remaining stake in Saket hospital (Rs.470 crore), setting up of new beds and maintenance capex. FY19 capex is projected at Rs.350 crore.

High debt and leverage: The debt is high on account of purchase of two new hospital in a short span of six months last year. However, the debt is structured in such a manner that there are very low repayments over the next two years (Rs.25 crore) while majority of the repayment are expected to be due after FY22 when the company is expected to generate healthy cash flows. The management has a check on the leverage. Targeting Debt/EBITDA of 2.5 - 3 times by FY21 - FY22. Even at our parent level (Max India) we are keeping some free cash for funding our capex requirements in the near to medium term.

Other developments: On Life Healthcare rejig at top management - The management continues to report to their old counterparts and there are no changes in that structure. On purchase of stake of IFC and issuance of warrants to promoters - Purchase of IFC stake was not factored in our cash flows and hence going for raising of funds. Promoters see good growth in the business and hence increasing stake. Some of the fund raising will also be used for funding plans of Max Bupa and Antara.

Max Bupa

Antara

(Disclosure: Invested)

Thanks @ankitgupta for the highlights. Did they speak anything about the pathology business that they mentioned in the Q3 concall and were supposed to start this quarter?

Q3 Concall excerpt:

“As an update on our new growth bets, these are progressing well too. Our pathology B2B

business launched in May 2016 has already done over 250 plus tie ups. The B2C

pathology business is also expected to be launched in Q4FY17, and we intend to

scale up this business quite fast.”

As mentioned in the summary, on the pathology front, the management mentioned that they have 320 tie ups on B2B side (increased from 250 plus during Q3 concall) while the B2C business was launched in Q4 as indicated in earlier concalls. Currently, they are doing revenue of around Rs.75 lakh per month and PBILDT margins from these business are higher compared to the existing hospital business.

Max Financial Services (MFS), Max India and Max Life today confirmed that the proposed merger with HDFC Life has been called off. The exclusivity agreement with HDFC Life, valid till 31st July 2017, will not be renewed.

More details at http://www.bseindia.com/xml-data/corpfiling/AttachLive/9a44644d-41b5-48d7-8b0f-da0f9b9a4de7.pdf

Max India - Key Highlights - Q1FY18

1. Max Healthcare :

Revenue growth 10% to Rs. 702 Cr

EBITDA growth 8% to Rs. 64 Cr

EBITDA margin 9.6% vs 9.7% YoY

Cash profit growth of 30% 32 Cr vs 25 Cr YoY

PAT loss at 3 Cr vs 5 Cr YoY

Impact due to stent pricing, closure of Inpatient facility in Pitampura & dis-empanelment from few ESI & PSU accounts

2. Max Bupa:

Gross premium growth 30% to Rs. 159 Cr - 31% growth in renewals and 28% growth in new sales

Net profit 0.2 Cr vs. net loss of Rs. 5.6 Cr YoY

3. Antara:

Commences operations in April’17.

102 units sold, 35 residents moved in

Investor presentation: http://www.bseindia.com/xml-data/corpfiling/AttachLive/eae6399f-92b9-455d-bdeb-fb40ccf6bbc4.pdf

Disc: Invested

Max India Q1FY18 Conference Call Highlights (My notes - might contain errors/mistakes)

1. Max HealthCare

Financials and management commentory:

• Revenue growth 10% at 702 Cr

• EBITDA growth 8% at 64 Cr

• Impact due to Stent pricing control, closure of Inpatient facility in Pitampura, dis-empanelment from few ESI & PSU accounts

• Expect strong revenue growth from up-country market and international channels

• Plan to convert Pitampura into Day care model same as Panchsheel

• Patient experience metric increases to 74% from 63%

• Two landmark acquisitions in 2015

• Plan to double the bed capacity – 5000 beds

• As hospitals move from unmature to mature state, we are outbeating on profit expansion as compared to other hospital chains.

Details:

• Average revenue per occupied bed increases 7% at Rs. 44,940. Price increase 3% rest across specialities

• Doctor model – part of cost savings, Minimum guarantee – most of the doctors, 15% doctors may not have guarantee. 2800+ doctors with 65% on rolls

• EBITDA per bed – our focus not on percentage but absolute number

• Speciality mix will be shared later in future Investor presentation

• No one has land capacity in Delhi, there have been few additions in Noida and Gurgaon. 500 beds by Jaypee hospital can go up to 1200 beds. Enough demand to absorb supply, did a Demand Analysis during Saket hospital exercise

• Measure capacity utilization by Night occupancy at 12am. Sunday – occupancy usually drop

• Capacity utilization can go up to 80-82% - comfortable and right thing to do, expect 7-8% increase from current levels

• Moved away from reporting breakup of unmature and mature hospitals. This reporting was misleading to some extent

• East Delhi complex and Saket – 70% of business. Expect to have most aggressive growth from these locations with future bed increase coming up in these locations.

Cost savings program:

• Program launched to achieve 70 Cr cost savings in this year

• Achieved cost savings of 100 Cr in FY16-17, this year target is 70 Cr, planning further 50 Cr

• Total 50-55 Cr may reflect in P&L, others achieved on account of not approving increase in budget requests from different units

• Half impact due to personnel cost, rest material

• Trying to optimize material usage – each surgery

• Achieve better negotiated rates through effective sourcing negotiations

• Optimize Doc cost, bring down power cost, optimize travel/conveyance cost.

Regulatory price control impact:

• Total 68 Cr impact - Minimum wage hike 37% in Delhi, Stent pricing impact, Drug pricing and ESI limit increase/maternity requirements

• Knee caps – impact 3-5 Cr

• Don’t bill at MRP, currently using markup

• 22 items got affected, total 30-100 Cr impact (rough estimate)

• Tried to bundle the prices but regulation said Stent has to be priced separately

• Mitigation on bundling product and services – change the business model.

Revenue distribution:

• Up-country 20% TPA/Walk-in. 5 more offices Lucknow etc. Meerut, Ambala – OPD; Lucknow – no OPD. Should be able to bring to 25% level.

• International 10.5% - opened office in Kenya

• Digital Channel – very promising – lot of potential

• Current ratio Indirect:Direct 70:30; Future plan to convert other way round.

Pathology:

• B2B – May’16 – 400 tie-ups, B2C launched last quarter

• Revenue 2.5 times growth monthly, 1 Cr/month run-rate.

Debt:

• Net Debt 1100 Cr

• Stake purchase 49% in Saket – close of this year

• 22% Pushpanjali Crosslay – 2.5 years out.

Capex :

Over 4 years – 800 beds coming up with expected 1 Cr per bed cost, total Capex 800 Cr

• Largely debt driven

• Debt/EBITDA 2.5-3 times

• Over 4-5 years horizon, Cash flow from Operations should be able to fund 70% of Capex.

Future growth forecasts:

• Revenue growth 12-15%

• EBITDA growth 20-25%.

2. Max Bupa

Financials:

• Gross Written Premium increases 30% at 159 Cr – driven by 31% growth in renewals and 28% growth in new sales.

• Net profit of 0.2 Cr vs net loss of 5.6 Cr YoY

• B2C segment – premium 32% growth

• Conservation ratio at 82%

• Market share at 3.9%

• Opex ratio down from 60% to 50%

• Q4 is biggest quarter so we may see Red again. Breakeven expected in FY19.

• New initiatives – policy within 2 mins

• First point of care desk – Saket Hospital from 30 mins pre-authorization to 15 mins

• Corporate agency agreement signed with South Indian Bank – goes live in Aug’17. This will give access to 850+ branches. Tie up with Federal Bank is already there in that geography.

Details:

• Overall contribution from Bancassurance channels – gone up to 20% from 15% last year

• Online sales – 15-20% digital – included in Direct Sales. Price increase 15-40%, blended 20% increase.

• Some signs of break-even by FY19. Q2&3 to be similar, may again see Red in Q4.

• After FY19, it can be a hockey stick, profits to emerge, start becoming meaningful.

• Agents come down 35% ? Terminated in-active agents – regulatory requirement.

• Agents Commission costs – variable. Supervision and training cost – need to bring down.

• Insurance agents are exclusive, however they do distribute 2-3 products using family members

• Number of agents – channel mix – half agency, half third party. Cleanup of unproductive agents 15-20%.

• Other players in industry - Star health – adding branches and agents aggressively – might be on a sell-out journey.

• We believe in calibrated growth, having a Sustainable Profitable Growth.

• Experimenting with Variable agency model – may double the profitability of channels if it works.

• South Indian Bank channel can scale up in next 6 months. Launch expected in August.

• Want to do a meaningful distribution expansion – add more profitable channels.

• Advantage with PSU banks – don’t push for extra profits, content with what is required as per regulatory guidelines. Bank of Baroda – 35% network penetrated.

3. Antara

• 30 residents moved in. More than half units already sold.

• Capital investment 1250 Cr (200 Cr equity rest Bridge Finance)

Investor presentation: http://www.bseindia.com/xml-data/corpfiling/AttachHis/eae6399f-92b9-455d-bdeb-fb40ccf6bbc4.pdf

Disc: Invested

More pain for hospitals after stent pricing regulation -

The government has slashed the prices of knee implants by between 59% and 69% using a special provision in the drug pricing law that enables it to intervene in “extraordinary circumstances” in public interest. The move is expected to benefit over three crore arthritis patients in India needing knee replacement surgery.

How is this going to impact the hospitals? I think it would have a direct impact for first few qtrs though affordability would result in more operations. This might compensate for the lost revenue.

Official sources said hip implants and intraocular lenses are the next items likely to attract the attention of the regulatory scanner.

My notes from Q1 FY 18 concall -

Healthcare

Finalized a funding facility of about Rs.484 crore through a non-convertible debenture in Max Healthcare again from IFC to acquire the balance 49% stake in Saket City which will most likely happen in Q4 FY18

Our preferred channels have outpaced the overall growth and our walk-in revenues have grown by about 12%. The upcountry channel through which we are going direct to market, as in direct to where patients. are, has grown by about 45% and our international business (10.5% of revenue (70% indirect and 30% direct)) has grown by about 24%. Oncology leading the revenue growth by growing about 24%. Trying to reverse the direct indirect ratio in 3 years.

Cost to setup international offices ~ 1.5cr per annum. Break-even in 6 months usually. They ave setup 4-5 offices to increase the international pie. Upcountry setups costs anywhere between 20-50 lac depending upon OPD.

Regulatory headwinds, the impact of stent pricing, minimum wage revision impacted revenue and margins. cumulative impact of all the regulatory actions is about Rs.65 crore on the earnings. Because of which, our margin has remained more or less flat in the quarter.

Have been sort of taking lot of initiatives to overcome that regulatory impact and the biggest of them is the cost savings. So as we speak, we have identified about Rs.70 crore of cost saving for FY18, out of which we have realized about Rs.15 crore during this quarter. These savings have come out from all the cost lines, but half of this is from the personnel cost and then the other half is divided between material cost and the indirect cost. The technology led cost rationalization and mix improvement journey will continue for another 3-4 years as we achieve the desired level of margins.

Saket Complex posted strong revenue growth of 14% and EBITDA margin also improved by about 150 bps versus Q1 last year to about 12.7%.

Max Healthcare is now one of the select few entities which has a liver transplant program. performed 55 surgeries in q1.

2,800 plus doctors, out of which about 65% are on rolls and about 35% are visiting consultants

Manpower is the only cost which will always go up. So max is trying to work on this cost to ensure that the growth is actually 70% of what the revenue growth is. So today these costs have been growing in the same proportion as the revenue growth, which is not ideal condition, but they want to make sure that this curtails. So, in order to minimize the impact of min wage hike in Delhi by 37%, they are trying to find out what jobs can be automated, bumped and things like that.

Pathology revenue has already sort of given us a 2.5 times growth of its monthly run rate and is currently getting closer to about Rs.1 crore a month run rate. Intend to scale up this business quite fast.

Started a daycare center on the cancer centre site, which is doing very well and has already achieved EBITDA breakeven in 12 months of operation.

Hospitals should be compared on EBIDTA per bed. Narayan’s margins are higher but EBIDTA per bed is half that of Max. The mature hospitals, that number would be Rs.25 - Rs.26 lakhs/bed today. This 25 lakh number can go up by at least 10%-12% in the foreseeable future.

Converting Pitampura into a daycare clinic model, same like we have in Panchsheel.

Expect the growth trajectory to continue for many more years as they double bed capacity to about 5,000 beds (brownfield).

4-5 cr impact due to knee cap price regulation.

There are 22 other consumables being considered by regulatory authorities. Depending upon how they put cap on these items, there could be an impact ranging from 30-100 cr. Mgmt is looking to bundle the prices. With stent, there was a regulation that it needs to be billed separately. They do make money with drugs and consumables and do not make much money from services…but will now revamp business model to raise the price for services. On Stent pricing front, they will not be able to recover the full losses, but they are doing various things in order to minimize the impact. This might happen starting q4 this year. Hoping to reduce impact by 70% through package price increases.

Currently other than Max, nobody has a land bank to add any beds in Delhi…there could only be some addition in Noida and Gurgaon, though. Regarding demand for the additional beds, mgmt is confident that these additions would be absorbed. While putting up the plan for Saket, they did a thorough analysis.

There has been a good improvement in average length of stay, as well as ARPOB (by focusing on right specialty, through right channel mix…and 3% price increase)

The potential acquisition of 49% in Saket and 21% in Pushpanjali Crosslay are the two outstanding items. Pushpanjali Crosslay is 2.5 years out, but Saket City is something which we are going to do by close of this year

At the healthcare business level, we have a net debt of about Rs.1,100 crore as of June end

Capacity utilization right now is around 72%. Can go up to 80-82% at best depending on specialty.

Capex for next 2-3 years will be debt funded. They have got capacity to leverage in Balance Sheet. Moreover, they converted all loans to 15 year period with 2 year clear moratorium and 3 year of very small repayment. So, when they start repaying debt, debt to ebidta would be 2.5-3 times. Also, 20-25% topline growth will result in good accruals, which would help with debt repayment. Means, CFO would be able to fund this 70% of the capex over a horizon of 4 to 5 years.

Want to add roughly 900 plus beds by FY21 and it should take Rs.1 crore – Rs.1.1. crore kind of a number for the CAPEX.

Pathalogy

Looking for 350 odd cr turnover in next 3-4 years (in house requirement).

This business can be scaled quickly if need be.

Bupa

Max Bupa business continues its fast pace growth and has grown its gross written premium by about 30% to Rs.159 crore. The new sales of Banca channel has grown by 121% and digital by 38%. Have tie ups with BOB, Federal Bank, RBL, and now South Indian Bank. OPEX ratio has improved from 60% to 50%.

The business is marginally profitable, but Q4 is the biggest quarter, which is where we could see a little bit of red again; however, overall sort of guidance in terms of directionally business getting into a break-even in FY19 continues. Hockey stick from 2019/2020!

Lots of new initiative like 2 minute policy issual.

Claim repudiation also sort of coming down from 13% to 9% which also reflects on good underwriting practices

Conservation ratio this qtr was at 82% (includes price hike). Ideal - 90%, which will happen in future.

Price increase across product categories is about 15%-40%. So, on an average you can assume like a 20% price increase.

Overall contribution from banks have gone up to 20% from 15% last year.

Digital contribution to sales ~15-20%

Number of Bupa agents has come down by about 35% Q-on-Q. This is deliberate to reduce training and supervision costs on inactive agents.

BOB penetration at 35%. f this, Max is getting 50% of the overall sales. Star is the other partner with BOB, which is getting remaining 50%, though has fully penetrated.

Compassion on growth models of other standalone insurers - Star, Cigna and Religare vs Max - Star is on a sell out trajectory and is trying to maximize sales (even non profitable) by opening branches relentlessly. Star will have GMP of 3000 cr this year, but won’t be profitable yet. Religare and Cigna are also expanding capacity. Religare has been pushing B2B significantly and Cigna has tied up with Bank of Maharashtra and Andhra Bank. So therefore their growth largely is through distribution expansion lead growth, whereas Max always believe in a calibrated growth which is more profitable. On agency side, Max is trying out variable agency model. If this model clicks, it would double the profitability of agency channel. Max tries to launch a pilot at few location (say 20), try to make the model profitable, then go for expansion. When Max will get to double of where they are now, they will be making some healthy profits. So, to that extent, even at half of where Star Health is, Max will be making very healthy profits.

Antara

Capital invested in Antara is about Rs.250 crore. Part of it has gone up with bridge finance, but part of it is equity, so about Rs.200 crore equity and 50 cr is bridge finance.

Around 30 residents have already moved into the community and more than half of the units are already sold. Has now reworked its strategy to drive capital lite growth in the future. Will speak about this in next few qtrs.

This news update is on Max Financial Services. Seems that suitors are again eying this bride

Thanks @drgrudge for link to IRDAI that publishes monthly GWP.

Data for August →

https://www.irdai.gov.in/ADMINCMS/cms/frmGeneral_Layout.aspx?page=PageNo3254&flag=1

GWP →

Aug’17 → 54Cr vs. 45Cr

YTD → 267Cr vs. 211Cr

I have been reading up about Max India and following are some notes →

The company has three major businesses namely Max Healthcare (46% stake), Max Bupa Health Insurance (51% stake), Antara Senior Living (100% stake).

MAX HEALTHCARE (MHC)

This business was started in year 2000 and it is an equal JV partnership between Max India and Life Healthcare, South Africa.

Hospitals

The company currently operates 14 hospitals with 11 hospitals in NCR region and a hospital each in Mohali, Bhatinda & Dehradun. The Mohali & Bhatinda hospitals are under PPP arrangement with Punjab govt who has also provided 50 year lease for hospitals. 11 hospitals are NABH accredited and 1 hospital is JCI accredited. (Apollo has 17 NABH accredited hospitals and 8 JCI accredited hospitals).

Number of Beds

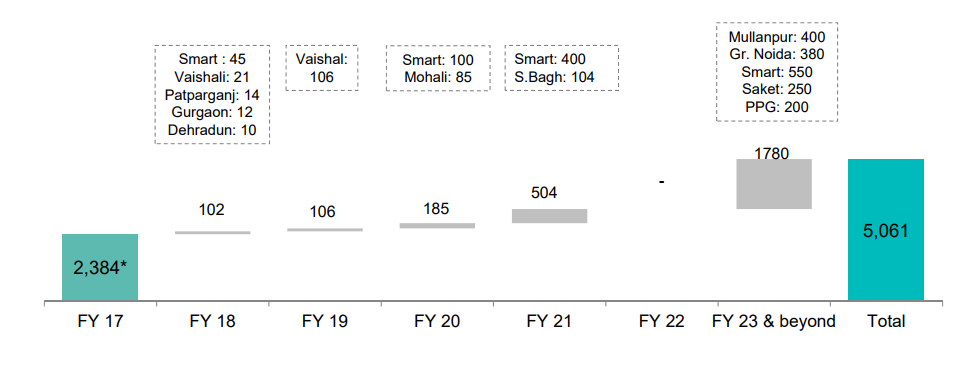

The company has 2330 operational beds (total beds at 2500) and It plans to add 900 beds over next 4 years and double the capacity to 5000 beds around FY23-24. The company expanded by acquiring 2 hospitals in NCR area in FY16. The details of acquisition are as follows →

The company has planned a capital outlay of 650Cr to acquire stake in Max Saket & Max Vaishali.

The bed addition plan is provided by the company in latest investor presentation →

The revenue and EBITDA figures for last 5 years are as follows →

Cost Savings

The company achieved total ~100Cr savings in FY16 & FY17 in MHC. The company plans to achieve 70Cr in cost savings in FY18 (18Cr achieved in Q1FY18). They claim to have visibility for this 70Cr and have set sights on next 50Cr.

Competitive Landscape

Following slide in investor presentation captures the competitive landscape →

The things worth noticing are the lowest ALOS (Average Length of Stay) & highest ARPOB (Average Revenue Per Operational Bed). The ARPOB is almost 50% more than Apollo. This is expected as Max is purely into Tertiary and Quaternary care whereas Apollo does primary, secondary & tertiary care. EBITDA per Operational Bed is at 20L.

New Businesses

The MHC has started following new businesses - Max@Home, Max Labs and Oncology Day Care.

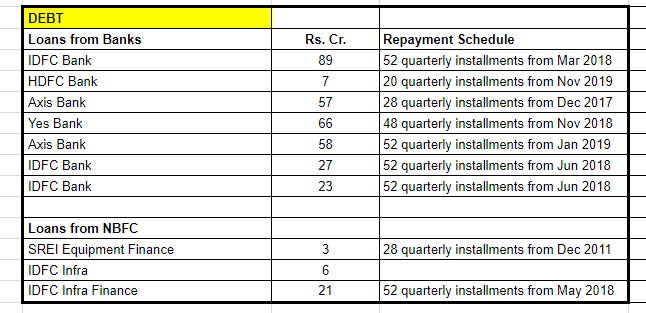

Debt

One of the things that senior VP members have pointed out is superior debt structure of Max India due to management skills. Most of the debt repayments start with a delay of 12+ months and very few managements can get these kind of deals.

Advantages

Risks

MAX BUPA

Max Bupa is a 51:49 JV between max India & Bupa Finance, UK. It is standalone health insurance (SAHI) company in India.

BUSINESS

The company has tie-up with 3600 hospitals across 350 cities. The company serves 20L total customers out of which 10L are urban customers. The health insurance industry has size of 25,000 Cr based on premium written and company AR claims it will grow to 50,000 Cr by 2020. There seems to strong tailwinds in the Health insurance industry with growth of 15% for many years.

Distribution

The company has four distribution channels - Agency (17,000 agents), Bancassurance, Direct Sales (130 tele-callers) and B2B.

Bancassurance

The company partnered with Bank of Baroda in FY17 which has 5400 branches & customer footprint of 6Cr customers. The company also has existing partnerships with Federal Bank, Standard Chartered, RBL Bank, Deutsche Bank, Muthoot Finance & Bajaj FInserv. The company has also partnered with South Indian Bank which gives access to 850 branches.

Industry Data

There are total 25+ general insurance companies and it is a very competitive sector.

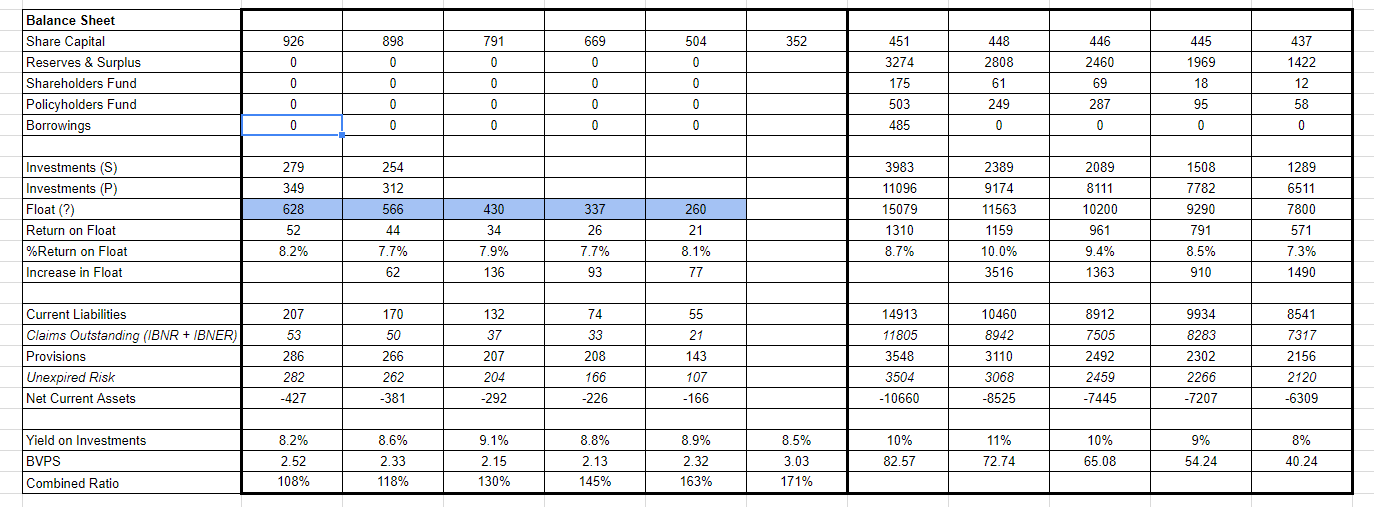

GDPI, Loss Ratio & Combined Ratio

Star Health is biggest player in terms of GDPI. Max is a small player in health insurance sector and should have ample space to grow. Loss ratio of Max India remains at very attractive 50-60%. If commission + operational expenses can be efficiently managed, there can be underwriting profit. HDFC Ergo has best combined ratio and Max has brought its combined ratio down from 130% to 108%.

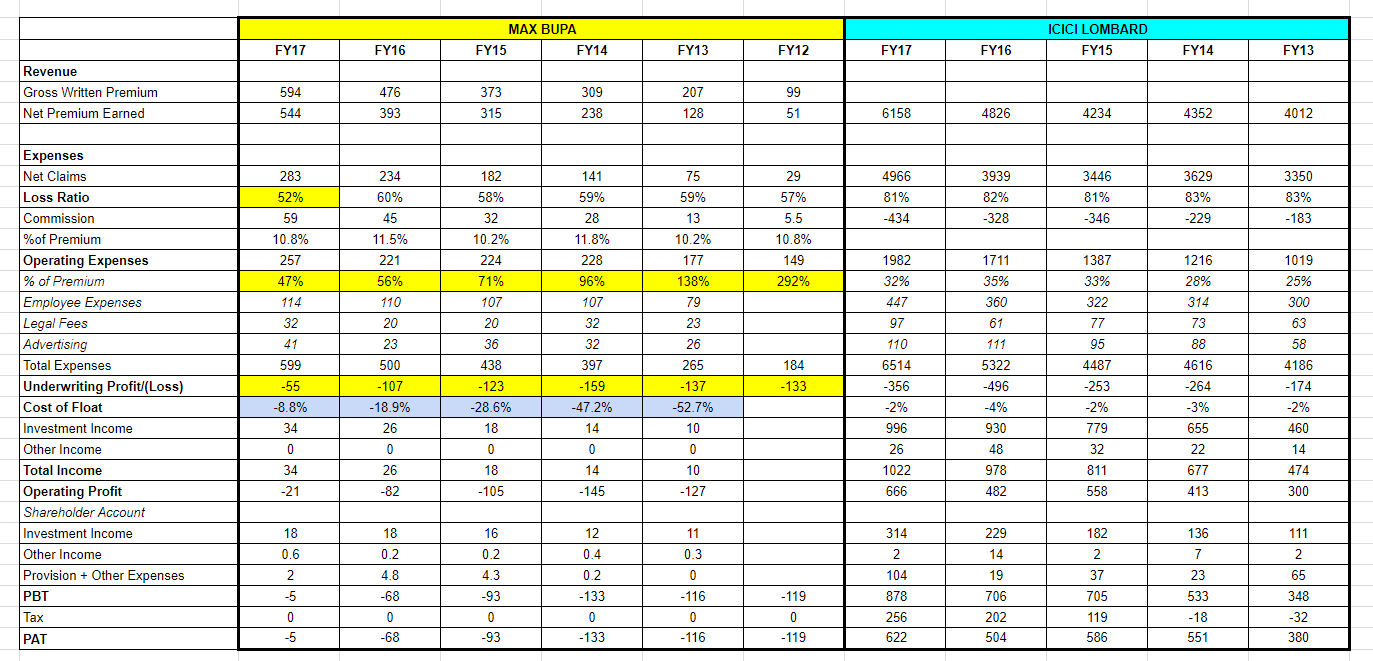

Finance Numbers

Since understanding insurance business is WIP, I will use Max Bupa & ICICI Lombard numbers as side by side. Please note that - ICICI Lombard is not strictly comparable to Max Bupa because it does insurance for Motor TP, Motor OD, Marine, Fire etc. as well.

P&L Account

Few Points

Balance Sheet

Few Points

Advantages

Risks

ANTARA SENIOR LIVING

I have nothing to add about this business other than I think that this is a capital mis-allocation. Senior living is a very good concept and as a millennial, I think I would be staying in one after 55-60. But that does not make it a good business or good investment.

VALUATION

This is the tricky part for this business. I would like to present two views - one short term (3-4 years) & one long term (7-8 years).

Short Term View (3-4 years)

Healthcare Business

Over next 4 years, company plans to add 900 beds, taking total bed count to 3400. One can assume Max India’s share at 1700 beds. Assuming 2Cr per bed gives valuation of 3400Cr, assuming 2.5Cr per bed gives valuation of 4250Cr.

The company has EBITDAR per OBD of 20L. At 1700 beds, this gives EBIDTA of 350Cr for Max India. Assuming EV/EBITDA multiple of 15 gives, valuation of 5200Cr.

Max Bupa

On non-going concern basis, Max Bupa is actually worthless as cost of float at 9% is about same as cost to get the same amount from financial institutions.

But I feel the right way to think about investing in Max Bupa is as a venture capitalist or PE fund (something like investing in Ola etc.). At such small revenue numbers, the business would not even have been listed but fortunately it is listed and retail investors can own it. The investment time horizon needs to be 5-10 years for Max Bupa I think.

On going concern basis, insurance business needs to be valued at Indian Embedded Value (IEV) but it is beyond my skill set to compute that.

What I have observed is, for general insurance company offering non-participating products, I feel insurance company can be valued at some multiple of float. There are two parameters that are important in growth of float - underwriting profit/loss and how much, investment record.

For a company generating float at small cost (small underwriting loss, 2-3%) & average investment record (8% yield), insurance business should be bought at discount to float.

For a company generating float at underwriting profit (2-3% or more) & average investment record (8% yield), insurance can be valued at float or some small multiple of float (1.2x-1.5x). If investment record is exceptional (12%+ yield) & underwriting profit, business can be bought even at 2x float.

At current stage, max would be valued at 600Cr kind of valuation. Bupa bought 23% stake at 207Cr in FY16, valuing business at 800Cr. I expect this business can be valued at 2000Cr in 3-4 years.

This gives valuation for Max India in the range of 5500Cr-7200Cr in next 3-4 years.

Long Term View (7-8 years)

If company does manage to get 5000 beds, then at 20L EBITDA per bed, EBITDA comes to 1000Cr. Assuming EV/EBITDA multiple of 15, Max India’s share would be valued around 7500Cr. If you add rising healthcare costs + more operational efficiency, this business can be valued at 9000-10000Cr.

For Max Bupa, I hope it can be valued at 3000Cr.

Views Invited.

Disc - I am invested in the stock and my views are biased. There might be errors in my valuations/assumptions or they can be completely wrong. I am not SEBI registered analyst. Investors are advised to do their own diligence before investing in the stock. Stock constitutes more than 5% of my portfolio and no transactions in last 30 days.