Page No. 13 of AR-2017-18 reads: “We foresee large volumes, revenue and strong profitability from this in the years to come”.

Though it talks only about Terpene Phenolic Resin, the product descriptions cited in the above post also relate to other two variants of Phenolic Resin, that is - DRT-4001/4002/4015/4007 and DRT - 4003/4004.

I think Kanchi Karpooram is a better company as its Return Ratio was higher even before this Camphor price rise year back. Mangalam Organics has bought back shares which resulted in better RoE. BuyBack has raised promoters stake by 2.69%. The buyback price was Rs 230. Promoters are sitting at good gain.

Kanchi Karpooram looked better in Return Ratio over long time but don’t know why its cash generation was so poor. Mangalam Organics Cash generation is comparatively better in recent years.

Few pointed about Employee cost could be due to higher pay by management but this higher employee cost was in June 2017 as well (7%). I see Kanchi Karpooram’s Employee cost has reduced in June and Sept quarter. It should be for Mangalam Org as well as I do not think higher sales directly translate to more employee. Same employee generally work to produce more to some extent. So, in this case, may be higher management has taken a raise!

I see both companies are in same business and getting same benefits past year due to Camphor price rise. Only point, is alliance with DRT, France by Mangalam Organics. I did not checked if any new development Kanchi has added.

Investors should remain cautious of price of Alpha-pine and other input materials. Alliance for Resins export with DRT can take time and market won’t wait for correction when raw input price rise and/or Camphor import from China rise to India.

I think @phreakv6 can help us here. He has tracked price of Raw material month wise. According to him, Menthol price is related to this !

In Related Party Transactions, 5 Cr is transacted for Rent deposit to Dujodwala Resins & Terpenes Ltd. It is same amount in 2017 and 2018. Is this transaction happen every year or once it has happened but company need to mention every year ? Find at on Annual Report, page # 67.

I am not sure why that cash flow means all is not well. Kanchi Karpooram is undergoing a major capacity expansion. Does it not explain where most of the profit last year went, as also the warrants issue?

Camphor price - Fall in price can turn the whole story:

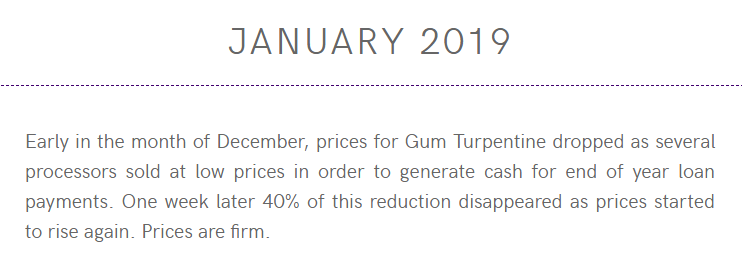

Called up a local wholesale shop in Bangalore and interacted with that guy for a while. He seems confident that the prices would sustain and don’t see prices falling back to previous levels of 300 per kg. That guy was quoting 1000 per kg.

Also have noticed that 50g boxes of camphor Puja tablets from local non-branded players are selling for 60rs in the retail market.

Production capacity by players around - Supply can outstrip demand:

Kanchi Karpooram seems to be expanding aggressively.

Have seen in some VP posts that Mangalam is also expanding but not sure if if true as I don’t know its official source yet.

No data on the expansion plans of unlisted players

Oil price - Checking if it increased:

With oil price falling back to its previous low levels, adhesive manufacturers shouldn’t shift back to Gum Rosin helping Gum Turpentine prices to remain high.

Factories in China - Worried if they start dumping in India:

Apparently, the closure of factories has slowed down in China in 2018. However, not sure if the Govt would allow the factory owners to reopen them as they still seem to have pollution problems.

Increase in production by the factories seems to be the only red alert to me.

Will keep monitoring these variables. Please add if there are more monitor-ables.

Breakup of revenues in FMCG B2C business vs. Commoditized B2B business should help us take either comfort or worry.

Disclosure: Holding Mangalam at 5% of portfolio. Not a buy / sell recommendation. Noob investor.

The stock was quoting at lower circuit this morning, so I called up a camphor dealer in Chennai & another in Mumbai. Both confirmed that the prices were ruling steady at around 1000-1100 per kg & for the last three months there has been no price correction.

@RajeevJ - This stock is a classic example of inefficiency in the markets, especially in microcaps. This fall from 576 to 379 is not the first 30% fall it has seen either - It has done it thrice already in the last 6 months. 30% down and up has been the routine here. I blame the management for this as they have been completely opaque about what’s going on. Unlike managements that dispatch optimistic messages often (like say sanwaria or sadhana), there is nothing here other than the bare minimal, mandated disclosures. In periods of uncertainty, the herd always looks for social proof. If it falls down sell and when its going up, rush to buy. Post-hoc rationalisation can justify any valuation. Today’s fall I think is because both Kanchi and Mangalam have been moving in lock-step for the last few weeks and issues in Kanchi’s management had a rub-off today here as well (They postponed the results by a day yesterday as the auditors required some additional information)

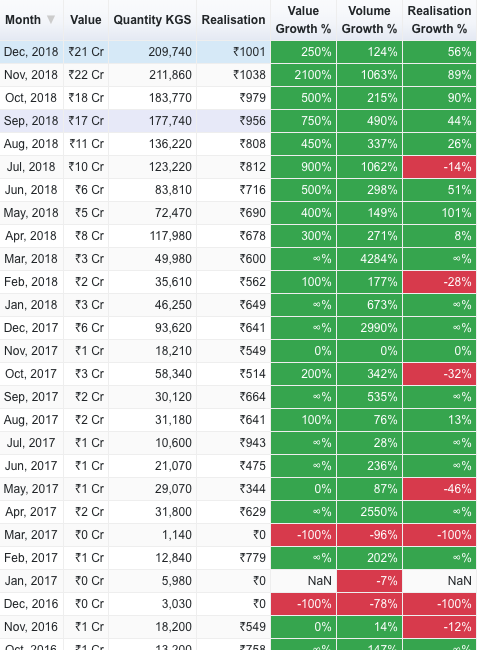

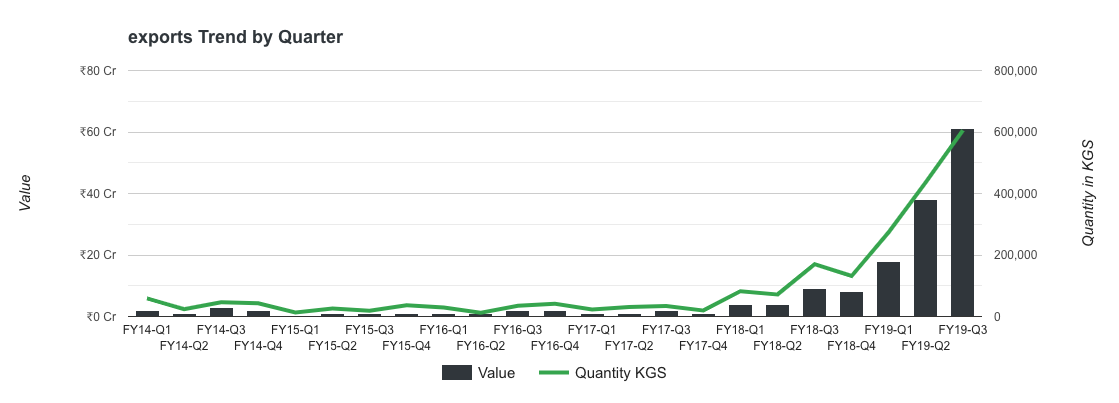

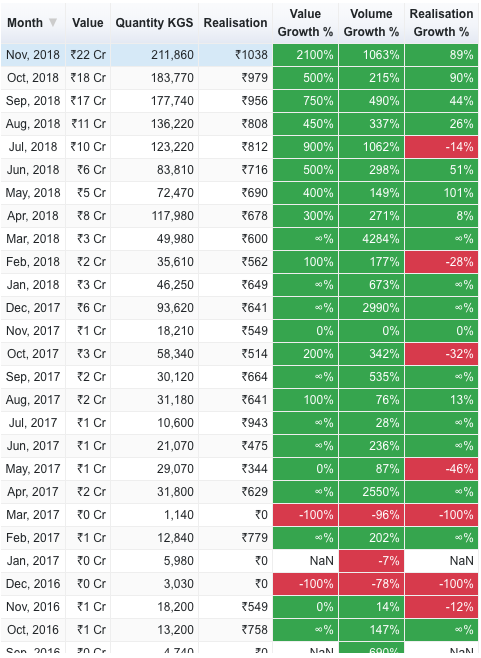

As for fundamentals, in addition to whatever I have dug up in the past, I also noticed that we are now a net exporter of Camphor since early last year and the same has picked up steam drastically in the last quarter. It looks like we are exporting around 600 MT of Camphor as of Q3, FY19. Half of this export is to China. That should be the reason why both Kanchi and Mangalam have rushed to expand capacity.

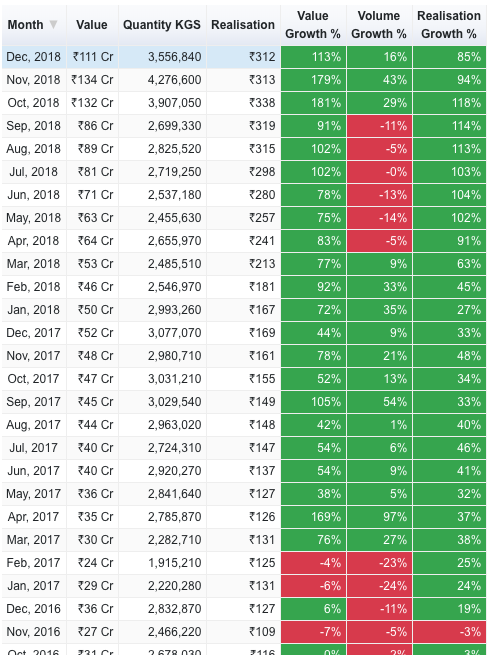

Camphor Imports - Notice the 400 MT/month rates in mid FY17 to 45 MT/month levels now.

I see that wholesale rates are around 1000/kg as you had pointed out and the Mangalam camphor retail on Amazon is still about Rs.1500-1800/kg depending on the packaging. There is no change there. Third-party sources still point to firm prices of Gum Turpentine oil. I also looked up a bit of Akshay Dujodwala and what I found is encouraging. It looks like he is the mind behind CamPure and Cam+ brands and there are sources online where you can find that he has got himself involved in things like branding and going by the brief he had provided the designer and cost-consciousness of the approach, showed the ability to think out-of-the-box. I also see the Dujodwalas are a routine presence in Pine chemical conferences in China and Brazil. They do seem keen to expand outside of wholesale Camphor into retail and also other terpene chemicals.

Market will find it hard to believe the sustainability of the numbers or to trust the management until we see what they intend to do with the 100 odd Cr they should be generating this year. Along with the beating smallcaps are taking and the company of Kanchi Karpooram which it is moving in lock-step with, I doubt if market will reward this company with runaway valuations. I was expecting 8 P/E before Q4 results but even that looks doubtful at this point.

Disc: Invested/Trading

Update: As I finished posting Kanchi’s results came out.

Topline growth of 54% and bottomline growth of 64%. Their gross margins are around 25% which is nowhere in comparison with Mangalam’s recent quarter gross margins of 58%. Mangalam’s GMs have been steadily improving in the recent quarters so either the product mix or in-house production of important RM or the retail play is distinguishing Mangalam from Kanchi Karpooram as I have speculated before. The market however refuses to see that and we must respect that. Until the management improves transparency and shows what it intends to do with the cash from the exceptional gains in the year, we will be subjected to the vagaries of the market.

One of the reasons for the fall probably was in sync with Kanchi Karpooram. In case of Kanchi the results were due yesterday and had to be postponed to today.as independent directors had sought further financial information.

Now this kind of announcement these days sent shivers down most investors spine. So Kanchi went down and maybe fearful investors invested in Mangalam organics also panicked and dumped.

These days inspite of very good results there is hardly any positive movement in stock prices and if it happens too, it fizzles out within a couple of trading sessions.

For investors who know what to buy and who have money to buy its a happy state. Cheap keeps getting cheaper. Just look at what happens in most paper stocks.

@phreakv6 - I agree with you that when mgt.'s decide to go into their shell, it creates a breeding ground for operators to play around. As is always the case, the retail guys are the target. It’s an open secret that Retail investors by & large don’t buy on lower circuits nor sell on upper circuits. This is exploited to the hilt by the operators. Again, this is possible only in small cap stocks, where few if any, larger investors are present as even a single big investor can spoil the operators game by coming in the way. The larger players, on their part are reluctant as there is not enough info available about the Co. So it becomes a bit of a vicious circle!

The Mangalam mgt. to their credit was very forth coming at the AGM, but as the AGM itself was held at the plant, not too many shareholders were present. Hopefully there will be more of us present next year. I also believe that the Mangalam mgt. is smart & will at an appropriate time decide to become investor friendly! That’s after they have taken their shareholding higher. The last buyback took it to 49%. I will not be surprised to see this at higher levels in a year from now!

We need to understand if growth in Camphor exports is sustainable. I suspect the exported camphor is going into the pharma industry. If true, then it’s a structural story & certainly a sustainable one. It is known that perhaps its only in India that camphor is used for religious purposes. Can we work on this aspect to better understand the situation?

There are probably not many applications of camphor in pharma as such, might be few of the derivatives of camphor are used in pharma. India is a major manufacturer of Pharma APIs, and we see a rise in camphor export. So this probability of rising in pharma application is less. I see camphor uses more in making speciality chemicals for various applications.

The major risk with camphor companies I see is the shift of manufacturing to countries like Indonesia from where this pine wood raw material is imported.

Thanks for the detailed updates. But there is no disclosure by Mangalam about capacity expansion. Do you have any source of information where its mentioned this expansion?

This company hasn’t disclosed any details to the exchange, from capacity expansion, retail foray, retail tieups with dmart, spencer, reliance retail (With d-mart http://dmart.in/camphor---kapur for eg.), the social media brand building (Mangalam Camphor | Mumbai, http://campure.in) using influencers (check videos for camphor cone on youtube using influencers) or ad spends (sponsored keywords on google, amazon’s choice product and sponsored ads on amazon), growth in modern trade and so on.

There are no concalls and ARs are bland with bare minimum info (compare that with AR of this company that possibly doesn’t even have real products). Pretty much every piece of information has to be dug up from 3rd party sources but there is quite a bit of information in the public domain if you dig in govt. websites, e-commerce websites, wholesalers like indiamart, retail shops, linkedin where you can see the sort of talent they look to have hired post 2016, from a FMCG manager, engineers from sun pharma/lupin and so on (and contrast it with their competitor in this space).

Ideally lot of this information should be available via company dispatches but the management probably has other priorities.

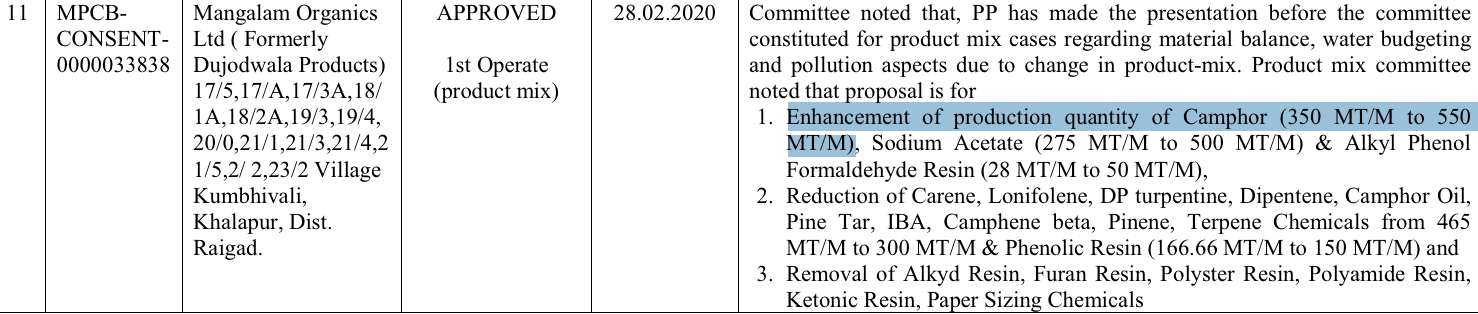

Thank you for this source of information. This reveals that the company is changing the product mix while keeping overall production constant if I have understood correctly.

There is a lot of developments on FMCG front but the company should have given disclosure for production strategy as there are many side products forms during the camphor manufacturing. The company will hopefully scale up high-value products instead of me too.

Hi, when you enter any stock with a stop loss strictly follow it (no matter what) if you enter with SIP mindset, follow that strictly. Mixing up can slump you further. I ignored stoploss in few cases and learnt the hard way.

Cheap keeps getting cheaper. Just look at what happens in most paper stocks.

Cheap keeps getting cheaper. Just look at what happens in most paper stocks.

if you enter with SIP mindset, follow that strictly. Mixing up can slump you further. I ignored stoploss in few cases and learnt the hard way.

if you enter with SIP mindset, follow that strictly. Mixing up can slump you further. I ignored stoploss in few cases and learnt the hard way.