I could not seen any such rise in promoters holding in June quarter…could u please explain?

1 Like

Please refer to bseindia.com and see inside trading under disclosures on Dt 31.05.2018, you will find promoter purchase of 50000 shares valued at Rs 1.11 crore.

1 Like

Presentation made by the company for Analyst meet

Thanks Sandesh.

During interaction in analyst meet, did get any elaborated justification for Deloitte resignation?

Thanks.

Where can we find the summary notes of the analyst meeting? Should the company upload them as part of the regulation?

Discl. Invested at lower level.

1 Like

Went through the Annual Report in detail…

Below are highlights

- Chairman’s address to investors in connection to share price volatility

-clear definition of three segments …three brand ambassadors and their contribution

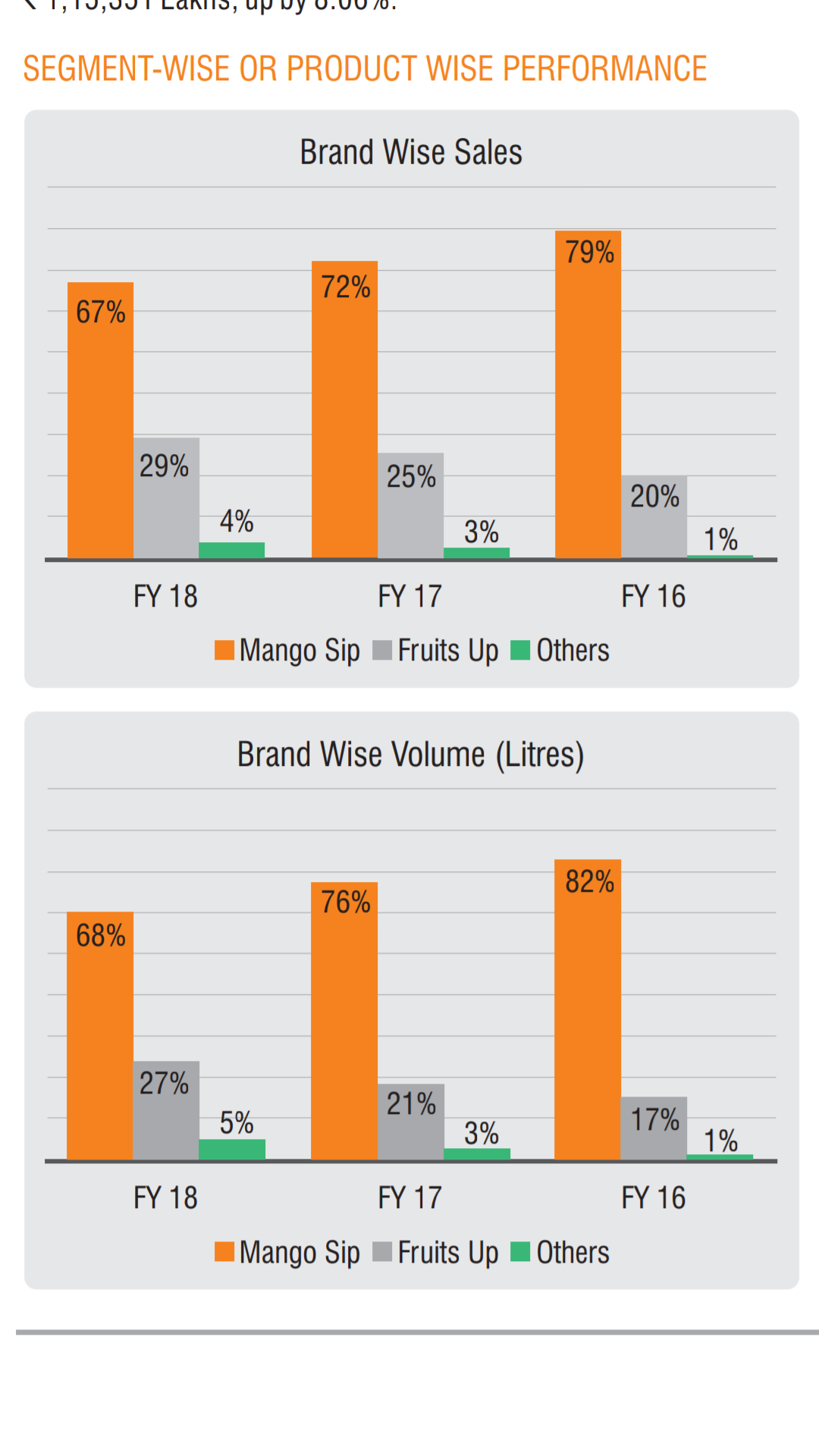

Good to see increasing contribution from fruits up here…and decreasing contribution from mango sip in terms of percentage

- Also in terms of focus of the company, chairman has stressed more on

*Access to 60L retail outlets and 10K distributors due to partnership with Parle G. I believe Parle has loyal customer base and this should help Manpasand gaining same.

- Expansion target 2020…10 facilities and 3.5 lakh cases per day…(from existing 2.25L)

- Focusing on new products…milk based…protein based…fruit based sugar free and glucose based

- Unqualified opinion

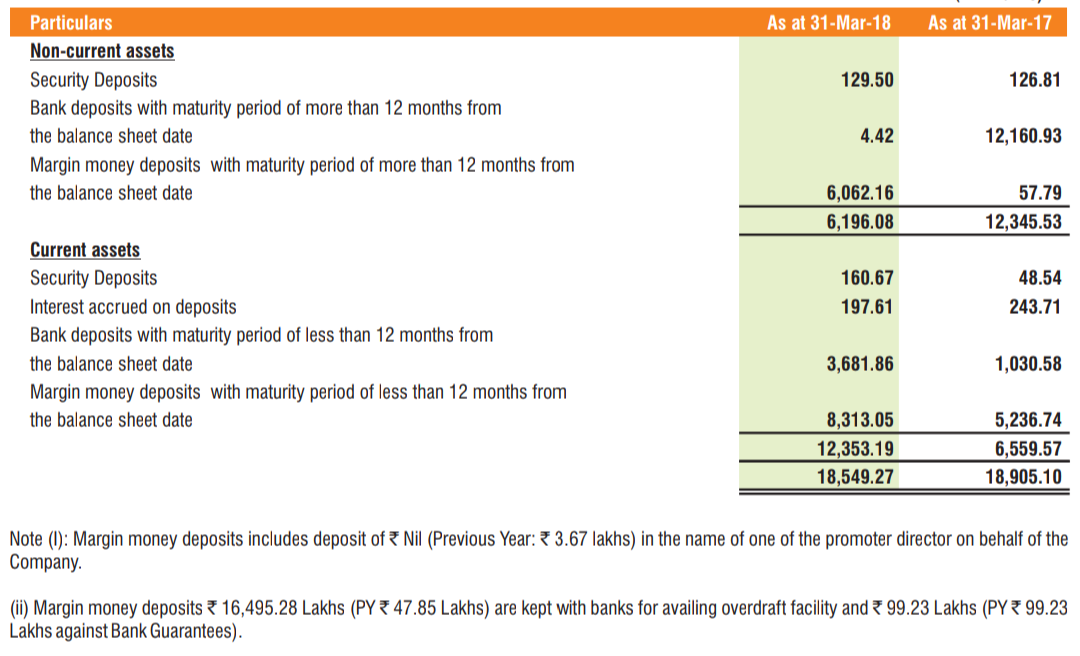

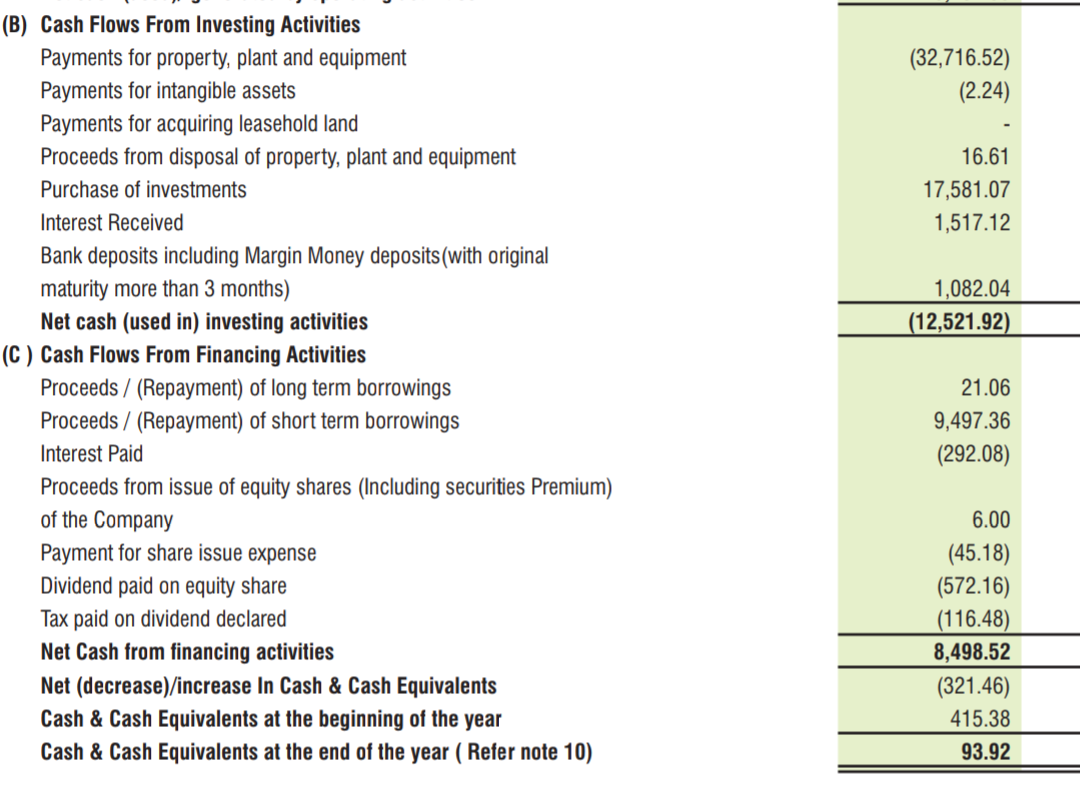

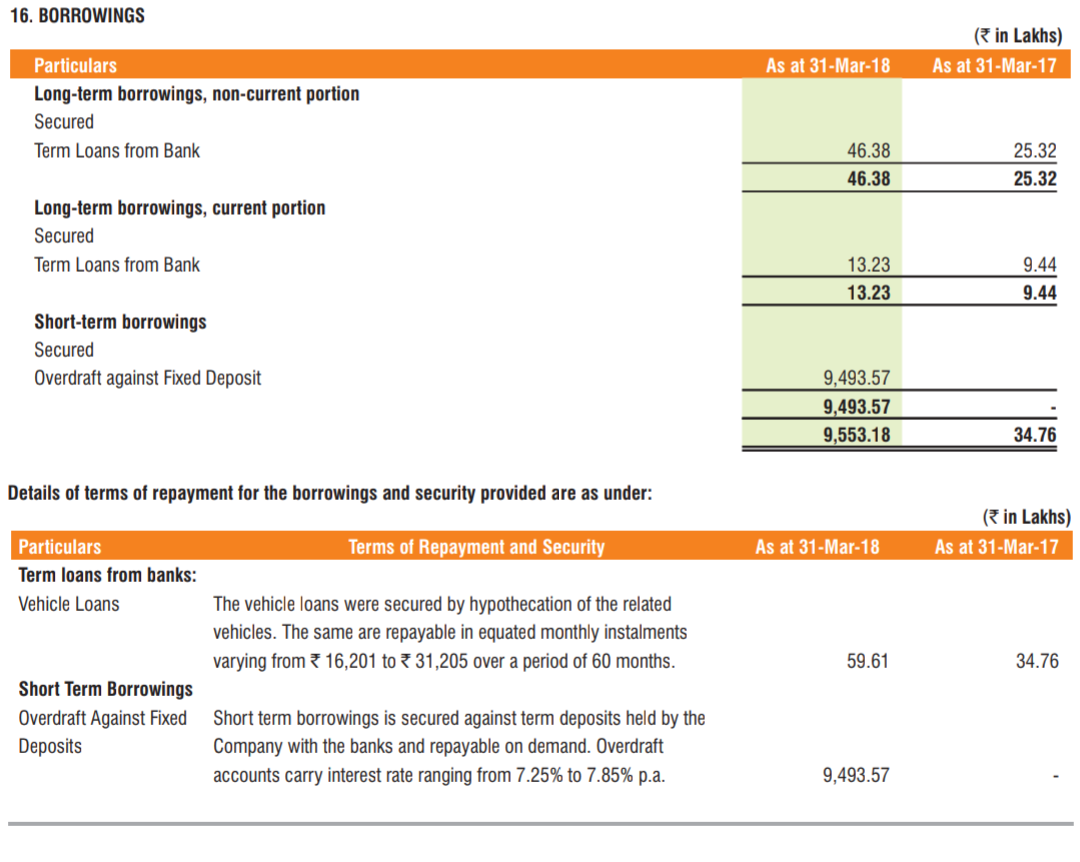

Clarity on decrease in assets and borrowing of 94 crores (except mutual funds investments were sold off for capex)

- Non current FDs were converted into short term FDs and margin money FDs

- 300 crores approx spent on capex 60% of this was financed by sale of MF units they owned

-Short term borrowing of 94 crores is secured against FD

Only concern that remains

Increase in trade receivables…

Disclosure: I hold Manpasand shares and views may be biased

2 Likes

Manpasand Beverages Inaugurates New Manufacturing Plant in Varanasi, Uttar Pradesh. The plant located at UPSIDC Agropark, Phoolpur, Varanasi is spread over 7 acres with an installed capacity to produce up to 50,000 cases per day. The Company has invested around Rs.170 crores to set-up this facility. With the expansion of this plant, the company will now have a manufacturing capacity of around 2,75,000 cases per day, across India.

Apart from the existing seven plants at Vadodara, Varanasi, Dehradun and Ambala, the plant at Sri City will be ready within 3-4 months while the facility in Odisha will be set-up very soon.

2 Likes

Ramdeo Agarwal on Manpasand Beverages

https://pbs.twimg.com/media/DllgEwpXgAAB3Er.jpg:large

https://pbs.twimg.com/media/DllgG51XoAEsqCp.jpg:large

https://pbs.twimg.com/media/DllgKAVWwAAYHMB.jpg:large

Source: Stockedge

3 Likes

With my limited experience ,I can say the statement of any interested party can not be believed in this business.May be, they were trapped and looking for exits.Some senior boarders may share their experiences

2 Likes

One doesn’t need much experience to determine that. I’m also not sure how a business that spends more than twice as much as it earns, dilutes equity continuously, pays a dividend while “growing”, and offers a return on invested capital/tangible asset that is about as much as bank FD can be called an investment; let alone a risk-adjusted investment. May be I am too simple and unsophisticated, but this does not look like a sound investment to me at all. I’d be careful of what people say here because we never know their intentions or their biases.

While we ponder the possibilities, here’s an extract from one of Berkshire Hathaway’s shareholder letters for one and all to read:

Business growth, per se, tells us little about value. It’s true that growth often has a positive impact on value, sometimes one of spectacular proportions. But such an effect is far from certain. For example, investors have regularly poured money into the domestic airline business to finance profitless (or worse) growth. For these investors, it would have been far better if Orville had failed to get off the ground at Kitty Hawk: The more the industry has grown, the worse the disaster for owners.

Growth benefits investors only when the business in point can invest at incremental returns that are enticing—in other words, only when each dollar used to finance the growth creates over a dollar of long-term market value. In the case of a low-return business requiring incremental funds, growth hurts the investor.

And something else about the kinds of business Buffett likes and dislikes:

The best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return. The worst business to own is one that must, or will, do the opposite—that is, consistently employ ever greater amounts of capital at very low rates of return. The worst sort of business is one that grows rapidly, requires significant capital to engender the growth, and then earns little or no money.

History is full of examples of businesses that attempted to grow too quickly and fizzled out leaving their owners with much less net worth than they started with. However, I’m just going to leave these 2 quotes on the table here for you to examine. You get to decide whether they appeal to your sensibilities.

4 Likes

Can you please give some examples from Indian stock markets and would be helpful if you can tell which metrics to look for to find out such companies. Any specific ratio ?

While I’ll refrain from offering tips, I’d advise reading the Berkshire Hathaway shareholder letters. There is far more knowledge and wisdom in those letters than I can explain here, I’m afraid. It should help you find good businesses.

I was not asking for tips or stock recommendations. I meant how can we filter out the companies which can employ large amounts of incremental capital at high returns. for ex. if we can look out for certain metrics (eg. ROE , ROCE , free cash flow etc). which can help in understanding such companies or any examples in Indian markets which have done this successfully (for analysis and learning purpose).

What does BH stand for?Sorry if it’s too common but I am not aware of.thanks anyways

Hi Rohit !

One of the many ways could be to look at average ROCE ,ROE & sales growth for last 5-10 years.

This I have found to be a reliable indicator of the company’s potential to deliver consistently. Hope it helps.

Thanks

I was watching Dhirendra Singh’s answers, he tactfully avoided giving clear answers to:

- What document(s) did Deloitte ask for which they delayed ?

- Didn’t the new auditor ask for those same document(s) ?

- If so how did they manage to provide those documents to the new auditor immediately who was appointed just within 1 day of Deloitte’s resignation ?

He didn’t answer anything clearly regarding these questions which can be literally answered in one or two words and just kept beating about the bush

New auditor did 5x sample check…

Given all documents whatever was asked for to Deloitte for last 8 years…

Audit continues even after signing…

I made the new auditor and investors sit in one room and left…

… bla bla bla.

1 Like

Motilal’s or SAIF’s assurance doesn’t mean anything, anyone who is already trapped would try to fake it. There were FII in Shilpi Cable’s too. None of Amit Mantri’s red flags were answered clearly.

2 Likes

This is one stock that still fascinates me (even after loosing a substantial amount). I want to share my below finding based on the most recent annual report.

- Company has a substantial Rs15cr under litigation with Income Tax Dept which is shown in contingent liabilities.

- Company has paid no taxes per cash flow from operation for the year. This could be a timing variance. Although the current tax was calculated as 17cr after MAT credit of 8cr and tax exemption of 16crs.

There are also the following red flags - Ever declining cash flows. Have never made a positive operating minus investing cash flow. CFO has also substantially reduced from the profit this year.

- Resignation of the auditor

- High accounts receivable of 15% of sales up from 10% of sales last year. I am not sure whether they are aggressively booking revenue just by shipping out more than customer orders and recognizing sale to intermediaries.

- No provision for doubtful debts which I think is very aggressive especially if 15% of sales are outstanding.

- Increasing inventory especially when the company is claiming that they simply cannot produce as much as the demand and doing such high capital spend like no tomorrow.

- Rs50 cr is shown as discounts. Aggressive discounting to push sales is also possible.

- The biggest expense is depreciation. 90% of depreciation is in relation to plant and equipment. They have used an effective life of 15 years for plant which gives a depreciation rate of 6.6% per year. However, even based on the end of year gross block of plant and machinery, depreciation rate for both 2017 and 2018 years works out to be around 14% which is more than twice the depreciation rate they have mentioned they use. This is a substantial Rs45cr additional depreciation for the year. What is the reason for this? Have they impaired the asset at end of year or used some kind of accelerated depreciation?

On the flip side, as WDV method is used, depreciation will keep reducing every year and if there are no substantial additions to P&E, this alone could give a Rs50cr boost to the bottom line easily a couple of years down the line.

8. They have listed manpasand snacks limited as a related party, which means manpasand brand is not exclusively owned by manpasand beverages and promoters have other interests with same brand name and also this reduces an area the company can diversify in the future.

A couple of positives are skin in the game promoters, low related party dealings, very reasonable promoter compensation and growth is high quality and seems sustainable for the medium term (ie purely based on increase on number of items sold).

At this instance, more negatives than positives and a high risk bet.

2 Likes