Nothing spectacular in result. Net profit number disappointing, but expected at this phase of expansion. What is more disheartening is tepid topline growth. One may get opportunity to add at around 2 times sales valuation.

The company’s foreign subsidiary Kaya Middle East, DMCC, along with its local partner has entered into a share purchase agreement to acquire 75 percent beneficial interest in Iris Medical Centre LLC situated at Abu Dhabi. Iris Medical Centre LLC carries out business of skincare services and operates one clinic in Abu Dhabi. Iris Medical Centre LLC has reported revenue of AED 2.24 million as per its last financial statement for half year ended on September 30, 2015. Kaya had reported consolidated profit of Rs 2.6 crore in Q2 FY16 (Aug-Sept) against Rs 12.6 crore in corresponding quarter last fiscal. The company has added 4 clinics and 35 Kaya skin bar outlets across format in India in Q2 FY16. Overall in India Kaya has 106 clinics and 64 Kaya skin bar outlets and operates 19 clinics in Middle East.

CONFERENCE CALL - from Capital Markets

Kaya

Looking at hair category for growth which will be introduce in Q2 FY17

Kaya held conference call to discuss the results for the quarter ended December 2015.

Following are the key highlights of the call:

For Q3 FY16, the net sales grew by 11% to Rs 95.2 crore. Same store growth (SSG) is 7% and 3% at constant currency level. The net profit de-grew by 70% to Rs 3.5 crore. Like to Like net profit is Rs 7.6 crore, de-grew by 38%.

Kaya has added 1 clinics and 37 Kaya Skin Bar outlets (16 SIS and 21 Modern trade) in India & 1 clinic in Abu Dhabi in Middle East in Q3.

Kaya India

The net revenue growth was 7% to Rs 47.6 crore. SSG is -3%. The loss at net profit stood at Rs 2.1 crore.

Collection improved by 8%. Collection SSG growth was -3%.

Ecommerce grew by 95%, contributing 12% of overall product sales.

Launched 2 Products - Comedone control and Blemish Control re-launched.

The company has total 107 clinics and 104 KSBs in 27 cities, 16 states.

Ticket size grew by 9% to Rs 7650 (SSG: 11%). Technology investments have helped improve ticket size and upgrade Mix

Customer count decreased by 8% to 57289 (SSG: -15%).

Cure category has de-grown by 1% (SSG: -5%). Its contribution to India’s revenue was 69%.

Care vertical grew by 23% (SSG: 15%) backed by PAN India Introduction of New Beauty Facials. Its contribution to India’s revenue was 13%

Product category (including E commerce)de-grew 1% (SSG: -7%). Its contribution to India’s revenue was 17%. Overall Products category (including KSB formats) grew by 28%. 2 discontinued products got re-launched in mid Dec 15

Kaya Middle East (KME)

The net revenue growth was 15% to Rs 47.6 crore. Same store growth (SSG) is 15% and 8% at constant currency level. The net profit declined by 23% to Rs 5.4 crore.

The company has total 20 clinics in 8 cities, 3 countries.

On SSG basis Customer count has grown by 8% to 16186; Ticket size grew by 3% to $ 444.

Cure category has grown by 13% (SSG: 11%). Its contribution to India’s revenue was 79%. Hair free technology scale up in UAE (7) & Oman (1) helped to drive growth

Care vertical grew by 7% (SSG: 14%). Its contribution to India’s revenue was 9%

Products portfolio grew by 7% (SSG: 6%). Its contribution to Middle East revenue was 10%

Other highlights

Clinic has to operate for 12 month for calculating in SSG. Stores tracking now for SSG is 89 clinics.

Taken price hike in some categories in December

Consumer sentiment is not in line with the expectation. High end customer is retained, whereas losing customers at lower end level.

Consumer promotion in Q4 to get customers back at lower end. Also communication exercise to make aware of the company offering to customers.

Looking at hair category for growth, this will get introduce in Q2 FY17 in 50 – 60 clinics.

The mgmt said at India level, it is in consolidation phase as far as opening clinic is concern. However, KSB will see 20 – 30 new opening on annual basis.

Middle East will see 2 – 3 clinics opening on year basis.

SSG in FY17 – looking at hair category to build SSG growth.

The capex for KSB – Rs 15 lakh at store level, Rs 5 – 10 lakh at SIS level and Rs 2-3 lakh at consumer level.

In Middle East, the company business will not get impacted in near term from present turmoil.

The company is looking at bring products contribution of Middle East to India level. It is also looking at increasing overall contribution and stay upwards of 20% in India.

Hair offering business – lots of offering is there which will be come in phase wise manner. Margin for it will be similar to skin care business

The company gets 65 – 70% sales contribution from Delhi, Mumbai and Bangalore.

Customer advance is Rs 75 crore at end of December 2015.

One of friend has very bad experience at KAya clinic in navi mumbai… this is what I heard-

There are many customers who are asking for refund- The company gave huge discounts in the month of August giving tall claims and now when the results are not evident, customers are demanding their balance advance money. The company is not responding well to the customers feedback.

3 Likes

@learning_ investor

worrisome for the brand

The stock had break out from 700 levels to 1000. Can you please throw some lights on recent developments 1) Management Change 2) New products 3) Revised strategy of refurbishing the old well run stores and closing down the loss making?

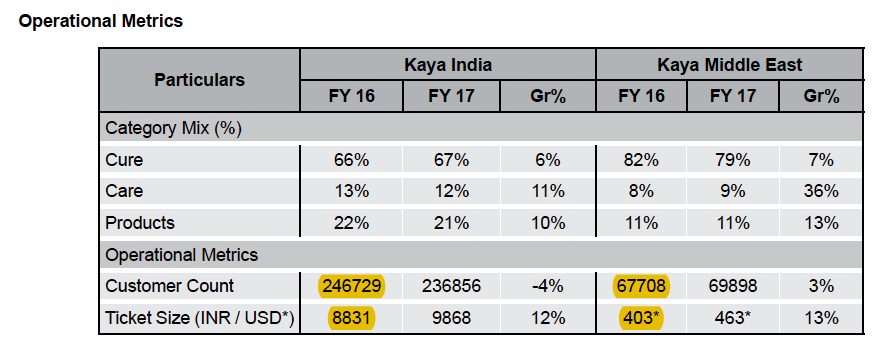

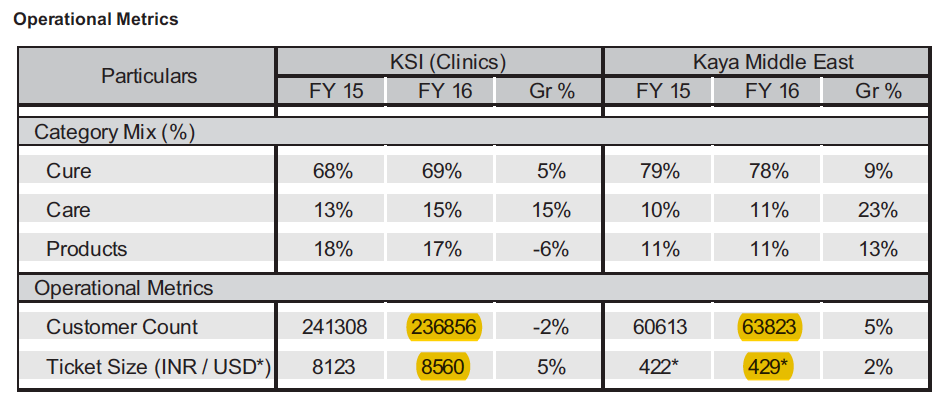

Was going through the Annual Reports for FY 16 and FY 17. Observed that the customer counts for FY 16 in the two reports aren’t matching. Same is true for the ticket sizes. Anyone has observed this and can explain the anomaly?

From AR 2017

From AR 2016

2 Likes

no news as such. Buyers are betting on shift from unorganized to organized market. Further, investment in Kokuyo camlin by Vijay Kedia in December quarter is endorsing this hypothesis of organized sector catching market fancy.

If you see FY17 and FY16 customer count, it is the same number left like that. My guess is that they forgot to update it.

It seems they have closed out 2 stores this quarter… From. Last quarter

Also, is this company does earnings call??

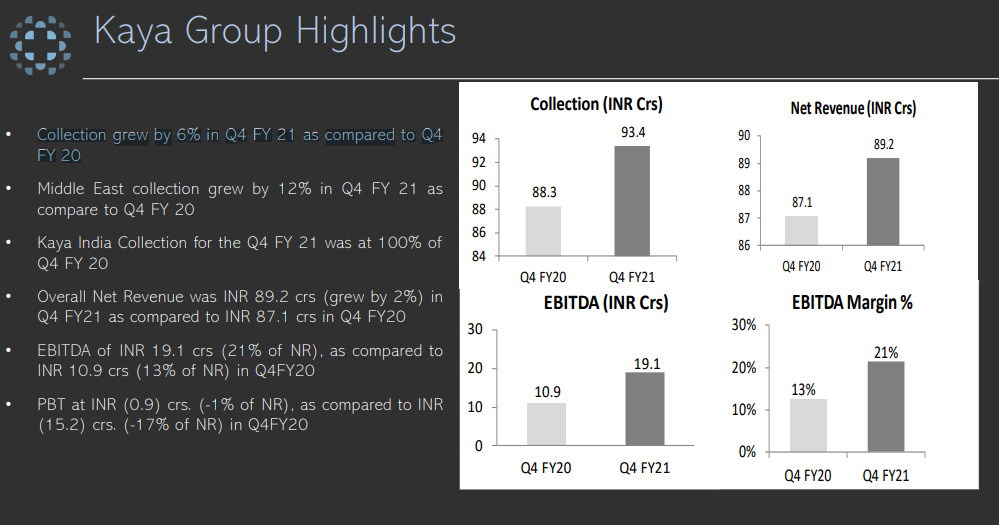

There is nothing great in Q3 numbers. The only thing worth noticeable was increase in EBITDA margin to 16% as compared to 7% in Q3-19. Marginal decrease in topline.

1 Like

R Damani has bought 1.11% stake in Q4. Are there some good developments going on in company?

RD bought 1% position in many businesses over the last couple of months. These positions are probably rounding off errors in his portfolio i wouldn’t focus too much on the news.

From a valuation view this looks reasonable enough to do some work. It’s branded consumer business which trades at 1x EV/Sales.

The business had a lot of issues around profitability structure (even before COVID) and the way they reorganize the business in a post covid world. So a lot of known unknown’s here. So one would have to do a bit of work around it.

1 Like

As per screener, Damani was not a shareholder in the March 2021. Has he sold his stake in Kaya? Can anyone confirm the same.

Moreover, their Book Value was 90.95/share on 15th June.2020. which reduced to 41.7/share in June 2021. This phenomenon can only be factored due to utilisation of reserves right or can there be any other factor?

Yep Damani is out of the name. You are right re the decline in BV using reserves (cause of losses).