NIM 15%’ Loan yield 24% is not sustainable in long term. Even micro finance yield has come down to below 20%. To scale up and create sustainable model , yield and NIM will have to reduce. We have to see what will be ROE in that case if yield is below 20%. I guess this is the reason of under valuation.

Disclosure- Invested with 3% exposure from lower levels. An undervalued opportunistic play for me.

1 Like

i remember in the con-call they having said:

for home loan businesses due to nature of skill/work, they have all independent office set up and are not using same infra of that of Manappuram Gold.

Not sure how much moderation can happen, but could be slight moderation if any. At the same time, note that gold loans are short term loans(3-9 months) given at 24% and there may be not be much moderation needed here…(Remember we pay 36% on credit card cash loans from banks still for short duration loans!) Further, the company has high CAR(22%) and very low gearing(3-4 times) and also high cost of funds(9.9%) currently - so it has these additional levers to further improve the margins or atleast sustain the margins near the current ones.

Regarding , utilization of existing branches, need to check - BUT they do have humongous CROSS-SELLING opportunities wherever feasible/possible. They can leverage the same retail customer base here (from gold loans ) for other types of loans(vehicle/home).

here are some additional points from Conference call(from a brokerage report):

–Presently, Non gold loan business accounts for 15% of the total. The management has cited about increasing it to 25% level by 2018 and further to 50% by the end of FY20.

–60% of the total business is now through online channel increased from 50% on Y-o-Y basis.

–Management stood positive about Q4FY17 and expects it to be better than Q3FY17, which was impacted by the demonetization drive.

2 Likes

Read more at:

http://economictimes.indiatimes.com/articleshow/57124436.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

…

Second, we are very bullish on this gold finance companies like Manappuram and Muthoot. That is one space where competition has been declining very steadily. They do not have pressure to pass on the declining interest rate to their borrowers because it is like a short-term loan. The interest rate on your credit card never falls. The gold loan is more like a poor man’s credit card and you do not expect the lending rates to fall because it is a short-term loan.

…

So on my FY18 earnings. Mannapuram and Muthoot both are available at less than 10 times

earnings. This is not possible in the NBFC space given the frenzy we had. So

these are the only few pockets where valuation is still very attractive and

_earnings growth is very strong. _

On Mannapuram and Muthoot, we are hugely positive for macro as well as micro

reasons.

1 Like

Is there any relation between the stock price fall of Manappuram and its appointing Nucleus software for its services?

why stock is falling irrespective of such a good results…anything we are missing?

Nucleus soft has one of the best IT solution for lending biz. It should be taken as positive.

1 Like

Lot of good news for Manappuram Finance - Excellent Q3 results, Deal with Nucleus to implement new IT Solution, Board meeting scheduled on 17th Mar to discuss the business plan for next financial year…

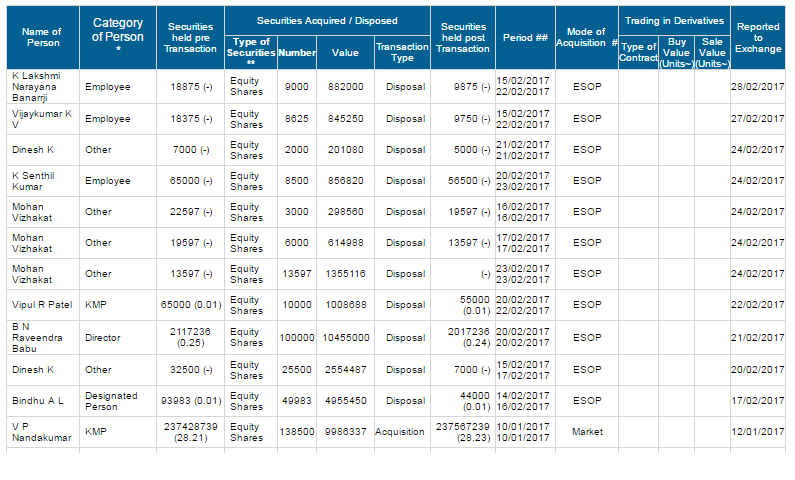

However, I am struggling to understand why insiders are selling the shares considerable in recent times. Is anyone got a view?

Regards,

Vinoth

1 Like

these are ESOP allotees and i wouldn’t be too perturbed with their selling. they’ve seen levels of 59 in the last 2 months so these prices are enticing enough for them.

I agree, BTW, there also have been “Acquisitions” by Mr. Nandakumar over past few months. If we see these acquisitions/disposals are roughly around 2-3 crores - this is negligible compared to current market cap of ~8000cr.

Has anyone received the dividend announced for Q3? The record date was 18th Feb and most companies pay out within a week of record date.

Invested in Manappuram for the first time in January so not sure if company generally uses the full 30 day window from dividend declaration for payout.

They had announced that the dividend would be credited on or before March 9. Reference below.

1 Like

The risk on declining gold price has reduced for sure by their multi-pronged strategy (3 month loans, lower LTV for longer durations)…but here is what Mr. Nandkumar had to say in a recent interview -

He expected 20 percent compounded growth annually for next three to four years, adding that moderated gold prices would be key. He expressed confidence that the company would not face much competition from banks that lend against gold.

-

I think what he means is that high volatility is what kills their profits (if it is declining). Stable/Rising gold prices is very good for business. Moreover, they were able to grow despite declining gold prices. Only worry is if the price fall is too quick (sudden volatility).

-

In declining gold price scenario, lower LTV indeed will help reduce defaults but AUM growth would certainly be impacted. They are lending against collateral, where the size of loan depend on the size of collateral. if value of collateral goes down, loans amount would be less.

-

When gold price are on the decline, can’t they ask for more collateral from the borrower if they would like to keep the loan? Or else, as @Yogesh_s bhai said, either they should close the loan or should auction early in case of default. This would minimize the risks involved (minimize loss of profits). How are they doing it currently?

1 Like

There are two ways Manappuram can hedge the gold price risk.

-

Include a margin call in the loan agreement. Should the value of the collateral fall below the maintenance margin, Manappurum should issue a margin call to the borrower and if the borrower is unable to put up sufficient maintenance margin, Manappuram gets to auction the collateral immediately instead of the current waiting period of 90 days. This is how all brokers lend money against shares and I am sure current regulations will allow such lending. This will significantly reduce the gold price risk and it will allow Manappuram to lower interest rates enabling it to grow its business further and get an advantage over banks.

-

Buy gold puts. If gold price drops, its puts will appreciate to offset potential losses from loans going underwater.

I am not too familiar with lending regulations but I am sure these options are available to a gold lender.

2 Likes

@Yogesh_s - If there is some provision like that, why are they not using it at the moment? Or are they?

A margin call wouldn’t really go well with customers. Some may not even understand it and they will just go to another lender who don’t give margin calls. Manappurum actually does not lose a lot going by the past data when gold prices drop. NPAs go up but eventual losses are low. Main impact of lower gold prices will be decline in their loans outstanding and consequent drop in interest income rather than spike in loan losses. As long as gold prices don’t go on a perennial decline, gold lending will continue.

I do see increased competition from banks. I see lot of advertisements from all local banks in my area who are offering gold loans. Higher credit risk might just work in Manappurum’s favor as it will keep marginal lenders out of this business.

3 Likes

Even I havent received the divdend …

div has been credited

1 Like

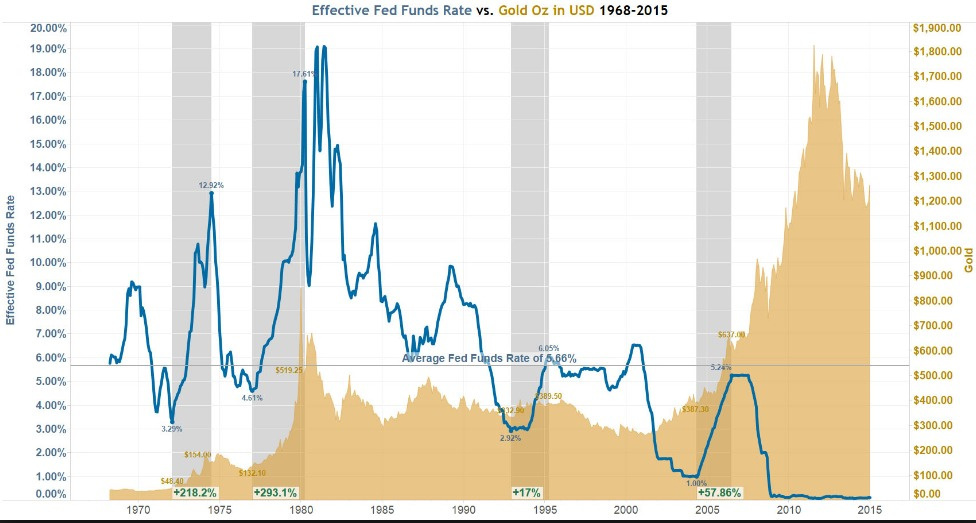

@Yogesh_s bhai - What is the correlation b/w US Fed Rate hike and Gold? There is contradictory opinions on the topic.

As per one of the investopedia articles - “Rising and higher interest rates may in fact be bullish for gold prices, simply because they are typically bearish for stocks. … Higher interest rates mean increased financing expenses for companies, an expense that usually has a direct negative impact on net profit margins.”

Came across this chart (US Fed rate vis a vis Gold prices), which suggests its actually diretly proportional.

Another piece, as per which -

“Gold prices suffer on likely US Fed rate hike

Anticipation of an interest rate hike by the US Federal Reserve put gold prices under pressure, correction to the tune of $40-50/ounce expected”

There are so many studies i found, looks like the opinion is mixed.

I believe in short term, rise in fed rate is bearish for gold, but in long run it is bullish. Your thoughts on this?

Gold is generally considered as hedge against inflation. Inflation is a result of too much money chasing too few goods. Too much money is a result of central banks lowering interest rates and printing (too much) money. So when central banks like Federal Reserves and RBI starts raising interest rates, there is an expectation that money supply will come down and inflation may come down with it or at least inflation expectations come down which causes demand for gold to come down causing gold prices to drop.

When Fed was lowering interest rates in 2008 and then started QE after that, gold prices shot up from $600 to $1800 fearing that such money printing will cause inflation. Since that did not happen, prices retreated to $1200.

2 Likes