It might be related to succession issue… might expected VC could help.

A thought… not sure though

Mannapuram block deal at 102.4 per share at a total value of 9.2 cr

2 Likes

Kindly give the source / link of the same. Thx

Company denied any plan of stake sale

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=4db2cd93-5495-401e-aa63-0535287a348a

2 Likes

Interesting to note is the fact that Mr. Nandakumar has denied selling any stake, he today holds around 35%. Though is wishful thinking at the moment but there can be another promoter coming on board who buys stake from open market, and hence compliments his current business with this one.

Can be all win.

Disc- Invested from lower levels.

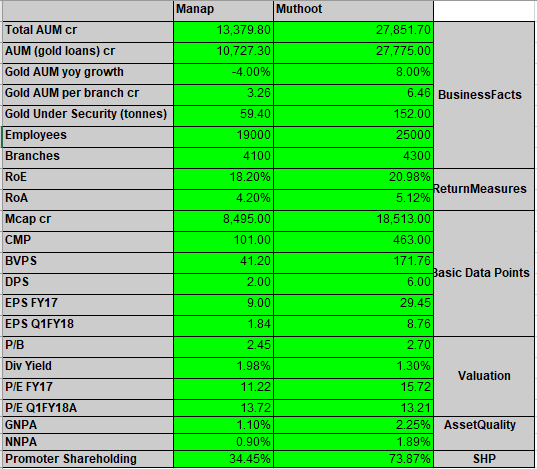

Manappuram vs. Muthoot comparison

Note: Manap NPA figures on a standalone basis.

11 Likes

Good post. Another important difference is NPA recognition period. Manna does 90 days and Muthoot 120. Once, Muthoot moves to 90 days in Q4FY18, NPAs will be even more.

4 Likes

thanks Rajesh, that’s an important point of comparison.

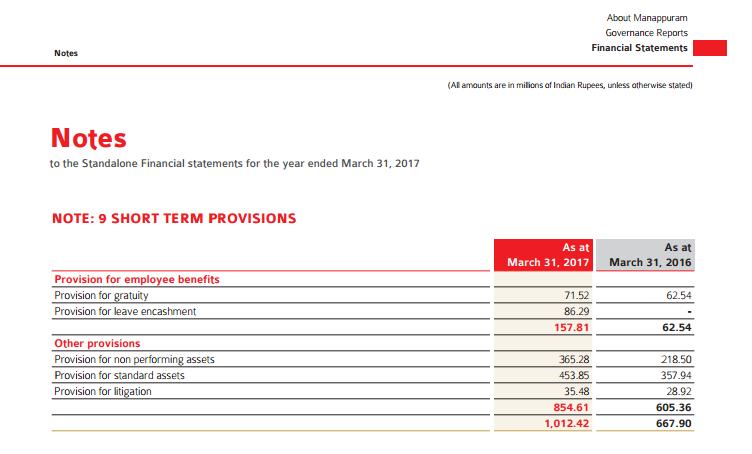

good post, but provisioning numbers for mannapuram and muthoot are much different. Let me provide individual info.

- mannapuram has total provisioning of @81 cr. for AUM of @13400 cr. (provisiong of 0.5%)

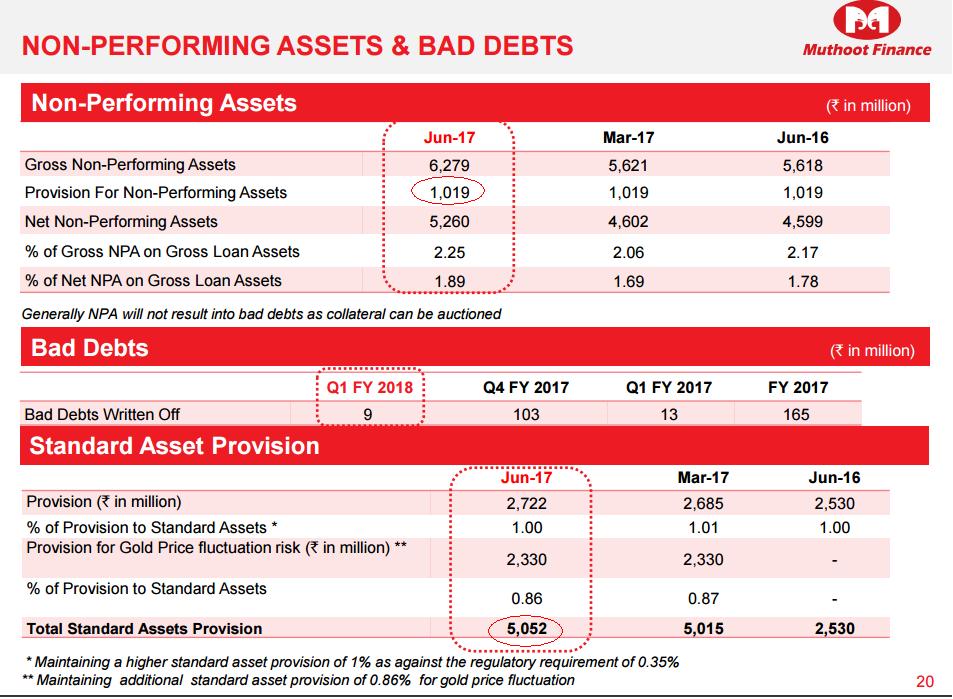

- Muthoot has total provisioning of @606 cr.(101 for NPA & 505 std. assets) on AUM of @277700 (provisioning of 2.1 %)

if we think logically manapuram has more riskier loans(1827cr. out of 13400 are micro finance ,non secure lending),so theoretically mannapuram should provide more in relation to AUM.

-

mostly investor just compare PE ratio and says muthoot is expensive. but spare some thought if muthoot had not provided for standard asset above RBI Guidelines(0.35% is rbi prov.req. vs 2% held by muthoot) its profit and book value would be higher.

-

most of muthoot finance NPA are secured gold loan asset (lower MFI assets propotion vs mannapuram) and can be monetized easily.

Disc: hold muthoot finance ,no position in mannapuram

8 Likes

3 Likes

My notes from Q1 FY18 Concall -

MFI -

-

On MFI, particularly now the industry has bounced back. The worst is behind us. With this quarter provisioning we have faced whatever possible PAR or NPA in the industry in the last three quarters. So, we are on a good wicket now; the disbursements have picked up considerably. This quarter was flat, because more or less disbursements and collections were same. From July onwards the disbursements have also picked up now. You know that all of us go through a credit bureau check and those passing the credit bureau didn’t get the loans and this has now again come back, which means that the borrowers are repaying their old loans. And we expect the industry, it may not grow at that rate as earlier, but definitely it is growing at a reasonably good pace. There may obviously be some more provisions. There is also likelihood of collections coming from the old book.

-

So basically the way I see GNPA is that 90+ days is 6.93 and 60+ days is 7.7. So, the difference is what is stuck between 60 to 90. That will indicate that largely it is taken care of. Disbursements made post December have almost 100% collection efficiency.

-

The demonetization has really given lessons in where to really expand. We have certain states in India such as Maharashtra, UP, Haryana, Karnataka which are more politically sensitive than other states and where the local smaller politicians play a havoc on the borrowers. So what we have done is, we have done a complete risk mapping now and internal strategy has been revised to grow more in South and Eastern belt of India. We will have the presence in Northern and Central India but it is much reduced portfolio. We will have coverage but reduced portfolio till situation changes. Eastern belt like Orissa, Jharkhand, West Bengal, Bihar and the North-East also where we have recently entered, we will focus on that. We will have a portfolio around 60% to 70% in south and east and balance only in the other areas. That is the revised thing we have done. This is formulated right from April and we are following it.

Gold -

-

Regarding the gold loan our NPA has come down because we follow regular auctioning of overdue accounts. We didn’t change the policy. We needn’t take the leeway provided by the RBI. I think the next two quarters will be better for gold loan. Even though the customer acquisition continued at the same pace at the later part of the post demonetization era, the auction pulled down the growth. We don’t want to give any guidance during the current year. I think there are signs of improvement.

-

What I have been maintaining in the past and now also, the gold loan, the tonnage growth will be maintained around 10% to 20% every year. I didn’t want to give any guidance QOQ. I hope this year also that 10% would be maintained. So, 10% - 15% in the lateral growth. So, the AUM depends on the price of the gold. So, i don’t want to comment on that. There was some sharp decline, the rural economy everybody knows was totally disrupted and our customers are from the bottom of the pyramid. So, they couldn’t meet their obligation of repayment or etc. etc. So, we were forced to auction and this led to very higher auction. The things have stabilized, which gives confidence for growth in the coming quarters.

Security cost escalation -

- Had to re-instate security guards in all gold loan branches following a few incidents which happened during the demonetization period to give confidence to the customers. That is why YOY this increase is there. The security guard costs are very high because in some of the larger branches we are putting night guards also. But we are looking at other initiatives which can help to bring the costs down. Per branch it is almost coming to Rs.40,000 per month per branch. If I take 3300 branches, this is huge.

Cost of borrowing -

- The cost of borrowing marginal and incremental cost of borrowing is 8.3%. So, we will expect continuous further decline in the cost of borrowing. We recently got upgraded also in our long term rating, so things are going positive on the cost of funds side.

Non Gold loan portfolio -

-

We don’t want to be revise earlier target of 25% coming from the non-gold. I hope it will be achieved. And more and more efforts is given to secured lending like home finance as well as commercial vehicle finance.

-

GNPA is housing finance segment is 3%. Corrective measures have been taken and new mgmt is confident of bringing it down to 1.5% by the year end.

-

Lending rate ranges from 12.5% to around 16.5% in home finance which includes LAP part also. Average fees currently is around 15.3%. These rates cannot be compared with larger institutions because we finance purchasing home by the unorganised sector - barber, small shop keeper etc. etc. who are really un-banked now.

General -

-

The proportion which would be more than one lakh in ticket size is basically around 50%.

-

In the disbursement…actually 60% is rolled over the same day as the LTV. So these are permanent customers; the loan just continues with them for a long time. So that is the largest portion of that. In which case there is no actual transfer of money. We just reset the LTV so that the risk is less and they pay the full interest.

-

Eefforts are to maintain the ROE at 20%

-

Operational expenses will be in the range of 7% to 8%.

-

Gold loans are basically short-term in nature like a credit card borrowing. This is not very interest sensitive. So unlike long-term borrowing like structured clause, these demand loans, the necessity of lowering the interest I think will not come a big issue. Another thing is that the cost of the operating as you have mentioned because of the security you mentioned also, dacoity, robbery etc. etc., already increasing. At this point we felt like no need of reducing the rate of interest. Our average contracted rate is around 22% and that can be maintained.

30 Likes

Thanks a lot for sharing. Great job done.

These are some real world risks. Though financial loss could be limited, reputational risk is always there. A good way to sell stolen gold is to mortgage it and let MFS sell it in auction later.

Disc: Invested

1 Like

In the latest share holding Dolly Khanna has picked up 1.3% stake http://www.bseindia.com/Corporates/shpPublicShareholder.aspx?scripcd=531213&qtrid=95.00&QtrName=

I think it is reduced. As per March SHP it was 102,08,675 shares now it is 95,34,454.

http://www.moneycontrol.com/bse/shareholding/shp_public_shares.php?sc_dispid=MGF01#MGF01

Centrum is bullish on Manappuram Finance has recommended buy rating on the stock with a target price of Rs 140 in its research report dated October 13, 2017.

Dolly khanna has actually reduced his holdings by small quantity…name of Ashish Dhawan is also not appearing. He used to hold 1.49% stake in the company as per march 2017 shareholding pattern.

The company is not giving good results in last 2 quarters largely due to stress in microfinance business and no growth in gold AUM. Although company is still cheap compared to other NBFCs.

4 Likes

1 Like

IMHO, the only number that we need to track here is Ashirwad’s NPA and profitability. If Ashirwad reports even a minor profit this quarter, then this company is headed to 160 for sure. It’s just matter of a couple of more weeks. The numbers should be out by November first week. Rest of the business segments are chugging along fine. The management commentary needs to be tracked carefully regarding growth in Q3 and Q4. It’s just the MFI business, which is acting as a cap on valuations. However, it can be an easy doubler from here in the next 6 months, if growth picks up for Ashirwadh…whichever metric you use, P/B, P/E , Mcap/ AUM…it’s ridiculously cheap. Will be interesting to see how long the market keeps ignoring this gem in the NBFI space. Perhaps the only mispriced bet left right now in the NBFI space, considering the quality of asset book they are building by focussed geographic and product diversification. I am sure the franchise will be valued at somewhere around RS.25000 crores, sometime in 2018. Since this sector has been on an absolute tear last year and most of the companies are trading at elevated valuations, any re-rating for Manappuram can be very Swift. It’s just a question of when now, and not if.

P.S.: I own a substantial position here and hence my views may be biased. Please do your due diligence before playing this wonderful story.

13 Likes