@Yogesh_s If there are no red flags, why do you think the stock is not available cheap? I want to know your thought process as I value it highly.

This is growing at 36 plus percent and quoting at 17PE. An FMCG stock with such large addressable market, excellent financial health and proven execution capability of the management over the last 3 years to keep growing at this break neck speed, a skin in the game first gen promoters, backed up by marque investors with only 3% retail ownership just 2 months back. If we forget that this auditor resignation taking place, I kind of think that this is an excellent value.

Hi,

Disclosure: Invested 20% of my PF.

I think people should only purchase this stock if they are having minimum of 5 year view. In short term it is very difficult that stock is going anywhere. This stock was highly owned by institution and they will be having tremendous pressure from unit holder to come out. So, if any of them will keep on off loading, prices will be in this range till the market mood is not getting euphoric.

So, according to me, it is still in fair value zone from the next 2 years perspective. I was waiting that some of MF will off load, so that I should get it somewhere between 75-100 Rs. In this price range almost doubt on number thing would have got priced in. But, Mutual funds are people with strong nerves especialy MOSL and SBI, so they are not going to sell on too much less than IPO price in hurry. They will only sell if there is some real issue that too in phases.

Till that time averaging slowly for next six month and trying to get information from real world about their products.

Don’t value it from the time of euphoria, but value it from margin of safety point. And, according to me if doubt on number thing is 30-40% correct, then it can go to somewhere around 75-100 and that to in next 2 years. My suggestion will be to invest in SIP over next 2 years.

I have written this in Vakrangee thread after both have fallen. Got criticised for having opposite view. But understand the risk before investing- don’t see only upside; try to see down side also.

IMHO, we need to decipher the reasons for auditor,s resignation and if the same is linked to cooking of books or dishonesty of promoters etc, we should keep away from it, whatever the price.We have seen in the past as to how the stocks fall without any recovery and finally get converted to penny stock.Its a pity that no one is really able to investigate the reasons for vakrangee,pc jewellers, kwality, shipping cable and many others and only sufferers r the retail investors.

Sooner or later almost everything reverses to its mean. Market was pricing it 40-50 PE because growth was visible. Even now the underlying assumptions upon which that kind PE rating is based, stays intact. Ratios are low because in last three years they have expanded their equity base multiple times. If their growth story is intact, in couple of quarters EPS growth should catch up.

When investing in a company, promoter background is as important as financials. I have tried searching it extensively, but there are no red herrings about the promoters, at least in public domain. In fact, if we put ourselves in the promoter’s shoes, and think, is it in his best interest to swindle away few hundred crores or let the company flourish so that his own networth multiplies couple of times, I think second option is in his best interest. Here is a guy who left his Govt PSU job and started selling juices from his minivan, so basically for last twenty years, he is just chasing his entrepreneurial dream. It is highly improbable (though technically possible), he is willing to let it go just to make few quick bucks.

About the concern raised by Deloitte, no one would know for sure, but my guess is they may have arisen due to two factors. As they basically operate in Bharat, they do lots of cash transactions, some of which may be virtually impossible to trace. Or, as they supply to a Govt entity, there may be some greasing up palms of higher ups, which became apparent while auditing.

The promoter is a rustic guy from UP, not a Jamnalal Bajaj and Harvard alumnus and spouse of a super banker who had the technical skill set to hide their questionable transactions from forensic auditors and investigating agencies.

Just adding to your reasons for Deloitte resignation-

Increase in auditor liability, much more stringent norms, SEBI order on PwC could also be among the basket of reasons for the resignation. The below video talks about these aspects towards the latter part.

Just a word of caution, New Auditor was earlier auditor for Bhushan Group (Listed as well as Unlisted Co.) & latter on, I think they were removed when both the Companies were admitted to IBC. Play safe…

Mehra Goel & Co is the ninth largest auditor in India having Nifty 50 companies like SBI and ONGC among its clients. In terms of client turnover, its bigger than both KPMG and PWC. Please find the attached document to confirm and in case of any allegation, please link relevant documents / websites so that fellow boarders are able to take an informed decision, thank you. PR-317.pdf (141.5 KB)

One can’t give proof for each and everything & sometimes you need to draw inferences also. I just shared what I was aware and that’s the fact which you can check yourself. It is just a word of caution for fellow Investors. The report which you have shared is old one and things have changed a lot after Bhushan. I can assure you at the moment Delloite is no. 1 in audit and if they are resigning due to certain information being withheld etc don’t take it lightly. Just do due diligence…Best of luck!

Its now Delolite Vs Manpasand, if Manpasand Comes out clean the entire onus will be on Delolite for the erosion of Shareholders wealth. Delolite should have been more informative in their resignation so that investors could have taken a calculated risk. The auditors might not be satisfied on some data provided by the company (without backup documents). Had the disclosure been made by the auditors, I as an investor would have discounted that material fact at a share price fall of 10% or 20% or 30% or 40% or 50% or 90% as per my understanding /risk appetite.

We have so much faith on Delolite that even after audited results we are not giving clean cheat to the company. I think if Manpasand comes out clean that faith ob Big 4 will be on a risk.

I am neither in favor of company nor in the favor of auditors I am just concerned about the retail investors who are stucked at high level and are left clueless.

My personal advise for new investors would be not to take any investment decision at this stage but just track the stock as it will give a rich experience. There are other stocks to invest which have also fallen considerably in the recent correction

Disclosure : Not invested and not even interested but just tracking the stock for increasing my experience.

Their decision to expand to other countries is, in my opinion, disconcerting. There’s no dearth of opportunities in India. There’s substantial room for growth in consumption of beverages. Why would they want to expand to uncharted, foreign territories?

Also, a question that has been plaguing me - What’s the upside for Parle in this collaboration?

Manpasand benefits immensely due to the extensive reach of Parle throughout the country. But, what’s in it for Parle?

Article says - “Manpasand, which became the country’s first listed non-alcoholic beverages firm with an IPO in June 2015” - Tata Global Beverages has been there for a long time.

Looks like the article is promotion for Manpasand. It just glossed over the auditor resignation and 50% drop in market cap which is not an everyday affair.

Please do fact checking before posting. Tata Global Beverages is a Tea and Coffee company. 80% of sales comes from TEa! The only beverage they sell in Indian markets is the highly overpriced Himalayan Mineral Water which has sales of less than Rs50cr. Even out of the total sales their India sales is less than 30%.

The company management here is talking of expanding to different countries when their core proposition is drinks that appeal to rural segment and regional tastes. I have a few questions here: Has it already covered the entire rural/semi-urban Indian market? Or is it expanding too thin by planning to enter other countries?

Other countries’ consumer tastes will be very different from their existing customers. Does it have the resources to understand and deal with the new customers? Isn’t it more profitable and safe to penetrate existing markets?

Will be very interesting to watch how the story unfolds. As of now, my doubts about the management are still there. Disc: not invested

The company has NOT announced any global expansion plan, nor is any mention of it in company announcements, AR etc. Its not that the company is spending money in global expansion in next quarter, or even next year onwards, Its just big talk and need not be given any importance.

Boarders in this subject may be divided into two categories. One, who burned their fingers in the recent crash, and take the company as a fraud. Two, who invested in it in the lows for whom everything is rosy and glossy at that price. The reality lies somewhere in between.

The basics never stacked up. The throughput per store was way too high. For example, Maggi is ~1200 crore at 8 lac retailers. Manpasand at 700 crore for 4 lac retailers means that it would have a throughput per store higher than Maggi. Does that seem credible? To clarify – it is possible for brands to have a higher throughput per store than Maggi. But those are typically brands in high price points and more urban-focused (think Cadbury Silk) – the opposite of what Manpasand claimed.

Low Tax Rate

Now if the sales figure of Manpasand is suspicious then the profit figure should be suspected too. In which case, the question is where are the cracks in the accounts? We note that Manpasand paid a tax of only Rs6 crore on a profit before tax of Rs56 crore. This is exceptionally low and is the first red flag.

Manpasand has never had high tax payout – not even in the years when the fixed asset growth was low. In 2012, it had sales of Rs85 crores, pretax profit of Rs6.82 crores and paid a tax of just Rs73 lakhs.

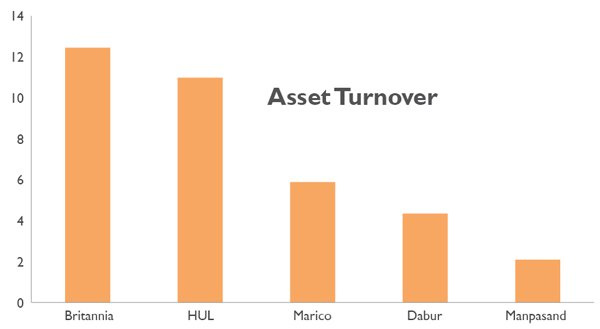

Low Fixed Asset Turnover

Clearly, Manpasand has one of the lowest asset-to-turnover ratios among the FMCG companies. And it is raising money to invest in more fixed assets. Over a period of time, if these assets don’t sweat enough, the return on assets will slump. Will investors be left with high valuation stock with strange figures on its profit and loss and balance sheet?

Disc: Never Invested, Not interested to invest even… just trying to learn things to avoid such companies in future…

As you had said you are learning things, it would be apt to learn couple of new things too before starting to form opinion ahead of facts.

Comparing Manpasand to Britannia, HUL and others is like comparing apples to oranges. These four are decades old established players who have considerable bargaining power in contract manufacturing and outsourcing and need not put a new plant every time they launch a new product. However a new player will be at the mercy of contract manufacturers, so need to put own plants for competitive advantage.

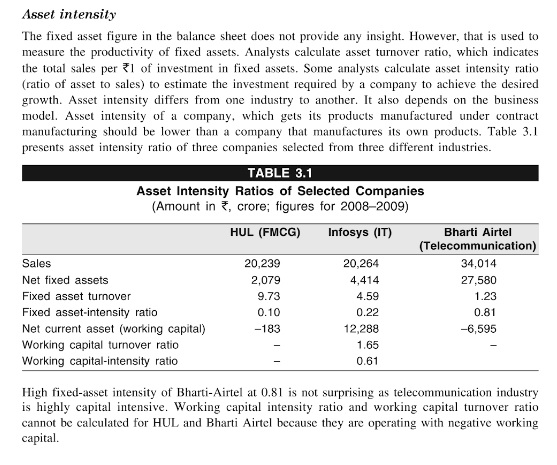

Check the image below to understand how asset intensity is different for different industries.

I just quoted the stuff from the article… The HUL vs Manpasand might not be relevant, but for a company which dilutes capital regularly, pays low tax, negative FCF, if the company is to ultimately grow, I would like to see increase in FAT (Fixed assets turnover) ratio… Else they will have to rely on debt from now on, as further equity dilution may not be possible (due to lower price, if they raise money, dilution will be even higher. Also, their may not be many takers.) Compared to 2013, their FAT ratio has declined y-o-y every year. Why are they adding capacities, if they are not utilising them at optimum level?

Free cashflow has never been positive for the company… is it a sign of a good company?

and if the debt increases the way they were raising cash from share sale, they will soon be spending 30-35% of the profits before tax in interest payments (assuming Rs 300 cr loan).

Considering their capital work-in-progess has risen in 2017-18 from 18 cr to 181 cr and net fixed assets by rs 86 cr (may be 95 cr, considering dep. dont have current figures for gross assets)… and just 40 cr investments to speak off… their capital requirements to pay off current expansion and any plans for exports, will need some capital… they have already borrowed 95 cr in 2017-18…

Comparison to maggie looks logical to me though… I know they are not in same segment and it is not apple to apple comparison… still both are food items… retails at same kinds of shops… I can see maggie everywhere but not mango sip… It is about same price point as Manpasand… Maggie sale per store is Rs 15000 per year per retailer (1200 cr/8 lacs)… vs manpasand’s Rs 17500… I dont think they have that much visibility.

Data on the throughput, of course, can be questioned…

So, all in all, I am pretty bearish on the company…