maithan is still dealing in traded goods which is not a healthy sign as they should be more focused on the production side. last year they had declared 164 cr of purchase of traded goods and in this q1 result they declared the turnover on it to be 175 cr which is a 11 cr profit or 3 cr every quarter.

if we assume the same turnover for q1 meaning on the 30.88 cr of traded goods bot, it would have been sold at 33.88 cr then the COGS as a percentage of revenue is 47% which is in line with the previous quarter and yoy quarter. the power and fuel expenses too at 22% is a bit higher than last quarter at 20% but same as yoy.

so maithan revenue from core operations was flat qoq and up 5% yoy. the inventory decrease is a healthy sign as maithan has been struggling to improve its inventory turnover ratio but it could be just due to frequent purchase and sale of traded goods so we need to watch out for it. overall a flat result i would say.

Good Annual report from a Commodity company.

Maithan Alloys, one of the lowest-cost ferro-alloys manufactures in the world, enjoying an EBITDA margin of 20.91% (FY2017-18) and ROCE (operation) of 70%. This is also helping the Company

to post ROCE (operations) in excess of 50%.

Cons: Top line growth is limited until the green field expansion take place in 30 months time frame,

Maithan A.R.pdf (1.7 MB)

Disc: Hold

MaithanAlloys-Presentation.pptx (528.1 KB)

My presentation on Maithan Alloys…

Disc: Vested interest and biased views

Yes you are correct but never know about the commodity prices after two-three years.

Any other differentiation besides being the lowest cost producer?

If that is so,would it not remain the same in the industry ,even if the commodity prices surge or fall.

Whar are the options companies have besides Maithan alloys?

Results kind of flat (less than 10% sales growth and 5% Profit growth). The commentary for the future is positive.

Whole press release can be seen at

https://www.bseindia.com/xml-data/corpfiling/AttachLive/a79269f0-50e4-4386-a296-1ac89c90904e.pdf

disc: tracking position and I do not understand cyclical much.

Positives

PE of 4.87, PEG of 0.1, ROCE & ROE > 40% makes a great value buy.

Negatives

Profit growth YoY of 2%

Need to see this company is service provider not as commodity player. They don’t own raw material nor they get in to long term contracts. Spot buying and processing and supply at spot rates.

The alloys are very insignificant portion of whole steel manufacturing part and these guys are well known for quality. Question for you: Will you deploy a cheap variant of electric switch in a crore rupee home? The saving is insignificant but the loss can be huge… Hope this helps, happy investing

Thanks. This is s a fantastic attribute. This makes the company a standout.

MCap: 1650

P/E: 5.53

ROE: 40

ROCE: 48

ROIC: 72

Profit growth 3 years: 78.85

is this a value stock?

Remember - It is a business catering to cyclical end industry - and it is operating at close to 100% capacity that’s why these numbers look high. You should not look at the top of cycle to make a conclusion imho.

They have expansion of capacity in the works. But it will be completed only in 2021. But it still seems like a good buy at these prices

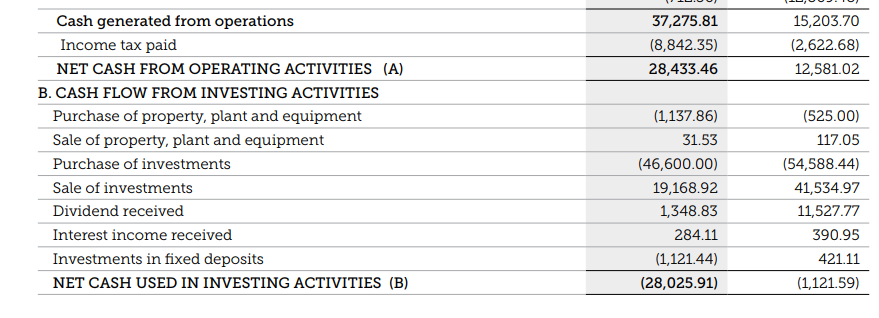

Does anyone know why there is a huge amount of “Purchase of investments” ? Are they buying some assets for the expansion they mentioned in 2021 ?

Price seems to be on a freefall… has hit 52 wk low this week. Upcoming Quarterly results / Budget / General elections might be the cause or any impact of Fundamentals at play ?

market cap of the company is around 1100 cr while the cash on books is roughly 550-600cr. The company maintain it can generate and EBITDA of 15- 17% in the long run. the company has generated net profit of 274 cr in the last 4 quarter TTM and is available at a PE of 4.

the company has an asset light model unlike other companies in similar sector as it has not deployed its capital in captive power plants , neither has it backward integrated in acquiring mines. this i believe is prudent on the part of the management as they are not focusing on just improving margins by some basis points rather they are focusing on maintaining better return rations.

the company claims to be the lowest cost producer of ferro alloys but looking at other companies in the similar sector i fail to understand how.

the company is putting up a plant for ferro chrome with a capex of 275 cr. this i believe will have a peak revenue potential to generate 1000 - 1200 cr at slightly better margins than the other alloys. it is a fungible capacity , in case they are not able to sell it they can switch back to ferro manganese.

plus the company wants to go for inorganic growth with the remaining cash , they are looking into acquisitions.

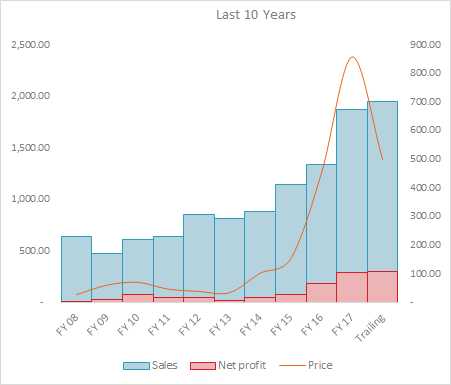

in a fragmented market it becomes very difficult to understand and analyze market shares and how it has been changing for the company. but looking at past performance of the company its safe to assume it has been improving its market share as it volume is definitely growing much faster than the rate of the growth in steel industry. ( steel is growing at a rate of approx 7 %).

the management has decided to not distribute huge dividends as they dont find it tax efficient . also they do a lot of dividend stripping , in fy 17 AR you can see dividend received to be 115 cr , and short term loss to be 114 cr. this i believe is a prudent way of saving taxes as dividend income for companies is non taxable but short term loss can e offset against gain( not sure how this works practically would appreciate if someone explains this in detail). as long as the management is not involving in excessive related party transactions and taking out significant cashflows i dont think there is a reason to worry.

Disc - Invested .

Got to know from that Maithan is a cyclical business, it is running at full capacity (>95%), hence market does not think that it can make more profits with existing capacity, this could be the reason for the fall even though the results were good.

From annual report:

maybe market is waiting for the greenfield expansion to finish?

Disc: Invested at +50% higher levels