I have a query on their announcement dt Aug’15 “Pending receipt of approval of TNPCB for consent to operate at higher capacity, utilization of the plants has been restricted.”

If their current capacity is under question for Pollution board how come a big capacity planned by the company will not face such risk in future?

Second in their May press release they had plan to invest Rs 100cr for capacity expansion

But in Sep they signed MOU of Rs 500cr investment which includes power plant as well

The company has informed stock exchange the following

Manali Petrochemicals Ltd has informed BSE that the production at both the Plants of the Company remains affected since December 02, 2015 due to flooding and the resultant power disruptions. The plant operations are expected to recommence shortly in a phased manner subject to resumption of normalcy in power supply, material movements, etc. Consequently the overall operations for the quarter and the year will be impacted significantly.

i have been holding Manali from 18 -19 levels, earlier i was very confident of the potential this co. has given the Crude Oil situation and balance sheet of the company. However, given that all that is already been factored in the last few quarters and i dont see any further triggers in the company - as is reflective in the stock price also, is it prudent to book out of this? it has not really made a solid comeback after Chennai floods and positives are discounted already IMO.

I was going through the annual report of manali petro and I have following questions which seems to be left unaddressed by management.

Current capacity of Polyol and PO of manali petro. 1.5 years back they have told to increase capacity by 25000 TPA by march 2016. Which should take the capacity for polyol to 75000 TPA.

6 crore was received as advance from insurance company for flooding, how much more is expected and by when ?

What is the exact role of singapore entity in increasing the sales of company?

Is Manali able to share the import and export split of revenue ?

Can manali share the sale quantity (TPA) of Polyol and PO going forth?

Also I see some red flags in terms of increase in working capital requirements.

Cash and equivalents has decreased by 32% from 94 cr to 65 cr. The main reason could be increase in working capital requirements which is like -

Inventories increased by 23% from 75 to 104 crores.

Trade receivables increased by 12.5% from 80 to 90 crores.

Short term loans jumped by 4 times from 19 to 83 crores. This includes advance to vendors upto 60 crore.

This looks like a deteriorating balance sheet to me.

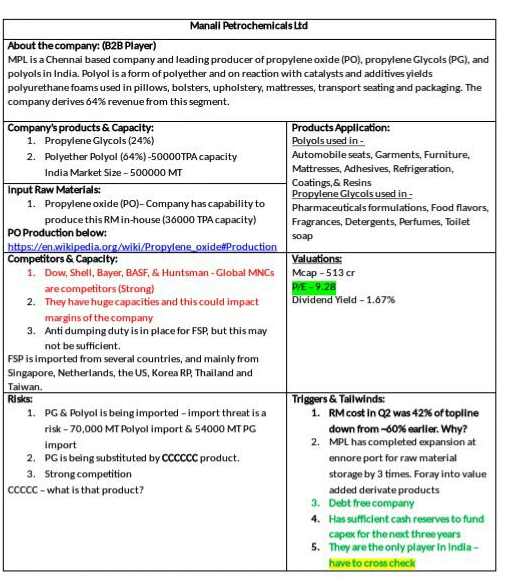

The major risk to company is from biggies like DOW, BASF who are now importing heavy volumes of polyol to India. Is this the reason they finding difficulty to sell ?

The management has told that they are increasing capacity but did not mention the exact capacity. Need to watch the next quarter closely to see.

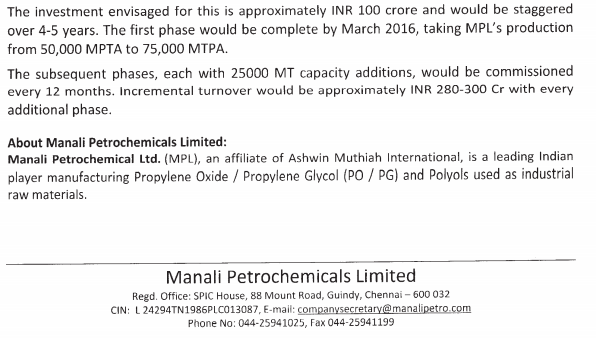

Company will increase capacity of Polyol @ 25,000 TPA and take it to 1,50,000 TPA from present levels of 50,000 TPA within 4 years at incremental cost of 100 Cr. With each step of increase in capacity company will generate additional 280-300 Cr of revenue.

No Idea

The offshore Singapore entity is set up for acquiring a company ovearseas

PO is used as a raw material for Polyol and PG which has fixed capacity of 36,000 TPA. Polyol and PG account for 60-65% and 20-25% respectively of total sales.

Thanks Jigar ! I see you are trying to answer my queries. But my query on point 1 is specific to what the company has delivered w.r.t what they have promised. They promised 25000 TPA addition by march 2016 as 1st phase of the 5 year plan but no mention of that in the report which give me a sense that it is not done. They have told that restrictions are lifted by authorities so now they can expand but yet to see that 1st phase coming up.

Regarding point 3, what kind of acquisition they are looking at ? I am not very clear on the plans.

Regarding point 4, you are assuming that they were able to sell entire amount produced of the maximum capacity but I am not clear how much was produced and how much was sold from the report. I feel a bit of detail is required here.

So the Singapore subsidiary swing in action. Though not much information yet but seems they are firm on the their plans for expansion. 120 crore investment to tap 45 countries as claimed by the news article.

Let’s see how this move turns in favour of Manali. Now some action is expected from top line and capacity of the company. Interest cost is another factor to be watched carefully due to the loan they have incurred which could be between 30-50 crores as per my calculation.

Not expected after they had a lot of good things going for them - Capacity expansion, Notedome aquisition, Anti-dumping duty. Of course, there were some challenges - Oil price rise, Demonetisation, Chennai flood (won insurance claim though).

Not much information available on loss-making subsidiaries. Sold a third of my shares prior to results (call it risk management).

Another bad quater. Inspite of acquisition and burning all the cash, the company is not able to improve its sales. Expenses are increasing though. The story is deteriorating in my view. The increased supply of imported Polyol from biggies is eating away margins on one end. Notedom is not delevering any meaningful contribution to revenues and profits so far.

Moreover, there is not much information from management about the situation.

Is anyone else tracking this and have any information available

Company : MANALIPETC

meeting of the Board of Directors of the Company is scheduled to be held on 27th September 2017, inter alia to consider proposals for fund raising to meet the funds requirements of the Company.

After one acquisition and using the existing reserves they are looking to raise money for fueling growth. How all this is going to pay off is a thing to watch.

AMCHEM Speciality Chemicals Pvt Ltd, Singapore made 9.04 cr loss in FY17 on the turnover of 69.48 lakhs - Employee Benefits expense (6.23 cr) and Other Operating expense (3.33 cr)

Have to check their financial statements for FY18. What is the purpose of this Singapore subsidiary??

@azadh20

The purpose of Singapore subsidiary is for acquisitions in this segment. However if you check the financials of Notedome which is in page 40 of the MPL-SUBSIIdary-financials.pdf you will find that Notedome actually has a net profit of 31k pounds that means roughly 27lakhs …and they bought this notedome for 120crore rupees.

Seemed like a red flag to me. Let me know your thoughts

another redflag kind of thing is pointed on the rent paid.

Business As usual:

They pointed out in their AR17 that they face significant import from Thailand and Singapore, and it got resolved because government imposed Anti-dumping duty. It seemed that they have good results also but the Notedome is like a concern for me.

Let me know your thoughts, ill be happy if someone can disprove this… it will be a good buying opportunity

According to their Annual report 17 Page 4.

AMCHEM, Singapore continues to explore other

opportunities for acquisition of existing overseas facil

ities to further improve the global presence of MPL. It has

been reported that options for taking up other activities

such as trading, transaction facilitation, business & project

consultancy are also looked at by the subsidiary.

Most of 6.6 Crore is staff salary and “Bonus”. Most probably for the acquisition

rest 3.3 they gave is Professional Fees