Sure! @rupaniamit - here you go! M/S. Mangalam Organics Ltd vs Union Of India on 24 April, 2017

Also, to the team researching here - I have compiled some studies on this stock into a pdf. Sharing it below

Mangalam Organics - Study.pdf (2.0 MB)

Sure! @rupaniamit - here you go! M/S. Mangalam Organics Ltd vs Union Of India on 24 April, 2017

Also, to the team researching here - I have compiled some studies on this stock into a pdf. Sharing it below

Mangalam Organics - Study.pdf (2.0 MB)

thank you for detail research note

Great work Akshat! The Co.'s appeal in the Supreme court clearly establishes the fact that it imports Gum Resin & not Gum Turpentine. Gum Turpentine is in fact produced in house, unlike in the case of Kanchi, which imports Gum Turpentine. This establishes why margins in Mangalam are higher. Being backward integrated, it creates value addition along the entire manufacturing process. Kanchi, on the other hand is more of a converter of Gum Terpentine into Camphor.

Even though the Supreme court judgement went against the Co., it did not affect it as the excise duty had already been paid & factored in & the Co. was merely seeking a refund, which if it succeeded, would have resulted in a one time gain.

This thread has seen some amazing scuttle butt & has gone a long way in unraveling the entire camphor puzzle! Great job guys! May the tribe grow!!

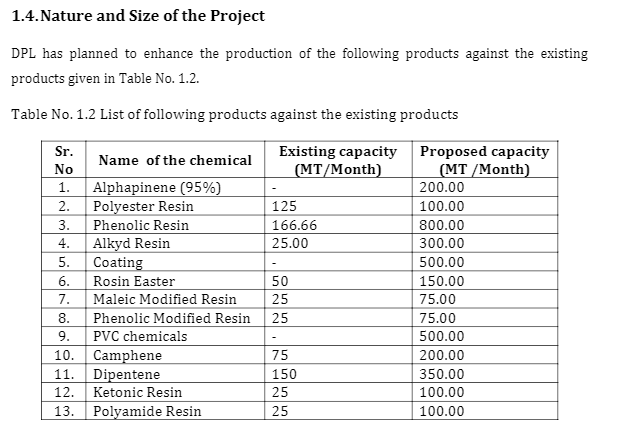

This is a document for proposed expansion by Mangalam (erstwhile Dujodwala Products Ltd.) from 2014.

http://docplayer.net/62245057-For-proposed-expansion-of-organic-chemical-manufacturing-plant.html

They had applied for expansion to enchance production of the above chemicals which includes Alphapinene manufactured by distillation of turpentine oil and not Oleoresin.

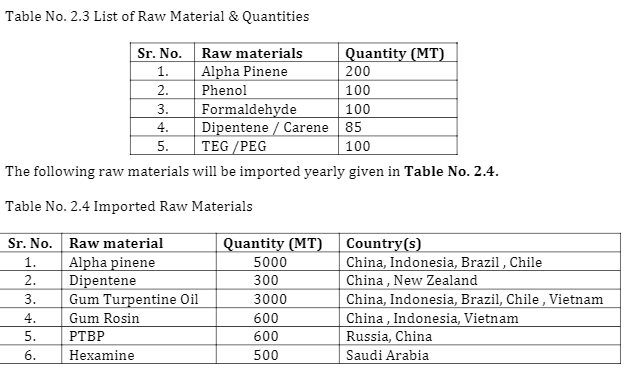

The following raw materials were to be imported for proposed expansion. I didnot find Oleoresin in this document. however application for imports of gum turpentine oil and gum rosin is made and in significant quantity.

I am confused whether the company has full capacity to manufacture gum turpentine or after expansion it has to import some to manufacture value added products.

I think the company applied for product mix change after getting approval for expansion.

Maybe i am wrong.

Regards

This was the missing link @akshat96jain. Looks like my earlier speculation wasn’t too far off. We still don’t know how much backward integration they have in place. I doubt if they will be 100% backward integrated.

I didn’t know this. Happened to go to a d-mart recently and noticed that their in-house brand Kaveri Camphor is actually manufactured and packaged by Mangalam Organics. I should have guessed going by how similar the Mangalam branded box and Kaveri box looked. This is the only brand of Camphor they were selling in this store and they were adequately stocked (must have been over 500 of these) and the product seemed to be fast-moving, going by the inputs from the sales clerk. I couldn’t find any CamPure or Cam+ products though.

Looks like they are establishing themselves in the modern trade and e-commerce channels. Not sure how they are doing in the retail general trade (unorganised retail). There is definitely significant value-add in retail sales vs wholesale and it could cushion the impact of RM fluctuations as well in the future.

The Promoters investing 1.87 crs buying 36591 shares at an average buying price of Rs. 511 is significant & meaningful, in that they see value at buying at this price. This will go a long way in helping build further conviction in the story, if at all it was needed!

MangalamOrganics Very strong results expected with Promoters buying stock worth ~2Cr directly from market “just few days before closure of trading window for results that takes place from tomorrow”

Looking at Friday Volume won’t be surprised if they would have bought more.

Status quo maintained for April.

Source: https://www.berjeinc.com/2019/04/

In the long run, if sufficient amount of the topline contribution comes from retail Camphor products, this shouldn’t matter too much.

Collected some numbers from Amazon:

| Product | Reviews | Price | Revenues |

|---|---|---|---|

| Camphor Tablets | 157 | 735 | 115395 |

| Camphor Sticks | 105 | 368 | 38640 |

| Camphor Tablets | 75 | 850 | 63750 |

| Camphor Cones | 438 | 470 | 205860 |

| Cam+ Pain Relief | 1 | 220 | 220 |

| CamPure Purifier | 39 | 255 | 9945 |

| Cam+ Sniff | 5 | 157 | 785 |

| Cam+ Roll | 6 | 240 | 1440 |

| Amazon Revenues | 436035 |

These are the revenues only via Amazon and from people who’ve only written the reviews.

Assuming 2% leave feedback, the revenues from Amazon till date (over past two years but not single FY) would be around 436025 * 50 ~ 2.2 crores.

This is not huge as compared to total revenues of 240 crores in FY18 and 374 crores in TTM.

However there is potential to grow.

Any one has any data on the offline segment?

I personally doubt if the revenues on that front are huge as it takes time for the company to setup a distribution network and expand it as they started this Retail business just two years ago.

Disclosure: Invested. Not a buy / sell recommendation.

I think 2% is too high even for consumer electronics. Lot of things drive this percentage from demographic (educated vs illiterate, young vs old etc), satisfaction (unhappy customers are more likely to leave a review), type of business (commodity business should have lesser feedback), repeat business (doubt if anyone will leave review on subsequent purchases), fluency of customer, age of product (older and established products will have less reviews) and so on. Base rates shrink drastically with overlap in the above. My working percentage for a business like this is 0.1%.

I believe Mangalam’s retail sales could be about 10% of topline at this point, but contributing about 20% of the bottomline roughly. I think it should continue to grow as they find more channels for distribution. In terms of valuation as well, I try to treat this part of earnings at a higher valuation than the wholesale commodity business, as this could be sticky with protected margins.

Just noticed that they have launched 4 new retail products

Hand Wash - https://www.amazon.in/Mangalam-Cam-Camphor-Handwash-250ml/dp/B07QFDT28P?ref_=bl_dp_s_web_15486913031

Camphor Oil - https://www.amazon.in/Mangalam-Cam-Camphor-Oil-Relieves/dp/B07QCN3N5J?ref_=bl_dp_s_web_15486913031

Hand Sanitiser - https://www.amazon.in/Mangalam-Cam-Camphor-Hand-Sanitizer/dp/B07QFDSC43?ref_=bl_dp_s_web_15486913031

Camphor Balm - https://www.amazon.in/Mangalam-Cam-Sniff-Ayurvedic-Preparation/dp/B073W8LPBJ?ref_=bl_dp_s_web_15486913031

Results on 11th. The wording mentions “recommendation of dividend” as well for consideration, which is good (last two years’ wording doesn’t have it). I think a PAT of about 20+ Cr. is possible, going by realisations. Volume-wise, I think this business is a bit seasonal and Q3 that went by was the best quarter.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=fbd1b1dc-6dcd-44cd-8010-28c7f5b2e692

If the management wants the company to be taken seriously by the market in terms of valuation, they must share a decent portion of profits with shareholders via buybacks/dividend as they did last year (even a 20 Cr dividend payout will send a strong signal, as it will be roughly 25% payout and a strong 4.5% yield at current valuations) and perhaps pay off a bit of the WC debt in the BS and more importantly, share more details about the business at least on a quarterly basis.

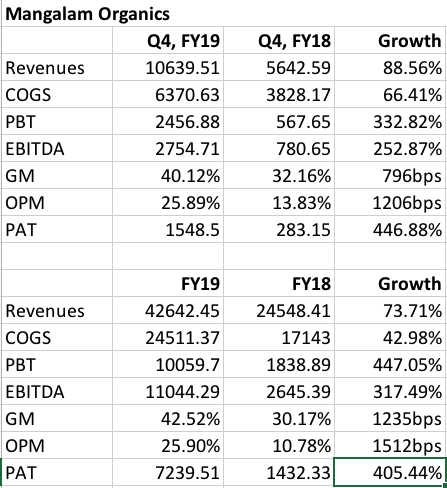

Mangalam Organics Q4 and Final year results declared. Dividend of Re 1 declared.

| Financials | Q4 FY18-19 | Q3 FY18-19 | % Change |

|---|---|---|---|

| Total Income | ₹ 106.39 crs | ₹ 121.69 crs | Down Tick -12.57% |

| Net Profit | ₹ 15.48 crs | ₹ 26.26 crs | Down Tick -41.05% |

| EPS | ₹ 18.08 | ₹ 30.67 | Down Tick -41.05% |

| Financials | Q4 FY18-19 | Q4 FY17-18 | % Change |

|---|---|---|---|

| Total Income | ₹ 106.39 crs | ₹ 56.91 crs | Up Tick 86.94% |

| Net Profit | ₹ 15.48 crs | ₹ 2.83 crs | Up Tick 447% |

| EPS | ₹ 18.08 | ₹ 3.13 | Up Tick 477.64% |

| Financials | 12 months FY18-19 | 12 months FY17-18 | % Change |

|---|---|---|---|

| Total Income | ₹ 426.42 crs | ₹ 245.48 crs | Up Tick 73.71% |

| Net Profit | ₹ 72.39 crs | ₹ 14.32 crs | Up Tick 405.52% |

| EPS | ₹ 84.05 | ₹15.82 | Up Tick 431.29% |

Looks like a strong set of results. Interested to hear inputs from other boarders.

Invested.

Pretty good numbers on expected lines and YoY growth is quite good in terms of sales, gross margins, ebitda and also PAT. QoQ numbers are perhaps not comparable as I guessed in my previous post due to bulk of festival demand being in Q3. Overall year as well, the performance is quite good by all metrics.

A bit disappointed by the dividend declared, so I looked at the BS to see what had happened. It looks like change in working capital is 50 Cr and about 22 Cr has gone into fixed assets (the expansion) - so that’s where a bulk of the earnings have gone.

The transformation from wholesale to retail is changing the working capital requirements of the company. It is going to reduce the cyclicality of the business at the cost of higher investments into working capital (inventory mainly). The return ratios and margins will moderate going forward but the earnings could be more sustainable. Retail though is tough business so working capital will need close monitoring going forward. Any P/E re-rating can only happen if market is aware of the proportion of retail contribution to the numbers (Current P/E post numbers has dropped to a shade under 7). Maybe the AR will shed some light on these things.

How do u see the sudden decrease in employee expenses and the increase the raw material prices which is against the notion u had about being backward integrated. Has the DRT deal started showing in the top line. And whether the capex is happening and what is the split of income from RETAIL segment. As u said clarity will come from ANNUAL REPORT

QoQ, revenue growth is almost doubled. Right!

Last 5 quarters employee expenses go like this (oldest first) - 3.6 Cr, 3.7 Cr, 4.5 Cr, 8.5 Cr, 5.4 Cr. So my guess would be that they ran more shifts in Q3 to keep up with the seasonal spike in demand, or paid out a bonus or maybe the payouts are lumpy or they could have hired someone to develop the retail products. There is absolutely no way to tell. We can only guess. We don’t even know how they are coming up with products, who is developing them and manufacturing them etc. I believe those contracting services costs will be part of this.

As for backward integration, I doubt if they will be 100% backward integrated and if they are not, the margins are in-line (or better) with rise in GT prices in Q4 (procurements for Q3 could have happened in Q2). GM of the quarter are roughly about the same as GM for the year, so as long as they maintain it around 40%, with OPM around 25%, it should be ok I guess. Q1 and Q2 GM were around 34%, so 40% GM when GT prices were at their peak is not bad.

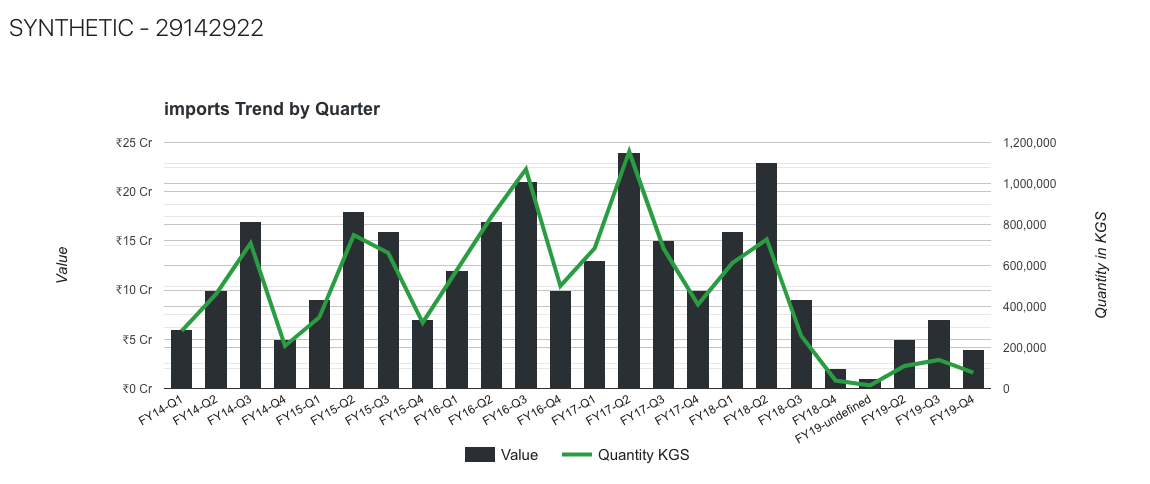

I looked at Camphor imports of last 5 years to ascertain seasonality. It is beautifully illustrated in this chart where Q4 of every year had the lowest volume and value of imports.

Interesting thing is Q4 is less than even 50% of Q3 consistently for last 5 years

FY14 Q3 vs Q4 - 17 Cr vs 5 Cr

FY15 Q3 vs Q4 - 16 Cr vs 7 Cr

FY16 Q3 vs Q4 - 21 Cr vs 10 Cr

FY17 Q3 vs Q4 - 15 Cr vs 10 Cr

FY18 Q3 vs Q4 - 9 Cr vs 2 Cr

Going by this sort of variation between Q3 and Q4 (possibly over 50% drop in volume of consumption), the drop in topline of 12% (QoQ vs Q3) shows that the performance has actually been stellar. This was something I noticed in Bata as well in Q2 and relative outperformance in a seasonally weak quarter usually indicates strength (Bata confirmed that in Q3). Hoping it’s the same stuff here.

sir any idea mangalam current camphor mfg. capacity ? and after expansion capacity?