While FII exodus from India would be terrible, but it may not be like this…this is a case of total lost of trust company and not good management company facing exodus…bottomline if company is excellent it will find investors in some other country or institution…a country level event would mean country has lost trust…if that happens then in any way something very bad has happened any stock markets worry would be smaller than the main event…

We can be cautious when investing but we need to think positive for country level…if such bad event happens then will banks be able to pay FD interest and government PPF interest? Will our jobs remain…will our business, if any, survive…and house prices will crash as no buyers…therefore best we can do is focus on good bsuinesses and trust things will be better at country level

Elantas Beck India fell 83.4% from Apr 2012 to Sep 2013.

It used to have a MCap of 1700 Cr at that time, same as of now.

Its PE was ~ 55 before the fall (Dec 2011 earnings) and became ~ 14 (Dec 2012 earnings).

I am not aware of the reason behind that fall, but EPS fell from 30.49 to 19.86 from Dec 2011 to 2012. It was 40.11 on Dec 2010.

https://www.screener.in/company/500123/

This is old ratings of Manpasand though not that old… But Crisil also said 4.5% Market share which is close to what actually people are expecting…

At 4.5% Market share of total 7-8K crore mango drink market …for FY17 … I don’t feel that revenues are shown more or hyped…

What about this rating?

Believe it or not “Every letter needs to be signed by a biological person” doesn’t happen anymore in more advanced countries. Times are changing.

The answer lies in first two lines of the document itself.

CRISIL has withdrawn its rating on the proposed long-term bank facility of Manpasand Beverages Limited (MBL) at the company’s request. The company has confirmed that it has not availed any debt against the facility.

Manpasand did not need any credit against the rating. So, they asked Crisil to withdraw it.

Withdrawing rating is also a possible euphemism for future credit downgrades. Credit rating agency regularly communicates with company and sometimes lets it know that future actions may be negative. Company can then decide it’s not worth having a credit rating. Credit rating agency is absolved of all responsibility once a rating has been withdrawn.

In short, about Vakrangee(1) and Manpasand(2), Latest Holdings Status

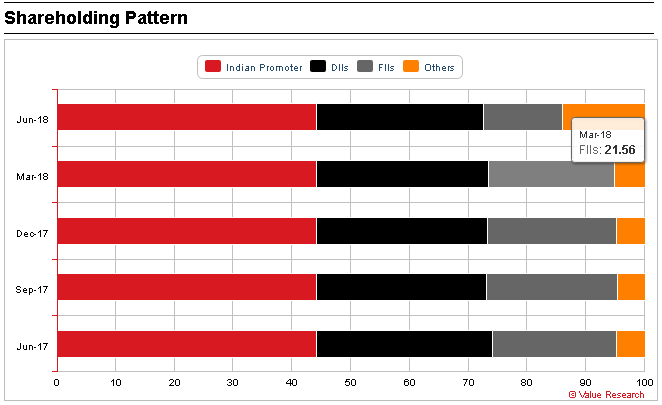

(1) Retail investors more than doubled their stake in Vakrangee to 10.55 per cent at the end of June quarter from 4.63 per cent and 4.16 per cent at the end of March and December quarters, respectively.

Foreign portfolio investors (FPI) also reduced stake in Vakrangee to 20.55 per cent from 29.12 per cent at the end of March.

Mutual funds held just 42,051 shares of Vakrangee as of June 30 against nearly 5 lakh at the end of December quarter.

(2) Retail investors’ with share capital of up to Rs 2 lakh hiked their stake to 6.19 per cent during the quarter gone by from 2.49 per cent at the end of previous quarter.

Foreign portfolio investors reduced their holding to 13.35 per cent from 21.56 per cent.

Mutual funds reduced their holdings to 10.83 per cent from 11.60 per cent at the end of previous quarter.

To summarize, for Manpasand, FPIs reduced stake by 30%, and MFs reduced stake by 6.5%. Retail absorbed these stakes. MF reduction is negligible, given 60% reduction in price. Reaction seems relaxed, or at least waiting rather than panic selling.

Discl: 2% stake in portfolio @ average price of 150, invested since past week.

Went to DMart (in Bangalore) and saw they have come out with their own mango drink - Mango Merry. Packaging is very similar to Mango Sip.

In many forums and posts about Manpasand, we hear that smart money is dumping and retail is absorbing it stupidly. I have just one question. What sorts of smart money are they who buy at Rs 450-500 and sell at Rs 150?

They are smart by saving whatever is left… Even if they had invested in IPO , they are not loosing anything except opportunity cost from 2015-18

For retail it becomes Hero-Zero game… We know everything what has happened and still we are emotional…we invest without any proof justifying ourselves that no…we can see so many shops selling it … This has to be true brand…

Well…Well…Well… Retailers can win this…by luck but FPI is losing nothing again…they find some other share …

Because domestic MFs knows our companies better than FPIs and if they don’t sell it this quarter then… Manpasand Beverages will stabilize and lack supply…

Its a question which time only can answer, whether retail is walking into a trap or FPIs over-reacted. I mean Delloite has signed their balance sheet for 7 years without even adverse qualification. So how probable is it that the promoter who was honest for 7 years turned a crook in the 8th? Its often compared with Vakrangee but their business models are vastly different. I tried hard to find out how Vakrangee can make so much money but could not find a plausible explanation. In Manpasand’s case, one can see product visibility in trains and also in retail stores.

In India, far more listed businesses have gone down under due to leverage than due to corporate governance.

Disc. Invested a bit around Rs 135, less than 0.5% of PF.

Word of caution: I’m pretty new at analyzing businesses, but trying to put

forth my analysis.

Let’s start with these numbers:

Part 1: Piotroski F Score breakdown

| Piotroski Score | 2 |

|---|---|

| Positive ROA | Y |

| Positive CFROA | N |

| Higher ROA yoy | N |

| CFROA > ROA | N |

| Lower Leverage yoy | N |

| Higher Current Ratio yoy | N |

| Less Shares Outstanding yoy | N* |

| Higher Gross Margin yoy | Y |

| Higher Asset Turnover yoy | N |

2-3 is a bad or low score. The Piotroski score highlights Part 2 and Part 3

as well, but just wanted to see where else this business isn’t doing well.

According to Professor Joseph D Piotroski, such a score makes it a great

shorting candidate.

* Yet to account for any additional share dilution.

Part 2: Declining ROE, ROIC, and ROA

| Year | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|

| ROIC | 16.44 | 16.45 | 11.27 | 10.22 | 9.97 |

| ROA | 10.47 | 10.96 | 9.99 | 7.67 | 7.52 |

| RoE | 21.43 | 20.48 | 12.65 | 8.28 | 8.33 |

| Net margin | 6.99 | 8.36 | 9.89 | 10.36 | 10.54 |

| FCF margin | -4.23 | -29.61 | -29.57 | -23.02 | – |

| Asset Turnover | 1.50 | 1.31 | 1.01 | 0.74 | 0.71 |

I’m not quite sure, but wouldn’t you be spending capital

on assets if your turnover on assets was going up (you’re already

using your existing assets exceedingly well) and you couldn’t

meet capacity with existing fixed assets? Please correct me if I’m

thinking incorrectly. Would appreciate input.

To me, what the management is saying and what the numbers are

indicating are at crossings. I know they’re spending on expansion.

However, I’d also like to bring to our attention what returns

the shareholders are drawing from their investment so far.

Can someone please explain why the RoE is tanking?

Their net margin is crawling up, but it doesn’t tell me that

this business has much pricing power over the customer

(other established non-alcoholic beverage manufacturers

could easily lower their margins and compete with this business

on price). Businesses that exhibit high pricing power don’t have

such low margins. Let us assume for a moment that Manpasand

raises pricing on its products, what stops consumers from

choosing alternative equally well-tasting products?

Part 3: Historical accrual buildup

| Year | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|

| Sloan Ratio % | 16.81 | 38.66 | 42.58 | 44.61 | 7.01 |

| Accounts Receivable | 477.45 | 593.35 | 677.50 | 751.93 | 1,392.71 |

| Change In Receivables | -161.96 | -123.73 | -119.68 | -74.27 | — |

The first line in that table is a big red flag to me

although it appears to have been alleviated recently.

Not sure, why it isn’t to others.

Part 4: Beneish M Score

While this is only a probabilistic guess, the Beneish M score is popular

for red flagging Enron before its collapse. The median

Beneish M score for this business indicates that it is an earnings manipulator.

Median score is -0.34. An M-Score of greater than -2.22 signals that

the company is likely an accounting manipulator.

Part 5: Dividend payment when the business needs cash

Assuming the business is in the initial growth phases of

expansion, every bit of retained cash should account towards

that specific goal to my mind. Appeasing shareholders by

using shareholders equity as a source of credit and then paying

out a dividend does not make prudent sense to me when it

comes to capital allocation. It’s like borrowing from one credit card

to pay for the minimum payment on another—it’s just revolving credit.

Why pay a dividend when the business itself needs to raise additional

capital, which it has been doing for roughly 5 years now?

Shouldn’t a business retain cash if it thinks it can deploy it to

better use for its shareholders than the shareholder herself could?

I find this sort of capital allocation rather puzzling.

Summary

In summary, the business doesn’t appear to have any pricing power,

it has lowering asset turnover, there’s reported growth in

the earnings statements and future promises, the capital expenditure

is powered by diluting shareholders equity to use it as a source of capital

instead of its own cash-generation ability, and it is paying out dividends

when it needs the cash for its own use. All this while the stock price had been

flying pretty high and is currently grounded very likely because

some investors have realized declining net worth. I don’t think

the FPIs are blind to all this and do believe that they may be making

wiser decisions, I’m afraid.

I’m still not sure why this business is worth buying so far and

would appreciate any insight that I might be missing. Looking forward

to your inputs.

Thank you!

I was reading on the net on Sloan ratio and it says if the ratio is between -10% and 10%, the company is in safe zone.can you explain a bit about it and your assessment to of Sloan ratio of the company whether it’s good or bad and how?

Direndra Singh’s first interview after auditor resignation.

I too heard the interview.its obvious that the management is provided with questions and they come prepared with answers which seem reassuring the share holders.Request experienced members to comment on the interview, body language

Here’s my understanding:

The earnings statement (PNL) highlights the net effect

of claims/rights to collection of payment (revenues) and

obligations to payment (expenses). Essentially, it

reports what the business promises to turn into

or pay out in the form of cash.

When inventory is turned into accounts receivable,

claims on future cash build up/buffer—this is called accrual.

The cash flow statement reflects actual cash inflow

and outflow—it’s where the accrual is realized. Usually,

for a rather steady business, there is a certain lag

(in some excellent cases, cash arrives in the coffers

“prepaid”) between accruals and cash flow, and is

not a problem. The Sloan ratio attempts to capture this lag

and is an indicator of the quality of earnings.

This becomes an indicator of a deeper

problem when several successive quarters/years pass

by with accruals building up and the cash doesn’t show

up on the balance sheet. In the case

of Manpasand Beverages, I believe, the majority of that

cash has gone toward setting up new plants. However,

such capital expenditure should also be justifiable by

higher asset turnover, which has been declining.

I’m not certain it will pay off.

My Assessment

While it is important to keep reporting growing

net earnings (net income, profit, bottom line,

whatever else you want to call it), it is also important

for the operating/free cash flow to match what is

being promised in the form of those earnings. If

this doesn’t happen for 5 years, it is likely some

types of investor will worry and sell their stakes in

the business off. I believe that has happened here.

Some people no longer believe

that this business can turn those promises into cash

and thereafter increase the net worth of the

shareholders. Shareholder earnings are drawn

from the free cash flow of a business, and are

different from reported net earnings.

Equity dilution has the same effect as inflation.

A stock certificate is a business’s right to print

money. Abusing that power reduces the value

of each stock certificate and therefore the net

worth of its stock certificate holder.

The business has diluted shareholder equity

to raise even more capital.

While the management doesn’t realize this,

the sell off reflects all of this, and the current

discounted price asked for by the bidders

indicates that they want to pay below the

rate of return offered by an index fund plus

some risk premium for investing in a business

that is yielding progressively lower returns

on equity (8.33% now).

I think of Manpasand Beverages as a

turnaround candidate not really a

wonderful business. It is in underpriced

territory because it hasn’t exhibited stellar

capital allocation—the auditor resignation

was likely just a trigger for the sell off.

Justifying aggressive expansion is akin to

justifying speeding on the freeway. One slip

and you’ll become roadkill. Fix these problems

and the business should recover. Do you see

that happening? I’d rather prefer more conservative

financing and capital allocation.

Additional Reading

You can read more about the Sloan ratio here.

Question: Have you tasted MangoSip

and did you like it? Do you think

you would prefer it over Maaza or Slice?

About Sloan ratio and FPIs etc.,

Q: What happened in past 2-3 months, to drastically change the analysis by FPIs of the overall business?

A: Nothing, except the news about the auditor.

About the taste, personally I drink Real mango but only after diluting it with more than 30% water ![]() as I find most mango juices too sweet and strong flavored. Which is what Manpasand also does

as I find most mango juices too sweet and strong flavored. Which is what Manpasand also does ![]() and makes money in the process

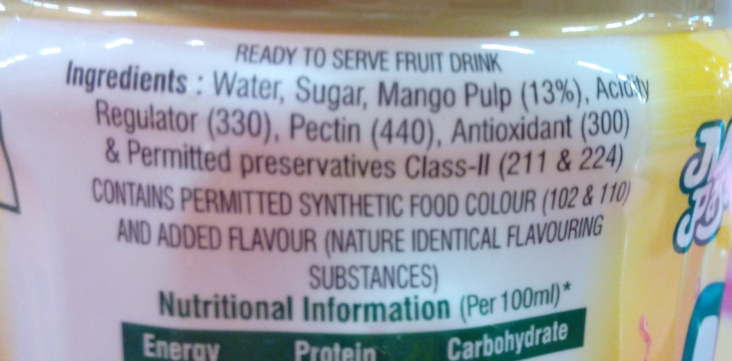

and makes money in the process ![]() Check the mango pulp content, exactly half of Real.

Check the mango pulp content, exactly half of Real.

I think MangoSip has good supply in (govt, rail) catering tenders, being on the cheaper side. Also more for the “aam aadmi” ![]()

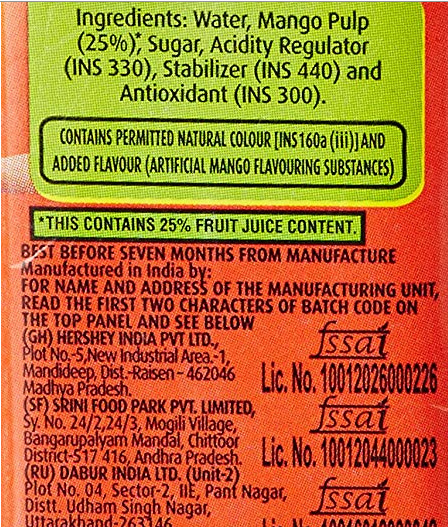

DABUR

MANPASAND

Discl: 2% stake in portfolio @ average price of 150, invested since July 06, 2018.