after denying any talks repeatedly, it will be a kind of somersault to announce being acquired. And the promoters clearly believe that the stock is undervalued. It looks likely that they are acquiring another company to deploy excess capital or some big investor (Piramal kind etc ) want to invest by taking large (~10-20%) stake. This could result in re-rating of the stock and eventual exit of the promoters later on. I have always believed that running a gold finance company is not easy. Just my side of speculation.

To me this seems to be the most likely scenario. They probably have some investment proposals from more than one entities, which they might be discussing and deciding over in the meeting on Tuesday. They might not be selling the controlling stake just yet but a small stake as you said.

Yes, mgmt has been denying the stake sale rumors but poeple mostly remain tight lipped till the deal is struck. If they are getting a good valuation, i think mgmt will be prudent.

Another possibility could be offloading part of business like micro finance to some bank considering latest structural development , deals n outlook

Authorised Mr Nandakumar to initiate further discussions on behalf of the company on investment opportunities available with the company.

Unfortunately, the announcement is a bit difficult to understand. Still not clear - whether this means the company is looking to sell part of its stake or is it looking to acquire another business as an inorganic growth opportunity.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/b44ad365-48c1-417e-8762-20774bb2c7c8.pdf

I may be wrong, but I think it is kind of straight forward that Manappuram is exploring new opportunities to invest further as it is one of their stated objectives to diversify away from gold loan financing. If someone else is investing in Manappuram, they would have notified as divestment options rather than investment opportunities!

7 Likes

Looks like will get rerated sooner or later

One article re rates the company?

For gold loans, which are adequately collateralised, why does the interest rate be northwards of 20%? Even mincrofinance loans without any collateral are being given at this rate.

Sense of urgency , Availability of other options in market I think r two key reasons

EPS of 2.05 vs 2.26 YoY

QoQ flat

Consol 2.06 vs 2.41 yoy

2.06 vs 1.90 qoq

Consolidated revenue growth of 5.15% QoQ, which is good!

Decent set of results from manappuram

Gold business

-

gold loan AUM up 5% QoQ, disbursements up 26% QoQ

-

operating expenditure to AUM down to 9.2% from 9.3%( which was going up during last few quarters), GNPA and NPA both down QoQ

-

Net profit flat

Asirvad MFI -

Finally seems to have turned around and given a small profit

-

AUM growth 7.5% QOQ and 27.9% YoY

-

NII growth 10% YoY and 22% QoQ

-

PAT up 101% QoQ ( Yoy suffered due to demon), turned loss to profit

-

Provisions down 18.5% QoQ

-

GNPA up slightly to 3.8 from 2.8 and NNPA down to 0.52

Housing finance had a flat AUM this quarter

CV finance did well with a 21% AUM growth

Expecting the MFI busniess to play well next quarter with risks being rise in interest rates

would wait for some more details in con call

DIs: invested since 80, added again @110

5 Likes

With much improved performance this quarter, we have now put the fallout from demonetisation behind us. From now on, it will be business as usual, we expect growth to pick up to the levels we saw before demonetisation," said V P Nandakumar, MD &CEO, Manappuram Finance.

The company is looking at fintech investment or strategic buyouts but there is nothing concrete yet, said Krishan.

1 Like

Sorry this may sound like a very amateur question. But can somebody explain what is the difference between these 3 items with a live example if possible?

- Gross NPA

- Net NPA

- Provision.

1 Like

Suppose bank has financed a loan of Rs 100/- but due to any reason bank is unable to recover the loan amt plus interest and as per RBI guidelines if bank is unable to recover its loans say in 90 days, the amount has to be transferred to NPA category. Bank has to create provision on this NPA after classifying it sub standard, doubtful or loss asset. This provision is deductible from profits of the bank also. In this case, if the account is classified as Sub standard and bank make a provisio of 10%, then the provision in this case will be Rs 10 and net NPA will be 90 i.e. Gross NPA Rs 100 - Provison Rs.10.

21 Likes

https://m.rbi.org.in/scripts/Glossary.aspx

Better to always refer to RBI glossary for definition. e.g

Net NPA = Gross NPA - (Balance in Interest Suspense account + DICGC/ECGC claims received and held pending adjustment + Part payment received and kept in suspense account + Total provisions held).

1 Like

Management thinks it can grow at 20% CAGR

Value price to earning is half of growth

In this bull run where all companies have price to earning more than cagr ,this is a company whose growth was interrupted because of demonetisation

Now they have derisking their business by diversifying

Captital adequacy is best in the business

Promoters bought at almost the current price

Excellent band

Honest management

Dividend yield is good

Currently market is too pessimistic about manappuram,but I think sooner or later rerating will happen

Also they are looking to cut the security expenses by digital security

Housing will pick up in future due to affordable housing

Vehicle finance doing good

And Microfinance has turned around

Anyhow for some reason beyond my understanding market is too pessimistic

May be I am missing something,not sure

4 Likes

Management have been guiding 20% growth all the time. But the reality is different. Review the YOY growth rate and you will get the picture. Diversification is good. But they are still a gold loan company predominantly. Therefore when the primary business growth rate falters it is a major red flag. Also gold loan have no direct relationship with demonetization or GST and these are no reasons for reduction in growth rate. I agree the valuation is cheap and I think it is cheap for a reason.

3 Likes

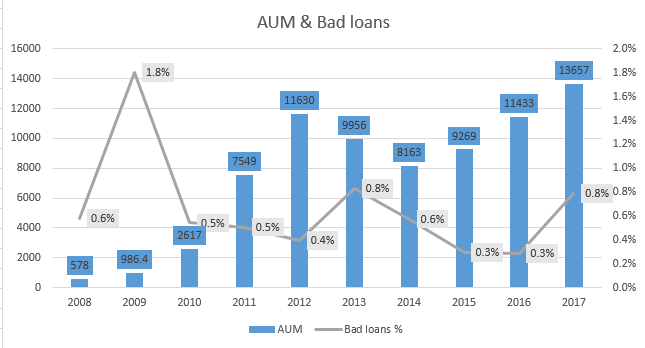

Hi all,

This is the first time I am trying to analyze an NBFC. So please pardon my ignorance. I have tried to assess the total write offs that Manappuram has made over the years against the total AUMs in a given year. Here are the numbers.

| Year | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|---|---|---|---|---|

| AUM | 578 | 986.4 | 2617 | 7549 | 11630 | 9956 | 8163 | 9269 | 11433 | 13657 |

| Total write offs | 3 | 18 | 14 | 38 | 46 | 83 | 47 | 27 | 32 | 108 |

| Bad loans % | 0.6% | 1.8% | 0.5% | 0.5% | 0.4% | 0.8% | 0.6% | 0.3% | 0.3% | 0.8% |

-

All numbers are at the consolidated level.

-

Bad loans have been derived by adding up “Provision for standard assets” & “Bad debts written off and provision for bad debts” from Cash Flow Statements for corresponding years.

Total write offs of 416 Crs in 10 years for a company with an AUM for 13700 Crs isn’t bad at all.

Disclosure: Invested

5 Likes