Gold loan and Microfinance are niche areas that both public and private banks stay away from. They have even tried and could not succeed. Manappuram as such targets unbanked segment so I expect the impact to be low. Even for private banks the impact should be minimal until all PSUs blow up the additional capital and get back to old ways.

7 Likes

If they knew how to satisfy retail, they would’ve gone to corporates . Infusing capital is easiest thing to do, infusing performance culture is key n there are structural reasons why it won’t happen if assumptions intact.

4 Likes

Hi Hitesh,

Manappuram seems to be nicely poised in a symmetrical triangle type of a pattern, good to decent results should give a breakout? Am bit of a novice, but tried my hand at it :

How does it look to you on the charts?

3 Likes

Is anyone here worried about loan book de-growth over the last few quarters, and the failure of quarterly disbursements in the last few quarters to show growth year-over-year? I understand economic conditions have been tough, but will you want to wait and see decisive signs of a turnaround in the company’s loan-book before committing money? Interested in people’s rationale.

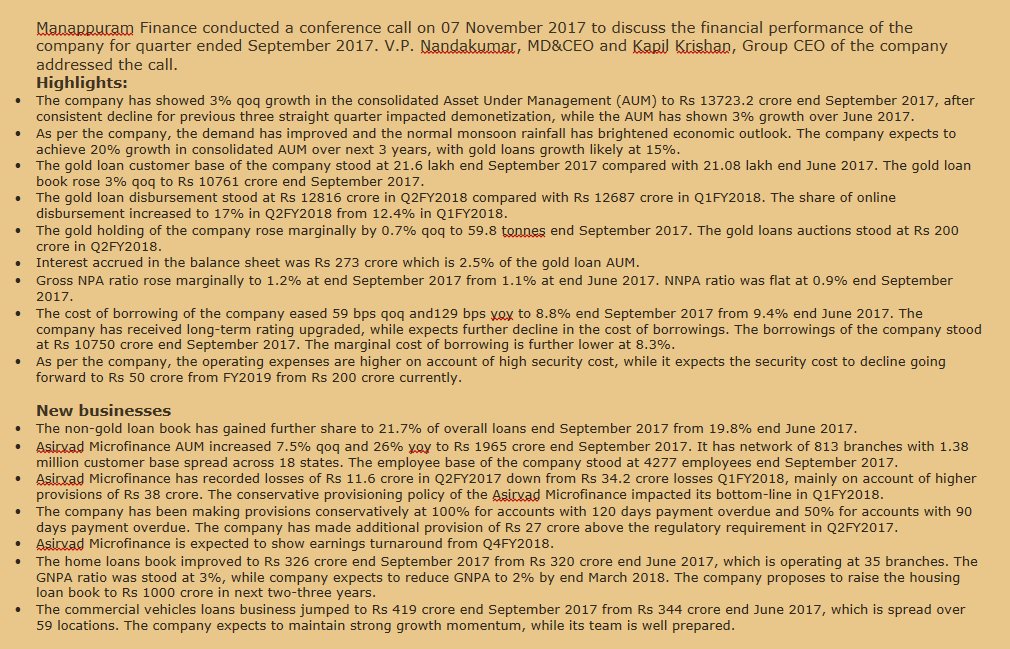

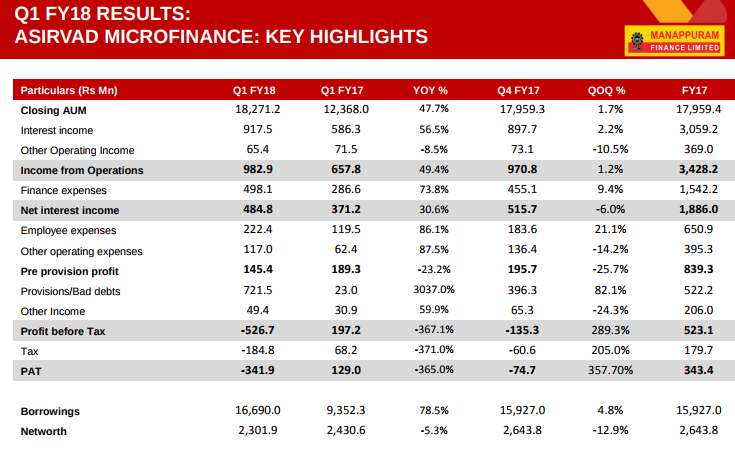

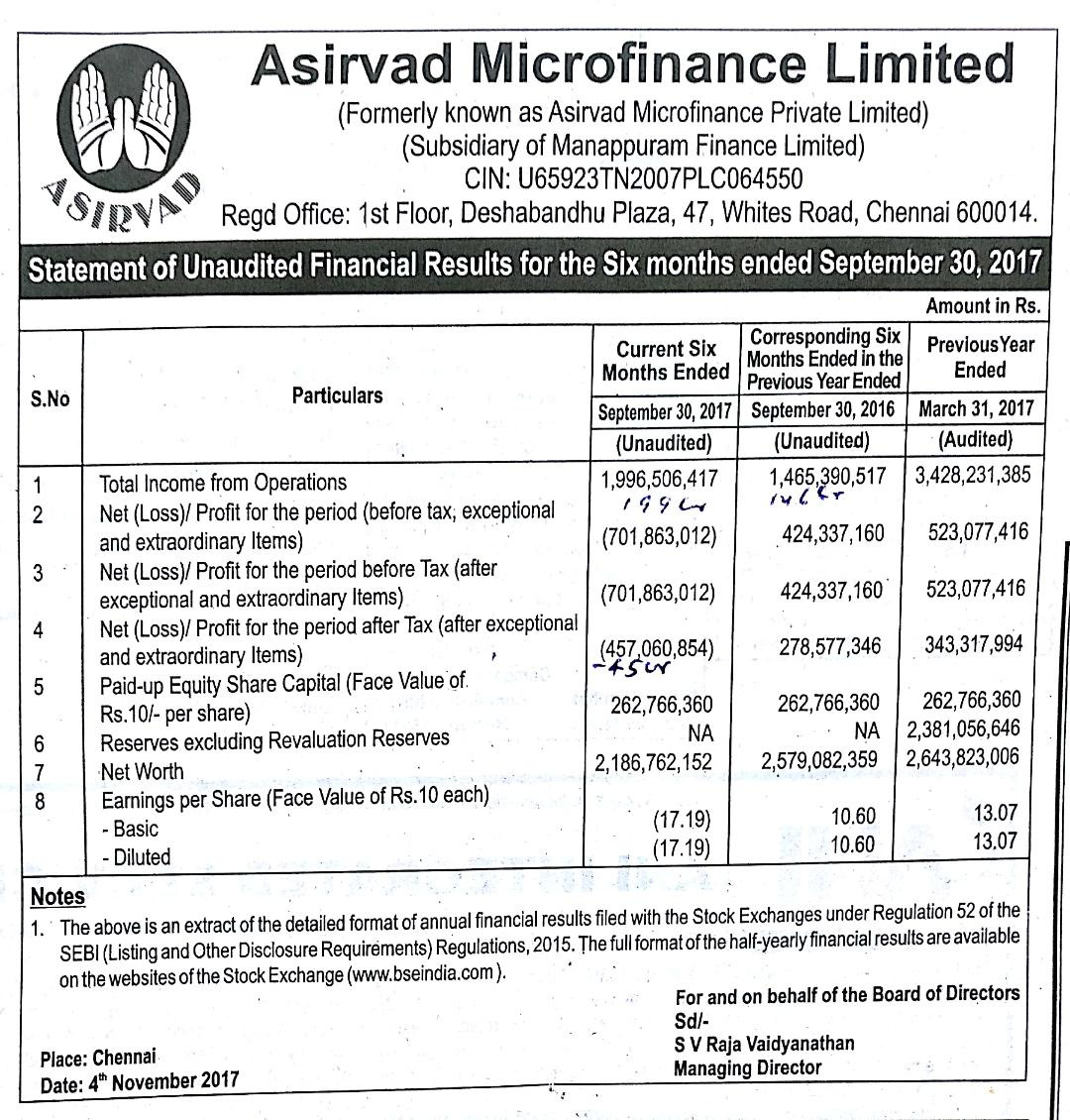

Today Asirvad Microfinance result is published in Business Standard, kolkata. on page 8. Result is for 6 months combined ending Sep17.

income is shown as 199.6 cr v/s previous yr six months 146.5 Cr.

net profit is shown as -45.7 cr v/s previous yr six months of 27.8 Cr.

for Q1fy18 net profit for Asirvad was - 34.1 Cr. that means they have booked another loss of about 11.6 cr in this qarter. am i correct?

Q1 data from manappuram investor presentation:

2 Likes

#Manappuram #Results #Q2 2017-18 Results.pdf (2.6 MB)

SRC: https://nseindia.com/corporate/Results_07112017164606.zip

Results look very pedestrian …

I am not able figure out the NPA numbers. I did not see them in the PL statement.

Can someone please point the Provisions/Contingencies/Writeoff number to me! Thank you!

Edit:

Provisions are down from 80 crs to 46 crs

1 Like

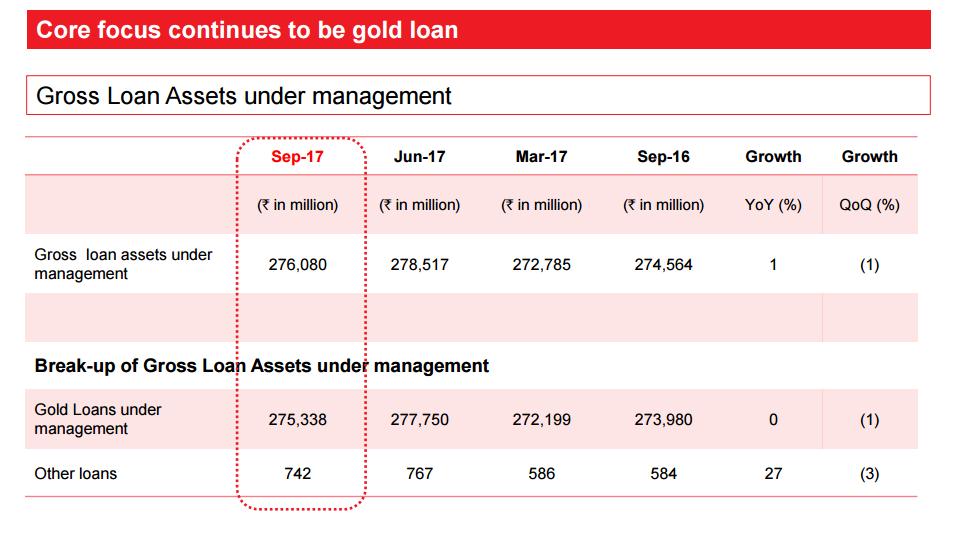

Though NPA challenges reducing and all numbers related to NPA in terms of day PAR, provisioning encouraging, the key concern is growth missing in core as well as new segments continuously from 3rd quarter. Planning to est 1-2 quarters more for growth to come back. I think may be because company is conservatively not getting into longer duration gold loans were customers have other options. Any insights on this would be appreciated

3 Likes

In the last concall the management had mentioned that although the tenure of the gold loans are of 3 months duration, but most of them get renewed without any payment happening if the customers pay their interest. So that shouldnt be a concern in my opinion.

1 Like

Again good set of numbers from Muthoot Finance in Q2 FY18…

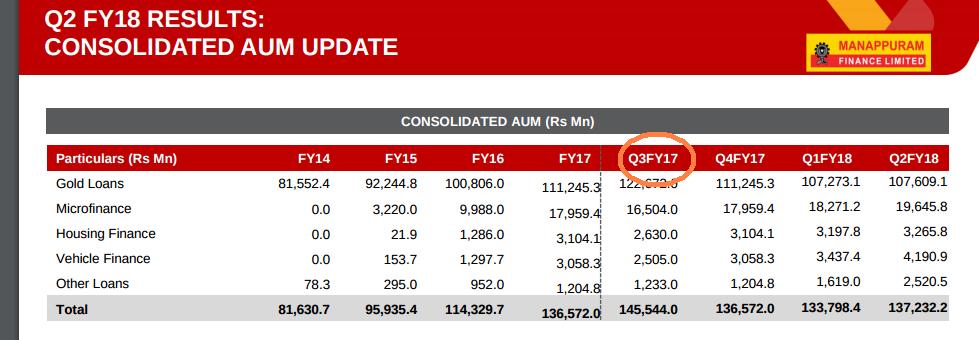

Manappuram was struggling since last 4 quarters… Asirvad Microfinance contributes only 8% of overall AUM and that too Q2 FY18 is much better. The key concern is, Why good loan business line is negative to flat in Manappuram when competitor able to show decent growth?

Disc: Invested in Manappuram at lower levels and no trading in last 1 year.

Regards,

Vinoth

1 Like

Gold Loan AUM - Muthoot marginal decline vs. Manappuram marginal growth Qoq

PAT - Muthoot PAT is mostly coming from NIM expansion but Manappuram has already taken that benefit

GNPA - Muthoot doubled QoQ to 4.56% vs. 1.1% for MFS

NPA: Muthhot 3.99% vs. 0.9% for MFS

Other segments - Due to higher costs/NPAs etc other service lines like home loans and MFIs have not been contributing to MFS but Muthoot is better placed.

Let’s not go by PAT numbers alone. MFS has to work on home loan while MFI has recovered completely. The biggest worry is structural stagnation in the gold loan segment across the industry.

Disc: Invested

9 Likes

I am tired of holding it for so long. No growth in AUMs over last 4 qtrs. Bottom line reducing every qtrs. Cannot live on only hope forever. Liquidated major part of holding today at some loss. Big opportunity loss since many others are going up every day on improved performance. Migrated to Rain Industries- excellent Q3 today.

I think, there are flaws in this reason (joined con call in between ,so, was not aware of this). Taking 1 lakh loan for 3 months and doing 33k payment (assuming 0% interest for simplicity) and doing 10k payment on 1 lakh loan for 10 months are very different consideing personal liquidity perspective. If some takes 1 lakh clears in 3 months and again takes 1 lakh back, this is more of rotating the money. Conservative lending is good but may be this is driving away customers to easier options

Disc: Invested and holding

1 Like

Trending down NPAs

Housing finance and ashirwad may increase profitability in coming quarters

VP Nandakumar, MD & CEO, said: “After demonetisation, the company went through three quarters without growth. But now our consolidated AUM has grown by 2.6 per cent over the preceding quarter. The pick-up in the rural economy following good monsoon has brightened the prospects.”

1 Like

what about yoy numbers for gold loan in Manappuram, they have conveniently skipped yoy nos from presentation. most appropriate comparision is yoy dont u think so ![]()

1 Like

So this is the statement in the concall “One thing I want to make clear, this three months is not three

months, if he has remitted the full interest and also the marking to the market the new

LTV he want to renew it, it can be continued for any number of months” In your example(assuming LTV is at 50% so gold worth 2lakh is given against which one lakh loan is taken), if after three months gold value comes down from 2 lakh to 1.8 lakh, the borrower would have to pay 10k as principal(50% of 20,000 decrease in gold value) and can continue with the loan as long he is updated with interest position. In my opinion, this is a conservative albeit risk averse way of decoupling your risk from gold prices. In three months gold price fluctuation wouldnt be as huge as it could potentially be in a year.

2 Likes

Will do YoY comparison from the next quarter when the landscape is comparable especially after demonetization during Q3 -FY17.

1 Like