I fail to understand why ROEs are not improving… Yes, they have raised capital on regular basis but why not leverage… they still have no debt… even after say 40% increase in profits ROE is falling…

does not look like an FMCG types balance sheet to me…

also, considering I have seen this mostly in supermarkets, where they are sold as 1+1 free and they do sell. make of it whatever you will, but for me, if this offer is from supermarket, they may be clearing out unsold inventory before it expires and if the offer is from the company… i doubt their margins…

As far as these fmcg labels are concerned - i dont remember who said it - but i remember reading about it in one of the wb letters in reference to something else but i think its apt here

How many legs does a dog have if you call its tail a leg? The answer is 4, because calling the tail a leg doesnt make it a leg

Apologies, but i couldnt resist it. Myself victim of calling a tail a leg in some cos invested in past

My humble submission - You’re right, Paper Boat has a much higher brand recognition compared to Manpasand. But, Paper Boat is a largely urban phenomenon. Whereas, Manpasand makes claims of catering to rural areas, price sensitive customers. Both companies operate in the same industry but target customers are as different as chalk and cheese. Paper Boat reported sales of 69 crores and losses of 78 crores with an anemic growth of 12.5% with a valuation of close to Rs. 700 crores. On those metrics Manpasand sure seems alluring. But, their relatively high profit margin despite the complimentary offering of one bottle on every purchase is astonishing.

It seems too good to be true.

Brand recall by itself does not determine a company value. If it were so, Ballarpur Industries Limited today would have been trading at a 10x price now.

About FMCG play, no one is calling it a pure FMCG play like HUL or Nestle. They are pure FMCG plays and market also give them P/B value of 50+ and 27+ respectively.

The real question here is - Is it a mispriced opportunity due to market apathy at P/B of 1.3+ and P/E of 15+ as its growing reasonably well, provided that they are not cooking their numbers, in which case, all bets are off.

Let me clarify why I didn’t take sales into account. For companies so small in a market so large, looking at Sales/Profits doesn’t usually give the complete picture. I doubt Manpasand’s numbers because of lack of visibility of its brands while I value Paper Boat higher (relatively), because I value it more as a startup going through cash burn and building its presence. It has got visibility as it has got a good brand and very good products and a good distribution in a short-time. That to me means a lot more in a market as big as ours in a segment sticky for brands. If you had to choose which of these two is close to Coca-Cola, what would it be? That was my thought-process in looking only at brand-recall, because I was looking at longevity. Anyway, this is by no means a parameter for selection but its a parameter for elimination. I understand each one thinks differently and will have a different opinion.

@Capsule91 - The idea is from Munger’s “Practical thought about practical thought” where he dissects in hindsight how a company like Coca-Cola may be built. The idea is that the company has to last, a long, long time - Probably a 100 years or more, have desirable products with great band recall, the desirable product should solve a physiological need (quench thirst, in this case), a unique ingredient that links the physiological need of thirst with the look/taste/brand of the product (the bubbles, the flavour, the aroma for eg. and the Coca-Cola logo in this case).

Such a brand/product/company in its initial stages might start small, make losses but the market size is large in that, it is big to start with, growing (esp in a country like ours) and has great marginal utility. Customers will buy product repeatedly with little thought due to cognitive ease caused by the brand/flavour.

So with all this place, if I had to choose one of Manpasand or Paper boat, the latter is a desirable product/company which has focused on building a brand. It is this part that pays rich dividends (pun intended) over decades of product’s existence. So on a relative basis, one of these is going to last a long, long time because its building its brand while what another is doing is cheap processing type work (railway contracts at lower margins). Think of this as someone bringing pails of water from the river and looking successful at first to someone building a canal to where he wants the water go. The former loses out to the latter though the latter looks to be starting slow showing no results. Switching costs are low for Manpasand while its relatively higher for Paper boat (I gave up Real and Tropicana for Paper Boat and ITC’s B-Natural). Again, “relative” is the operating word.

So with all this place, 50 years from now if human beings in the country are still going to be consuming fruit juices (a certainty), ITC, Dabur, Pepsico and Coca-cola along with whoever builds brands with strong recall (Paper boat) are going to have staying power. At that point, today’s sales matter very little. That doesn’t mean whoever is buying Manpasand or Paper Boat is buying to hold for 50 years but that it has got to figure in the valuation in some way. Sorry for the long-winding answer but its not easy to put down a few disparate mental models onto paper.

Another thing I quickly considered is that if start-up valuations (usually done on Price-to-Sales or some other obscure gimmickry to justify random numbers someone came up with) that Narayana Murthy backed Paper Boat commends are cheaper than what I will have to pay for Manpasand, clearly I will choose Paper Boat any day. Hope that makes sense.

Let me add my two cents on visibility. I had a small position in this stock in one of the accounts I managed. I sold out due to frequent dilution and low return ratios. I thank my stars for this.

Since then I have found Manpasand products in railways, big basket and countless shops in not so posh areas. I often take stroll in different Mumbai slums to check consumer behaviour and changes. I found Manpasand products in many of the shops in these areas. The name on the bottle i.e. ‘Mango sip’ is immediately recognisable. It feels like they do not want to spend on marketing but the product does sell in their targetted areas. I have no idea if this could be a proof for the sales they report. I have a feeling that mgmt renumeration comes from capex

The problem is in spite of countless analysis of impenetrable moat of Coca Cola by Munger and Buffett in Berkshire Heathway newsletters and annual reports, Coca Cola has not produced wealth for its investors in a meaningful way for last two decades.

It is that impregnable moat that has made the company last 132 years and will probably make it last another 100 years. Moats = Longevity. As for investor returns, do look at Coca-Cola’s dividend history.

Coca Cola is a dividend aristocrat. Looking at share price alone would be misleading.

An FMCG company is expected to either plough it’s earnings back into the company or return it to shareholders. Deploying earnings back into the company is expected if the market penetration is low and with scope for growth in sales and volume. The company can then acquire a larger marketshare by either increasing it’s production, enlarging it’s distribution network to increase reach, or by M&A activities that achieve the same. At some point, there is a prospect of diminishing returns; it is at this point where the company focusses on retaining marketshare and protecting it’s brand and margins while returning any excess earnings to shareholders. Coca Cola is at this stage.

The main moat of coca cola is the syrup and more specifically the chemical composition of it. The chemical composition of the syrup is such that it has no taste memory, thus you can drink more and every addotional time you drink the utility of it remains roughly the same and it violates the law of diminishing marginal utility.

This is what he says -

“Cola has no taste memory. You can drink one of these at 9:00, 11:00, 3:00 in the afternoon, 5:00. The one at 5:00 will taste just as good to you as the one you drank earlier in the morning. You can’t do that with cream soda, root beer, orange, grape, you name it. All of those things accumulate on you. Most foods do. And beverages. You get sick of them after a while… There is no taste memory to Cola. And that means that you get people around the world that are heavy users, that will drink five a day… They’ll never do that with other products. So you get this incredible per capita consumption.”

Add to that a large distribution network, brand awareness, pricing strength and population growth - and one can easily see why its an inevitable.

As far as share prices of coca cola are concerned - in addition to dividends coca cola has also done large scale buyback programs over time. The structure of warren buffett’s enterprise requires it to invest in cos that send their money to him so that he can reinvest it in other equally good businesses and if they cant he requires them to increase his % stake through these buybacks. Coke does both.

He has structured compensation plans for his operating managers in the subsidiaries based on how much money they can send to the parent without disturbing their own operations.

So, the movement in share price of coca cola just doesn’t count for him as he views the investment as a property that produces ever increasing cash flows to berkshire over time.

However, for those like us movements in stock prices should count and one should try and endeavour to buy shares when they are undervalued and sell them when overvalued.

@phreakv6

I am not trying to raise questions but just asking your opinion on paper boat and my observations

Have you tasted paperboat ?

I have tasted most of it’s products… Latest one being coconut water…

I feel they are charging exorbitantly high and even if people pay high just to taste it, they won’t be repeat customer.

And if you are going on stocks n inventory… paperboat is much more spread over all the shops from retail to supermarket… reason being they are doing all the marketing to make it a success… They lure shop owners giving them some free things etc… Still paper boat are not sold so fast…so finally super markets keep an offer of buy one get one to clear the stock before expiry…

Only thing paper boat is being successful is … people trying it once due to that Indian attractive names…aampanna…imli…etc…

This Parle is different, the maker of Parle biscuits and not maker of Frooti. Maker of frooti is a direct competitor to Manpasand.

Regarding paper boat, I agree. When it was new and thing, a year back, I bought I think Imli to try out of curiousity here in Australia. To be frank it did not taste good. It just tasted different and I never bought another paper boat product again. I am also not finding these in shops here any more. Even if they are here, it’s not prominent.

But Manpasand is a different market. It is a utility product that we would always like to have in our fridge, for example it is much more convenient to give guests juice than a coffee. People will definitely prefer a cheaper option here if it’s for daily use where Manpasand can make a difference.

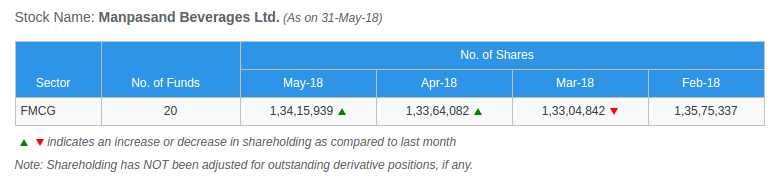

This figure is of 31 May 2018 which is within two days of auditor resignation. So during that period liquidation of mutual fund holdings is highly improbable. However June end data of both mutual fund holdings as well as shareholding pattern would be quite interesting as it will give an idea of the churning that has happened.

Had you taken some efforts to go through the filings and also done some industry research a lot your questions would be answered.

Unilke several other FMCG categories where most of the production is outsourced, in bottling business to get some scale and control over volumes, you have have your own backend. If you see nos for Varun Beverages who does out sourced work for Pepsi, capex is high. Now, they clearly stated that the QIP money raised is for new plants coming up at Baroda, AP & Odisha. Capex typically takes 2-5yrs and that is what is happening. You can’t expect miracles to happen overnight! Topline is growing, new plants are coming, new products are being launched… give it time…

Now Paper Boat is a niche brand targetted at HNI’s and going by your limited understanding, they have hit the right audience. But mind you, to get volumes and scale you have to have the right price point. India is such a vast market with total beverage consumption of just $10bn. US market size is US$240bn! India is much much hotter country with 4x more population! There is enough space for atleast 10 such companies…

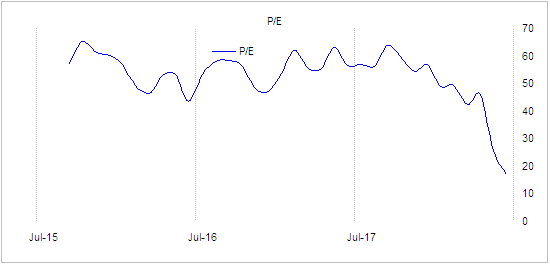

This looks like another case of a wake up call. I looked at the numbers and didn’t find any red flags so far if the numbers are true. Stock could have dropped simply because it was way overvalued going by PE ratio. In spite of the steep fall, PE ratio is still a reasonable 17 which is low given the growth rate and opportunity size but definitely not cheap.