Has anyone collected information on how much gold is auctioned by Manappuram in each of the last 4-5 years?

A while ago these companies used to give out balloon loan (where interest and principal is payable at the end of the term) and would refinance that at the end of the term so the borrower never really repaid anything. This worked while gold prices were going up and the collateral was always worth more than principal + accrued interest. Do they still use balloon loans or they now use amortizing loans (e.g. EMIs like rest of the lenders)? to me this is the biggest risk even if the LTV is now capped at 60%. A balloon loan that is regularly refinanced is nothing but a ponzi scheme.

sorry for so many questions but checking the story after a long time so trying to catch up.

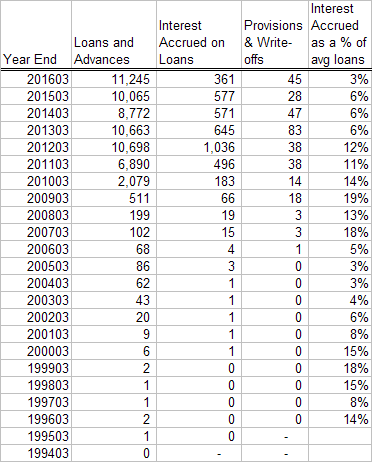

Since a large amount of portfolio is auctioned each year accrued interest on these loans is essentially an unsecured loan that could potentially be written off. With a LTV of 75% and average yield of 23%, borrower will default if gold price drops more than 7.75% (1 - 75%*(1+23%)) in a year since the disbursement. I am not even adjusting this number for all the add-ons like making charges etc that lender consider while calculating LTV. Given the volatility in gold prices, this is very likely especially over the next year or two since gold prices have gone up in 2016.

that makes accrued interest a key monitorable for this industry. And the story is good here. Here are the numbers

Amounts in Rs cr.

Accrued interest peaked in 2012 exactly when gold prices peaked as lenders just refinanced existing loans at the end of the term. When prices dropped, borrowers defaulted as value of collateral suddenly became less than amounted owed mainly because of accrued interest. Write-offs peaked a year after accrued interest peaked.

Over last 2-3 years, company ha learned it lesson and it is now collecting accrued interest at regular intervals or making short duration loans so accrued interest does not build up. That appears to be working. Accrued interest is down even when loan portfolio is growing.

Manappuram has done away with fixed LTV. Now LTV is a function of the tenure. Longer the tenure lower is the LTV. Also interest is now collected at regular intervals and not in bullet repayments, like before 2012.

I had posted on this thread about this earlier this year.

While interest is collected at regular intervals (monthly I think), principal is not. For the borrower, repaying the principal will always be a simple function of gold prices. If gold prices fall, there is no reason for him to pay a higher price and take his gold back.

People don’t seem to understand that this is actually a riskier business model than Microfinance inspire of the so-called ‘secured’ nature of the loans. Gold prices and ‘evergreen’ loans are a recipe for frequent disasters.

Gold prices have fallen sharply in the past month and so you will see a definite impact.

Gold prices were fluctuating for quite few years…is there any past data for considerable defaults with Manappuram or Muthoot because of gold price fluctustion?..if yes then it’s a risk…i have not seen any considerable defaults in the past

They got badly hit in FY 13, while they are slightly better protected now because of lower LTVS, it is still a core business model weakness because principal is never really repaid when prices go up (loans in fact get topped up) and while prices go down principal isn’t repaid because the borrower isn’t stupid to pay a higher price than what his gold is really worth to collect his jewellery back.

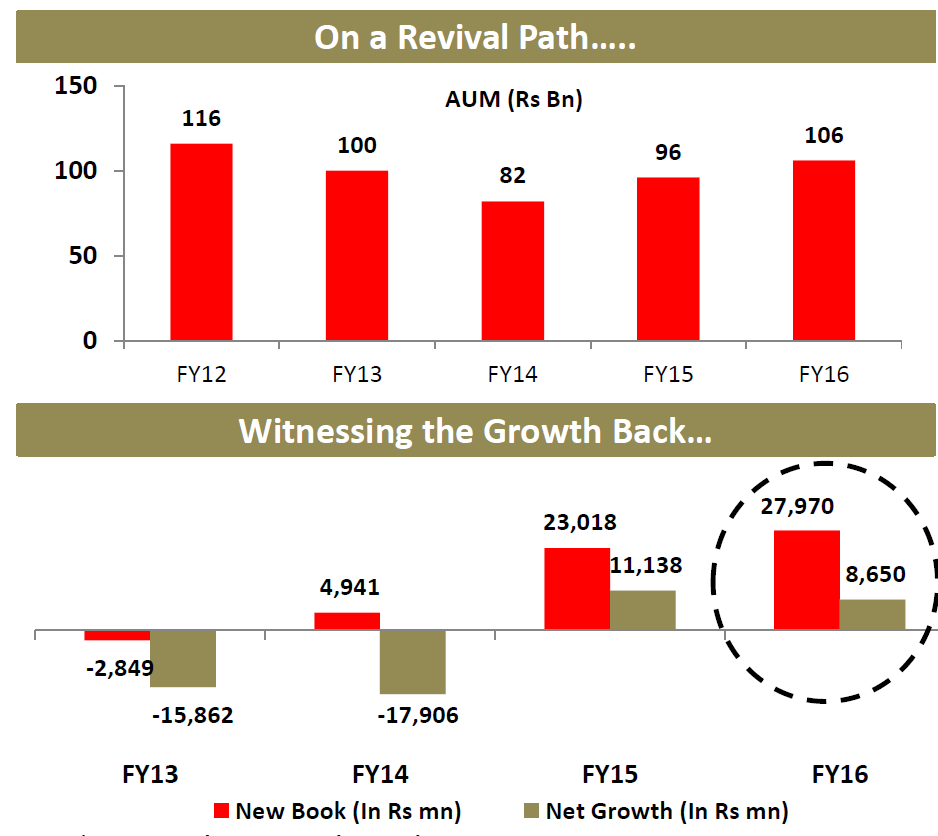

Check any of their quarterly results, they talk about how they have recovered from FY13’s troubles in great detail

Agree that principal is not paid back monthly. However, in gold loan business collateral is in lender’s possession, unlike vehicle, home or land. It is easy to liquidate and recover the due.Gold falling more than 20% within 3 months in Rupee term and continue staying low is highly unlikely. If so it could be like black swan event. It is all about risk-reward when it comes to investing.

Trailing PB value of 2x and 3% div yield and single digit FY17 earling multiple, you can’t get risk free asset.

Also, people pledging jewelry don’t just look at as financial asset or commodity. It has some emotional attachment, hence most of the small borrowers likely to get it back.

The liquidity of gold isn’t straight forward. There is a cost to auctioning and you lose 5-10% value. There is also a cost to holding gold assets, they had a 20 crore robbery recently as well.

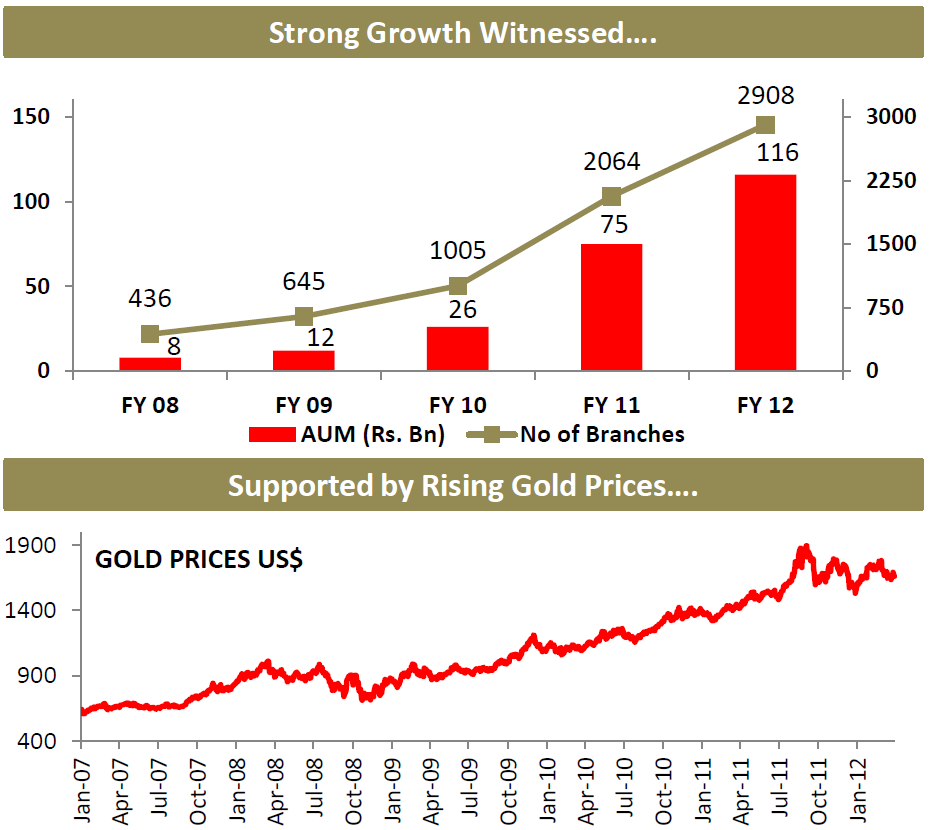

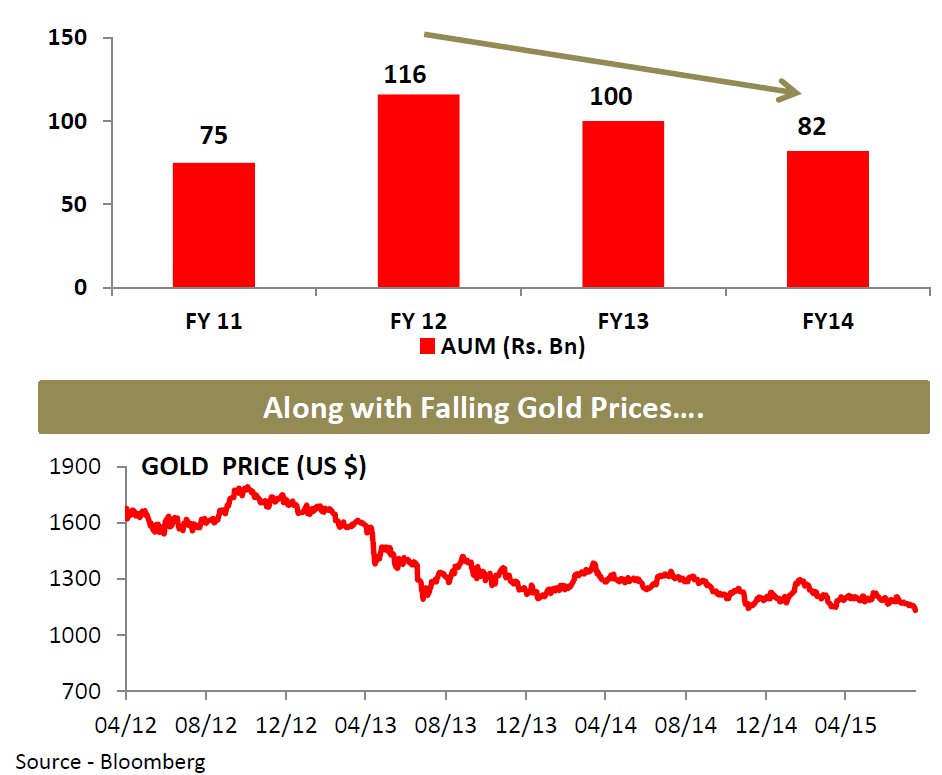

Point being, that even a 10% drop in gold prices will have a disproportionate impact on demand and NPAs. Actually if you plot the company’s performance and share price against gold price, it is a beautifully correlated chart

The gold price and stock price are correlated because the mkt behaves so. Are the earnings, the annual dividend - go up and down as per the gold price. What was the annual dividend 4 years back at same gold price and what is the dividend today?

I don’t want to do your homework for you, but here are a few charts from their quarterly presentation. Their AUM and profitability is 100% correlated to gold prices. The market is being very rational in reflecting that in the share price. This should trade at a discount to traditional lenders. And at 2x P/BV there is enough MoS. At 3x there isn’t.

Since collateral is auctioned when borrowers default , Manappuram profit is hit if gold prices drop sharply. Even then, looking the auction numbers, amount of gold auctioned, amount recovered and amount of write-offs it looks like a good number of people pay off their loans even if it is underwater (i.e. value of collateral is lower than amount owed). This may be due to the sentimental value, making charges etc. So there is some truth behind the sentimental value which acts as an additional collateral.

Manappuram share price has been correlated with gold prices in the past but will it be in future? Manappuram is a lender and not a gold miner or jeweler so to me the correlation is not that straightforward. How will you explain price jump from 20 to 70 in last 6-8 months when gold prices did not move to the same extent?

I think Manappuram profit is correlated with volatility in gold prices rather than the actual price itself. Gold has been volatile in last 4-5 years but that was largely because of unprecedented easing by central banks of developed world.

Here is a long term chart of gold from 1975-76 to Nov 2016.

Please note that the Y axis is logarithmic scale

.

Gold is trading right at long term trend line (log linear regression line). The drop in 2012-2014 was due to sharp rally in preceding 10 years. I am not trying to predict gold prices here but trying to see how much volatile gold prices can get from here on.

In the long run share price is always correlated with EPS and not price of collateral.

Yeah, you just made my point. EPS is correlated to gold price and share price is of course correlated to EPS. So gold price volatility will create volatility here.

Unlike Micro finance which gets weekly or monthly repayments of principal, this is a model that is effectively a perpetual loan unless there is sentimental value based repayment.

Manappuram shareprice is going down drastically since 8th Nov (Demonetisation). Is it bottomed out? or Are we expecting further fall (if FII pulls due to recent FED news)?

Please share your views for short-term (1-2 months) and Midterm (1-2 years)?

The price drop is not just due to demonetisation but also due to drop in gold prices. Manappuram has been saying that now their operations are completely delinked to the gold price. I guess the Dec quarterly results will tell to what extent that is true. Demonetisation has affected rural areas and the bottom of the pyramid the most. This is also the target customer base of Manappuram. This combined with the fact that Manappuram branches may not be getting adequate cash to disburse new loans, so they might be disbursing via collections. So this is definitely affecting the disbursals. I think the market has fairly factored in all these risks & developments. We need to wait for Q3 & Q4 results to see if Manappuram can get back to the growth rate of pre-demonetisation.

Thanks for your response. Gold Price was reduced considerably from 52 week high. Are we seeing this to rebound to start moving upside in near future? What are drivers?

I won’t know if the gold price will go up or down. I wouldn’t want to invest in a company whose fortunes are linked to any commodity. At this moment I want to believe the management when they say operations are de-linked from gold price. If Q3 and Q4 results suggest that it is not the case, then I will exit this investment.

They sanction loan on Price of Gold . The current LTV is 60% -70 % I believe.

So a basic calculation would show than any decrease in price of gold would lower the sanction amount of loan,thus lower the revenue.

In short term I see revenue linked with Gold price. In long term they are targeting to have 50 % business from Non - Gold Business (based on rough calculation I have done in past ,Current share of non gold business might be between 15 - 20 % ). And based on the current execution,I think they can achieve this target.With this they might isolate at-least half of their business from gold price.

Disclosure - Invested at 30 Exited at 95

I might be interested again to enter this counter based on the future execution and valuations.