Isn’t it too low for an IT service company?

@aashish2137, Majesco cannot be categorized as IT services company. It is predominantly, an IT Products company focusing in the Insurance space. It is in the initial phase of life-cycle presently, investing heavily in development of products. As you can read above, almost 14% of sales are spent on products R&D in FY16.

Pls go thru the detailed Indianivesh report (link given above) to understand the business, valuation and projections.

1 Like

Short Summary of Q3 conference call:

we have also prepared few other summaries. Sharing here: https://goo.gl/5RTk0o

Read disclaimer for summaries here: https://goo.gl/HELov8

$MJCO Released Q3 on 23rd , Below is concall details.

http://seekingalpha.com/article/4038850-majescos-mjco-ceo-ketan-mehta-fiscal-q3-2017-results-earnings-call-transcript

Renaming the topic to Mastek Ltd as demerger has completed a long time back, and Mastek is now operating as an independent company.

Instead of opening a new thread, I think it is better to rejuvenate an old thread so the historical perspective is retained.

In FY 2019, Mastek has reported 101 cr profit, and H1FY20 PAT is all most 48cr.

Due to the Brexit uncertainty, Mastek is facing a headwind in term of revenue growth and PAT. However, looking at the Brexit situation wherein the Conservative Party has taken the lead in the opinion poll, Brexit is likely (high probability) to be resolved soon. This shall give Mastek more order book visibility going forward.

Mastek is currently operating as a plain vanilla IT Outsourcing company earning more than 75% of revenue through Time, and Material assignment and trend is not likely to change anytime soon.

Mastek has a market cap of around 950 cr (has increased by 250+ cr in last 2 weeks) and cash and cash equivalent of 200 cr on its balance sheet. Plus they are aiming to monetise their Majesco stake, which shall bring them around 200-250cr after-tax (approx). In addition, Mastek management is trying to sell some real estate which may fetch around 50 cr to them.

Essentially, Mastek has around 500 cr of cash and cash equivalent plus an existing business which is generating 100 cr PAT every year (no major CAPEX planned). I think the stock is well-positioned considering the risk-reward ratio.

Dis- Invested for a long time so views are biased.

.

5 Likes

Mastek is on a divesting spree recently. They have sold stakes around $16 million last month, plus additional sale of $6 million today, fetching around $22 million in total so far (150 + cr), and still they are to sell approx half the remaining stake.

Looks like they are building a war chest for further acquisition going forward.

2 Likes

Mastek (UK) Limited, a wholly-owned subsidiary of Mastek Limited, today announced that it has signed a definitive agreement to acquire the Middle East business of Evolutionary Systems Arabia FZ LLC through its group company for USD 65 million. The transaction would be subject to routine regulatory approvals and customary closing conditions.

HDFC Sec Report

3 Likes

I’m researching this company. Went through the thread. Long time holders, such as @paragbharambe,

-

what are your thoughts on the promoter pledged holding? Apparently 57% of promoter holding is pledged (as per screener.in). Does anyone know why?

-

They also have a big debt of 333 cr which increased from 70 cr last year. Any idea why they are taking on so much more debt?

Thanks!

In term of promoters pledging, I am not too worried about it. Most, or maybe all promoters have a shareholding in Mastek and Majesco. So one or more of them may have used funds to increase shares in Majesco by pledging Mastek share. I have observed company management over many years, and I have not found anything to suggest their integrity. Mastek might not have grown rapidly in the past, but in term of management integrity, they are at the top league.

Mastek has bought a company Evosys in Feb 2020, and it is a big transaction for Mastek. They have paid around $90-100 million for the company. As part of the transaction, they paid cash to the tune of $60-65 million and the cash was raised through debt. As Mastek has a global presence and 90% or more of their income coming outside from India, they get access to the cheap global funds. I reckon the cost for the Rs 300 cr+ debt will be less than 4% per annum, which is not bad.

Bear in mind that they have cash and cash equivalents of Rs 300 cr + Majesco stake valued around 80 cr as on today. So if they wish they could repay the full debt, instead they prefer to keep the cash.

Evosys acquisition could be the game-changer. In the current quarters, approximately two months of revenues have added 12 cr of Profit in Q4. Barring Covid-19 situation, I won’t be surprised if they start reporting 50 cr PAT for each quarter within next 3/4 quarters once COVID situation improves.

Note- Figure mentioned above are are approximate. Please refer to company publications for exact numbers

6 Likes

Majesco US is being bought by PE player for $594 millions.

Mastek is having shares worth more than 80-90 cr (as on yesterday’s price) in Majesco US. The PE player is offering $13.10 to each Majesco share, which is 74% premium to yesterday’s close price.

This shall result in Mastek earning around 130-150 cr by stake sale which is a good news in the bad times.

5 Likes

Over all things are looking favorable with good track record on bottom line for the last 3years. For the business which is dependent on UK and UAE. Post covid do you have any update…as i couldnt find any?

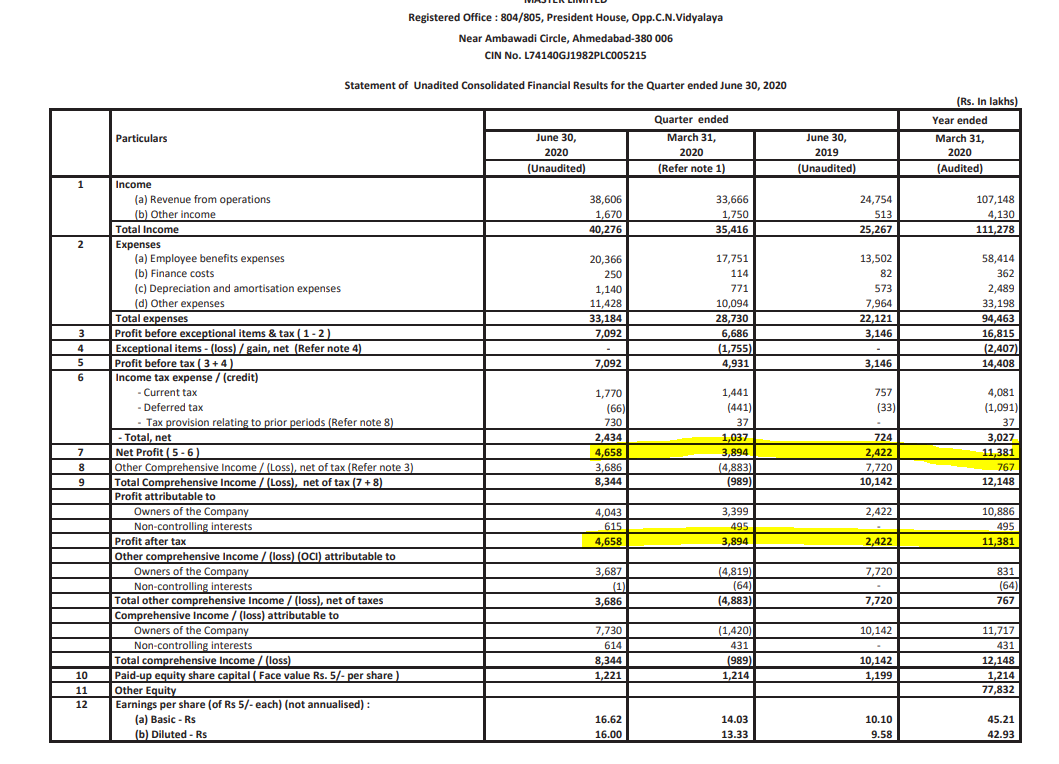

Another set of stunning result by Mastek. Q1 PAT of 46cr, highest ever profit for Mastek. Looks like Mastek has handled Covid very well.

@pgramle- Mastek revenue does not rely much on UAE. They acquired a company in Feb 2020, which has contribution from gulf region, hence UAE is shown. However, UAE contribution is not much as compared to revenue from UK/US.

4 Likes

Indeed a stellar quarter. This is only the first quarter with full impact from the acquisition.

-

Revenue up 59.4% YoY.

-

Net Profit up 92.32% YoY.

-

Another positive. Promoters pledge is removed

https://www.bseindia.com/corporates/shpPromoterNGroup.aspx?scripcd=523704&qtrid=98.00&QtrName=June%202018 -

There is also circa 200 Crs anticipated via the Majesco sale

2 Likes

Q1-FY 21 Con Call Notes.

Key takeaway from the con call

- Mastek will get 200 cr from Majesco sales. It is the net amount after paying tax (or considering the structure of the deal tax may not be required)

- Current performance can be sustained in Q2 and can be accelerated in H2

- Q1 has been a real challenge.

- A number of new contract signing extended into Q2.

- US - Struggle goes on.

- Plan to divest non-core asset and invest in incoming generating assets.

- Aspiration- Become a recognised mid-cap. This seems to be a new focus for the management as they iterated this word a few times during the call. This indicates to me that Mastek will be a lot of things investors want to hear with a focus on improving profitability. For example, they can increase the profit by cost-cutting (already doing it) or keeping bench level very low. This may be good in the short term and boost immediate profitability, but when the project starts coming in, they will struggle to get the resource on board.

- Price Pressure is an ongoing trend.

- Revenue down Q-Q and increased risk of client bankruptcy.

- Canada and the Middle east- the additional market for cross-sell.

- Canada and European market new opportunity.

- Focus on local hiring.

- Planning to hire 100 + trainee this quarter. This shall impact profitability for next 2/3 quarters.

- Capital allocation priorities- Conserving cash, repaying the debt, reinvestment in the business. They are not keen on increasing dividend or buyback at this moment and focusing on navigating COVID crisis. I think this is good (exactly what many investors want to hear)

- Evosys Value by the Delivery approach to execution- It is an outcome-based approach to delivery. This is quite different than other company offers. Evosys Developed various IP assets to aid this.

- Cross Sales- Pursing it in all geography.

- The average size of Evosys deals is $200,000-300,000, which is small from Mastek’s point of view. But it offers Mastek immense cross-sell opportunities. The biggest cross-sales deals Mastek signed in Q1 is $4 to 5 million and 4- 5 deals are in the range of $1 million. I think next 4-5 quarters shall provide Mastek with quite a few cross-sales opportunities. Management has said that Evosys customer acquisition engine is a major decision-maker for acquiring them.

- Addition of 40-50 cr of cash every quarter.

My view

Mastek has 170 cr of cash + (40-50 cr) of cash addition every quarter. By the end of March 2021 (optimistically assuming that COVID situation does not become worst than the current), Mastek will have approximately 300 cr of cash. In addition, receipt of 200 cr shall repay most of the existing debt. In a nutshell, Mastek will be more or less debt-free plus 250- 300 cr of cash by the end of March 2021 and generating PAT of around 180 cr.

At a current price of 1400 cr, Mastek is valued at PE of 7 @FY 21 earning. Based on the current valuation, it is attractive.

On a technical side (I am not an expert in this, but read few things from on valuepicker), the stock all-time high is 608, which is not too far from the current price. Once it breaks that price, there is a high probability of it reaching new highs.

Please refer to reasearchbytes for full voice transcript of the call. You may need to register to hear the full transcript.

Here is PDF of con call transcript .

Note- I am holding Mastek and views are biased.

14 Likes

Discloser: I am holding this stock in my personal capacity.

Hi,

How to access FY19-20 annual report, I tried to google around but couldn’t find it.

Every company has to report to the exchange regarding updates related to the company. Quarterly results & annual report being the topmost in that list.

Companies also report public data related to investor meet intimation, newspaper advertisements, dividend declaration & much more. For such info visit the corporate information tab https://www.nseindia.com/get-quotes/equity?symbol=MASTEK

Thanks for the reply. I think I should have been more elaborative while framing the question.

Question :- I am looking for FY2019-20 Annual Report

Resource looked already : BSE, mastek web, google, tickertape etc

FY2018-19 Report was published around 26 June 2019, Hence I was thinking for FY19-20 Annual report should have been come by now.

Email sent to investor.relations@mastek.com unanswered for last 2 weeks.

So anyone has idea what is timeline for annual report publish, Off-course I will get to know via announcement, I was wondering if I have overlooked.

I think they have not yet released AR for FY20. Will need to wait.