CFO manappuram

1 Like

Hmm

I have increased my allocation to manappuram

NPA of mannapuram is 1% while of

moothoot

is 4-5%

Going forward security cost will come down

Loan growth will improve

Management said 20% growth

Ashirwad has turned around and we will see profit in 1-3 quarters

Vehicle finance Is doing great

Home loan aum will be 1000cr in 3 years as per management with the new housing team

Diversified in 4 sectors

Demonetisation effect going away

Great penetration in south

Risk :regulatory for gold

Political For nbfc u

To me

Limited downside

Possible rerating soon

5 Likes

Nandakumar purchased 10 lakhs shares of his co, worth 10Cr INR. It is a good sign.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/3f536370-d5a4-4754-a409-1b1e060f0780.pdf

8 Likes

Has anyone else noticed that Asirvad’s pre-provision profit has slumped year-over-year in the last two quarters? Finance costs have outpaced interest income, so it ain’t just about high provisions. Has management addressed this issue?

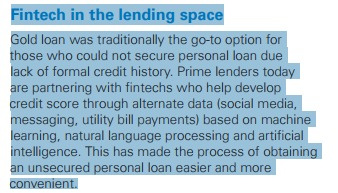

If you read in detail , It says it would be based on their credit score .

And manappuram targets to lower base of pyramid(Most of their customer) where credit score reach is not even closer.

3 Likes

One more development :

Disc: Invested in Manappuram

I am a skeptic about online/P2P lenders. One of my friends was running a company, and they shut it down after 18 months. One of the major reasons was the lack of proper credit information. Since these algos have eventually to be based on some baseline data about the borrower, the target audience for these lenders become really small. This goes against the biggest benefit that internet gives - distribution.

In a nutshell, I am less bothered about P2P platforms on businesses like MFL compared to overcrowding of market. For instance, there are now a number of players (gold,MFI) who are focusing more on market in South India.

(Dis: Holding MFL, may be biased)

3 Likes

big share boughts by

promoter himself

and baring india (which shows as related party transaction )

so i guess a good sign for the company!

2 Likes

Could you pls. paste the screenshot or point to the source of information pls.

look at BSE announcements.

My notes from the Q2 FY18 concall. Please note that i have not summarized financials, which are there for everyone to see. Some excellent questions put forward by participants, which gave insights on the gold loan business model, longevity of this model, succession planning, Aadhar penetration benefits for MFI industry, risks to this business and what mgmt is doing to tackle these, and some misconceptions about gold lending business.

Q- In standalone P&L we have seen a dip in profits (gold loan business), so what exactly led to this given the flat kind of AUM but still profits going down ~10%. So is there any expenditure, which has come up which is one off?

A- There was an other income in Q1 of 19.7 Crores so that is not there in Q2. So that is the only reason.

Q- Is gold lending business undergoing a structural change? Because when we look at the growth of the gold loan business vis-à-vis other NBFC businesses after demonetization can we say that structurally competition is emerging for the gold loan business from other NBFC doing consumer durables financing or small ticket SME financing or SFBs because gold loans do tend to be expensive as compared to the sources of finance. Is this a threat to the gold loan growth business of ours?

A- No. Our customers are from the bottom of the pyramid from informal unorganized segment so these were the customers who were most affected due to demonetization, which is the reason for stagnation. So, the demand was lower the economy was not doing well. It led to a situation of higher auction. We do not see much competition compared to the previous quarters. It is more or less similar and as I said what we expect is that three years our expectation is to grow the gold loan portfolio at 15% CAGR starting Q3 onwards.

Q- Security costs ~200 cr annually. Will it come down?

A- Security was beefed up due to robberies. They are adopting new storing mechanisms to bring these costs down to 50 cr annually in next 2 qtrs. Discussed some cellular storage model from Godrej (security solution).

Q- For MFI business, what was the porftloio at risk and what are the current numbers.

A- During demonetization, 420 cr of the portfolio was at risk, which is now down to 125 cr. We have written off 109 cr till Oct 30. Balance provisioning has been 58 cr. Hopeful to recover another 100 cr of this number. So, max. risk now is ~20 cr (Further provisioning that might be required). Major write-offs are in Karnataka.

Q- Housing Finance business NPA and growth are not as expected. Reasons?

A- CEO left, and the new team is in place now. Focus on reducing NPA. Hopeful tor educe Gross NPA to 2% by end of this year. Aiming 1000 cr loan book in 3 years. Very good prospects.

Q- Auctions in this qtr?

A - 200 cr. We expect this to come down as rural economic situation improves.

Q- What is the gold lending mix between business loan and consumer loan?

A- One-third is agri sector, another one-third is working capital for this micro businesses, and further one third for consumption.

Q- With gold lending, you mentioned demonetization as the reason for AUM stagnation. On further delving, my sense is that when the rural economy weakens, they will need additional credit; so they have to come to Manappuram, pledge their gold, and then use that credit further for agri sector or for their small business or for their consumption. So, this is contrary to what has happened?

A- This the wrong impression about gold loan. The gold loan is no longer distress loan. People use it as working capital in the rural economy. The requirement of working capital comes whenever the economy is fairing okay; as the economic activities go down, the demand for borrowing naturally comes down.

Q- Is the opportunity size of the gold loan reducing since the advent of Jan Dhan Bank account. How many people would be interested in taking loan at the high rate of 23%-24%?

Q- See the Jan Dhan account and other things they did not reduce the scope for gold loan. The gold loan scope is there and you will see in the coming quarters the gold loan is back to what it had been.

Q- Succession planning?

A- The second generation is already in this business. I am assuming on bottom role as it will take sometime for them to come back to be in the leadership of businesses. Daughter is a medical professional. She is in the business now. Two sons they are business graduates. They are also in the business.

Q- With the advent of Aadhar, KYC, and the high marks credit bureau what about the defaulting persons? Were any primitive actions taken for those who have not defaulted and returning, and any measures that are left for us to be taken, and are there any credit records?

A- In MFI industry (as such, today, post demonetization) we have close to 50 lakh defaulters. As an industry as a whole, we are very clear that even if someone defaults one company, no other company is going to lend them. So, we want to bring in more discipline. Out of ~6 Cr borrowers, 50 lakh people (12%) are now in this list and I am sure that more discipline will come into the market, and we will find new borrowers. When we look at the bottom of the pyramid, we have now more than 20 cr people here and we have not even covered half the market. So I do not think demonetization has really affected the business; in a way it has brought more discipline in the market and that is the reason everybody is back to the normal collection efficiency.

Q- On Aadhar benefits?

A- Very helpful. This provides them information on how many MFIs have lended to a person. 99% of Asirvad customers have Aadhar now.

Disclaimer: Invested. Added more in last 3 months.

19 Likes

Here’s the KPMG report on India’s gold loan markets

1 Like

Thanks for the summary

Thanks for the link, Aashish! Most of the stuff which has been covered in this report has already been discussed on this thread. I am just pointing a few key points (risks), which should not be ignored -

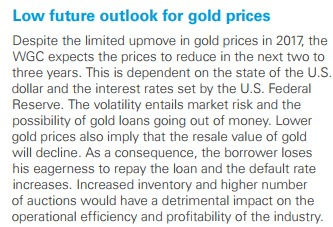

Lower tenure loans does help mitigate risks, but lower gold price means lower AUM growth.

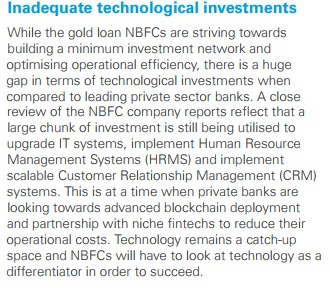

Focus on online disbursals is a good step. As mentioned in the recent concall, increased Aadhar penetration is helping NBFCs a lot.

- Central gold repository model may be the future, but with the current demographics in India, may be relevant in very distant future.

1 Like

The first point is a disruptive risk but my question is, even with the AI, where is the collateral? No lender will lend without:

- A fixed source of income; or

- Collateral security.

Indians love their gold and have more than they can wear. This works as an excellent collateral for gold-loan companies. They can, however, use Fintech to target customers outside their current market and that’s where the edge will come against industry peers/ non-organized sectors.

3 Likes

yes having the same questions. Report tells that the future would be Data driven unsecured loans. Would these un-secured loans be just based on data available in public domain and use blockchains/smart contracts as collateral or something ??

seems possible

I am not an expert in blockchain but whatever i have read about it is that blockchains/smart contracts do not need any kind of trust or collateral.

CEO Mr. V.P. Nandakumar has bought 3.015 lakh shares from open market on 14th of this month

http://www.bseindia.com/xml-data/corpfiling/AttachLive/fbdf71ea-2ed6-45f8-bc05-4c4d61122b13.pdf

2 Likes

After a nice up-move last year…the stock has consolidated well around 90-100 levels. Also the demonetization disruption seems to be largely over(going by the conf calls of Manappuram, Muthoot and other MFI’s) - IMHO, growth is back on track. Feel the investment thesis shared in the past is largely intact.

Mr Nandakumar adding stake for the last 2 months is a definite positive. Q3 results could be the trigger for the next up-move.

Disc: Good chunk of my portfolio. Holding since 2.5 years. Also added more during demonetization. Views are definitely biased. Please do your due diligence.

6 Likes

My take is, sell thought should be based on deteriorating fundamentals or personal needs. You don’t sell a company just because price is rising. Manappuram is a good company in all aspects as per me, and when a good company gets market visibility because of it’s value, there’s absolutely no limit as to what levels the price may rise. Holding onto a stock during these times can reward tremendously in long term. I don’t think any great investor had ever sold a fundamentally sound stock just because the price is rising. I personally committed this mistake in stocks of Endurance Tech, Balaji Amines, PI Industries, Sunteck Realty, Divi’s Laboratories etc. I sold because price rose and valuations became expensive, but they kept rising and rising that I regret selling them, and I cannot buy them now as comfortably as I did buy them when I bought them because of current valuations or the recent run up that has happened in them. Had I held on to them, my portfolio would have boosted by now.

Disc: Holding around 30% of my portfolio, no thoughts of selling as of now

5 Likes