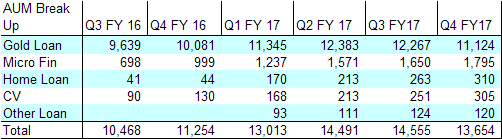

What do you mean by 40-50% CAGR in growth, the relevant number for growth here is AUM in tons of gold since other businesses are marginal (Housing/CV) or face their own challenges (MFI).

AUM in tons of gold has grown by 20% this year but the 3 year CAGR as well as management guidance going forward is 10%. So I dont know where is your number of growth driver coming from.

And please be aware of the fact that RBI at any point of time can since there is an onward lending cap of 10% for MFI (small ticket, poor people without collateral) then why should gold loan companies be allowed to get spreads of 15% (small ticket, poor people with collateral). And as someone mentioned that gold loan companies is just 1% of banking assets, RBI wont have any problem if this busines model gets completely disrupted. So there is a question on both growth as well as profitability going forward which has an effect on valuations. I am not saying that this is a cheap or expensive valuation but please dont extrapolate just one year performance and think this is going to continue for ever.

Well, price action reflects market’s worry on several fronts. the main biz of gold loan is growing @10% cagr for the last few years. High RoE and low gold loan growth should result in capital allocation to other businesses and dividend which is happening. The key question is are they adding shareholder value?

Well, it looks like their biggest diversification in the form of MFI has bombed. It could recover but not before applying breaks on growth engine in the medium term. Before Q3-FY17 they were bullish on growing MFI biz now they want to focus on secure lending in priority of Gold>Home>CV>MSME. Except MFI, others are small enough to contribute to any meaningful AUM growth. I don’t think big investors are worried about MFI as such but the biggest worry is slow AUM growth in the short term when other NBFCs/HFCs are growing at 30-50%. Promoter’s interview suggested 20-25% cagr in loan but the cash cow gold loan is expected to grow @10%.

In long term, Manappuram doesn’t face competition from Banks etc but change in consumer behaviour. IMO, Gold loan is largely a distressed MFI loan biz. A distressed villager will try to secure a loan first and sort out issues rather than sell gold holdings as a first response during financial hardships. The question keeps coming to my mind ‘will repeated loan waivers,Kisan credit and proliferation of Mudra loans etc will reduce general stress level resulting in reduced potential for gold loan companies?’

We believe manappuram story looks good in mid/long-term - decent growth, good management, undervalued etc. Wondering why insiders are selling continuously if stock expected to run anytime soon. Are they know about the business and outlook which is unknown to us currently?

It beats me on why home loan cos demand such high valuation…From just one

player 35 yrs back, it has become like 100+ players now. What is the moat

for each company and there is zero entry barrier…

Manappuram has a large customer base spanning around 3.5 million. VP Nandakumar, in his latest interview has mentioned that, company is planning to cross sell affordable housing to those existing customers. Can’t we consider the above itself as a moat for the company against the other established Housing Finance players? Why I feel so is that, Manappuram’s customers (gold loan, MFI) would mostly likely be having an yearly income of less than Rs. 6 lakhs. As I understand, maximum subsidy (6.5%) under the affordable housing scheme is offered to those whose annual income less than 6 lakh rupees (EWS/LIG category). With 50 million houses as the target, I think, the above category of customers are likely to be the main beneficiaries of the affordable housing program. I do not think that, other established HFC’s have many customers with less than Rs. 6 lakhs of annual income

The reason why home loan companies are getting a much higher valuation is probably the same reason why any company would get higher valuation- Predictability and Stability of earnings, besides lower exposure to regulatory risks. Housing loans are least exposed to regulatory risks.

Every government that rules this country will want increase in housing loans as much as possible and to that extent the housing loan rules will also be attractive as no regulator (there is nothing called an independent regulator BTW)/ government would want to restrict housing loans.

Housing prices have been steady for a long period of time and hence the NPA shocks are substantially lower, resulting in more predictable earnings. Also, home loans repayments are the first priority for majority of families in India and hence customers will default in home loan payments only as a last resort. All said and done, housing loans are secured loans. However, it is critical to note that gold loans, business loans and vehicle loans are also secured loans. Then why don’t they enjoy the same discounting as Home Loans? One critical reason is the volatility of the asset class which is used as a security besides the probable order of customer defaults among asset classes in case of a stress scenario.

Also, the market size has increased considerably with the present dispensation’s focus on housing for all. However, the proliferation of home loan players means that the underwriting standards may be lax. If there is steep fall in home prices, NPAs may buildup rapidly. The market is not discounting for any such black swan events, Enjoy the party while the music lasts!! Hope this clarifies.

Just to add on … Not all housing finance companies are enjoying the same valuations … Companies like Can fin homes which cater mainly to salaried class and have consistently recorded Net NPA of 0 and Gross NPA of less than 1% , growth of 25% plus over last few years and healthy return ratios and trading at a premium…

Same is not the case with lets say a PNB housing which got listed in November last year… Many differences exist with respect to the above points i mentioned and the difference is clear in the valuations …And PNB is not a bad housing finance by any standards… its growing at 40% and doesnt have “bad” parameters to put it that way … just that there are some differences and these are visible in the valuations …

Housing finance in general is not trading cheap, but you cant take the shots on a complete sector as a whole. You still need to pick your bets and market is giving premium valuations only to the ones that deserve it… (correction can happen in near future, but if it happens then it will happen for all alike)…

So how MF or any one else goes around in this game of housing finance will be closely looked at…if they do poorly, it will show in the valuation…

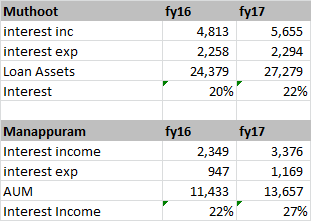

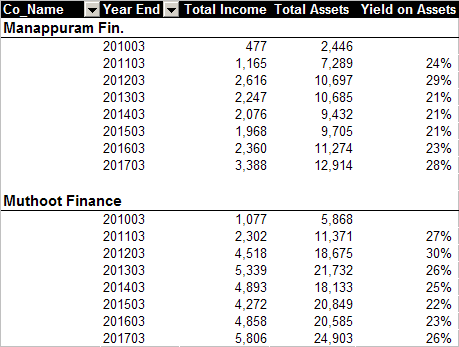

Please have a look at this. What is the reason for such high interest yield for Manappuram? Yield as per income statement is at 26% in FY17; which is higher than 24% it claims for gold loans and despite the fact that 20% of the loan book is of slight lower yielding housing finance and vehicles.

Also the increase in interest yields and thus income (without corresponding increase in interest expense is wierd) and explains such a dramatic jump in net income for the Company in FY17.

If Muthoot being market leader is lending at 21 odd percent, what are the chances for Manappuram to continue with 26% kind of average yields.

Have you considered consolidated numbers for Muthoot? Here are my numbers.

Source: Capitaline

Manappurum numbers are higher than Muthoot as you pointed out but not too high. However, in 2012-14 period, Manappurum suffered larger yield erosion than Muthoot.

Also for Manapprum, less than 1% of assets are low yielding not 20% as you mentioned.

yield of 25-26% secured by such a liquid collateral and with haircut!! dont you find it kind of a risk with increasing consumer finance, sfbs and mfis. This might pose risk to such high interest rates.

Second one is on increase in NIMs for Manna. What is the reason for such a significant increase in interest income. Stand alone (not consol to keep focus on gold and avoid mfi) interest income increased from 2,200 cr to 3,000 cr (+36% yoy) while interest cost just went up by 100 cr to 1,000 cr (+13% yoy) and gold aum increased by just 20% to 13.7kcrores.

I understand they shortened the tenor, resulting in higher disbursals… but this should be the primary reason for increasing yields…

Yields are high because ticket size is small. It takes lot of administrative expenses to originate and collect a small loan. All these costs are built into higher yields. MFIs have the same issue.

This is driven by growth in AUM and yields,

Interest rates have been generally going down in last 2 -3 years so many lenders especially high interest lenders have seen lower borrowing costs.

Beginning 2014, Manappuram’s AUM has started growing again while its fixed costs have largely remained the same. This has resulted in net profit surging in last 2 years.

Manappuram’s customers use gold as a savings account. These are people whose income fluctuates so they park extra income during good times in gold. When income drops, they try to first borrow against the gold instead of selling gold due to emotional attachment. If their income does not go back up and they are not even able to make margin on the loan, lender will auction the gold. I think they wouldn’t mind the gold being auctioned because they would have sold that anyway. this is the reason there was a lot of auction during Q4 of FY17 when many borrowers were not able to put up the margin on the loan.

Short tenure of loans is to prevent build up of accrued interest which is just an unsecured loans which results in losses. this has helped gold loan companies manage their NPAs much more than MFIs

I think, gold loan companies will be best poised to benefit from this, given their affinity with the customers as well as readiness with the infrastructure (collection and purity testing centres, more so in rural areas that account for massive stocks of household gold). It may take some time before this business picks up, but definitely looks promising from a long-term perspective.

It’s good for companies as they understand market and customers better. The monetisation scheme could be additional service option to customers and could structure different types of products like housing loan industry . Thanks