The company is in the business of selling vacation ownership.

Business Model:

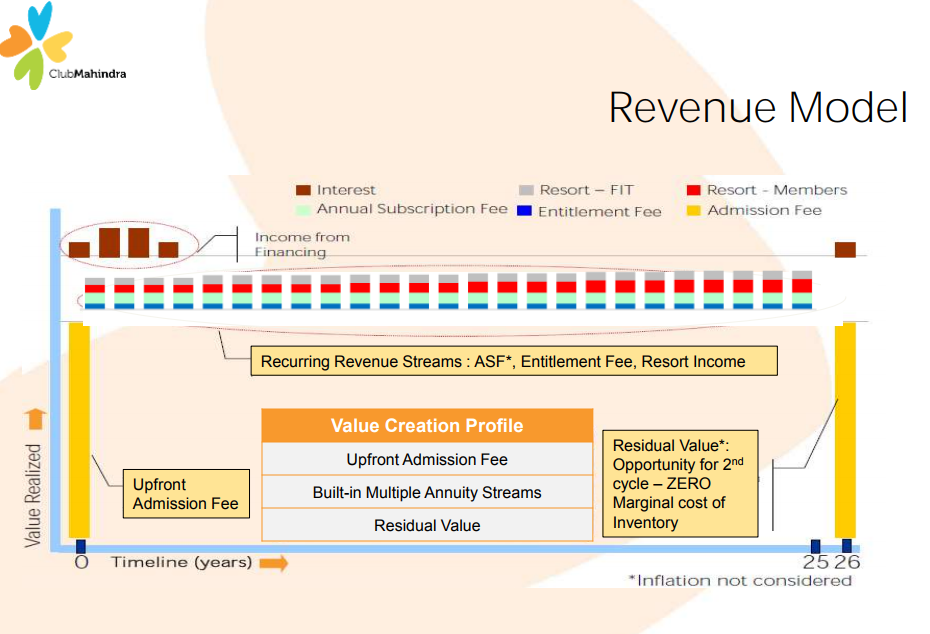

Company collects upfront charges from customers for selling vacation for periods of 10-25 years.The same is recognised as income over the period of vacation. Company even provides an installment option for purchase of vacation ownership.

Annual Subscription fees: Apart from this the company also collects annual subscription fees

Apart from that the company also earns income by selling food and beverages in its resorts

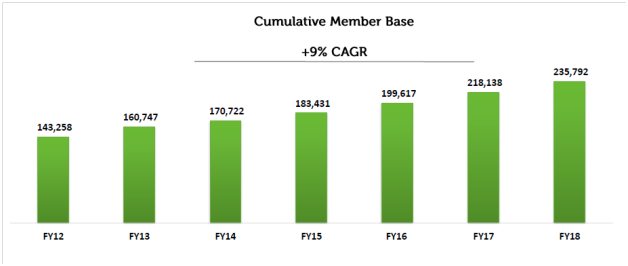

The company has been able to grow number of members from 109884 (2010) to 218138 (2017)

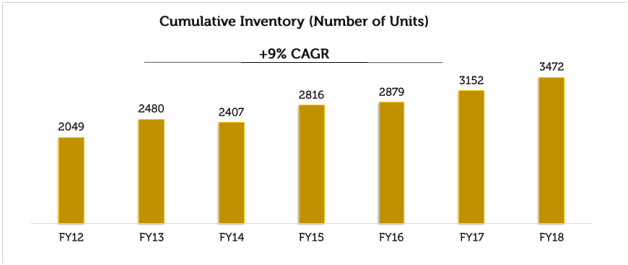

No. of units have grown from 1476 (2010) to 3152 (2017)

3.The company has been able to increase customer as promoter score from 12% (FY 13) to 42% (Dec 16)

My Investment thesis:

Vacation ownership is a discretionary item and as per capita income of the country is growing its expected to get a higher wallet share.

2.Asset light model as the business involves collecting amounts from customers upfront and then building the resorts

Resort diversity and international prescence in sweden, finland and spain

Believe that the company will be able to increase the number of member at 10-12% with 5-6% price hikes from resort income and interest income on installment sales which currently contributes to (22% in 2012) 27% of revenues

Key Risks:

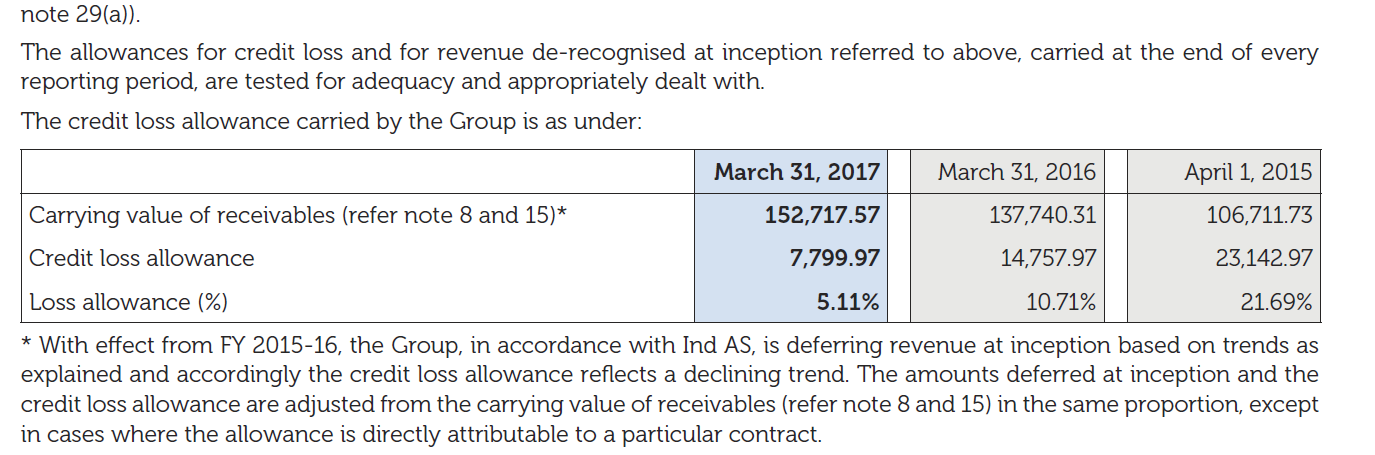

Very high Trade Receivable amount and high provisioning is made on the same as per annual report

It is indeed a consumption story and despite poor quarterly numbers looks to be a good bet. I have come across many people who are exploring this as an option (to become member).

Company collects upwards of 200 cr in maintenance alone from existing members.

Its difficult to get bookings in their resort which is bad for members (like me and others who have shared their experience above). But that is good for company I believe.

With disposable income growing I think they will keep adding members and income will grow at gradual pace.

Can this high trade receivable be attributed to new members opting for EMI for payment of membership ? Generally such emis are for 11 months . Other than that I am unable to figure out receivables as customers have to settle dues when they check out.

Yes it surely discourage members. Infact I myself have asked two prospective customers to not become a member. One was in advance stage of issuing cheque.

But if bookings are not available, that means they are sold out.

But at the same time they are successfully adding members. If someone ask me I say no, may be you will also advise against the same but still they add.

What that results into is non payment of maintenance charges by disgruntled customers who vent out their frustration by delaying maintenance and abusing the back office staff.

So my only point is _ no booking available means they are sold out that’s all

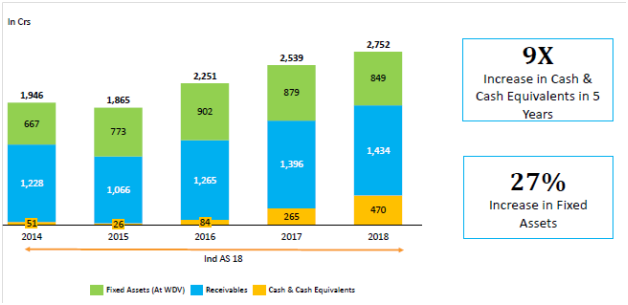

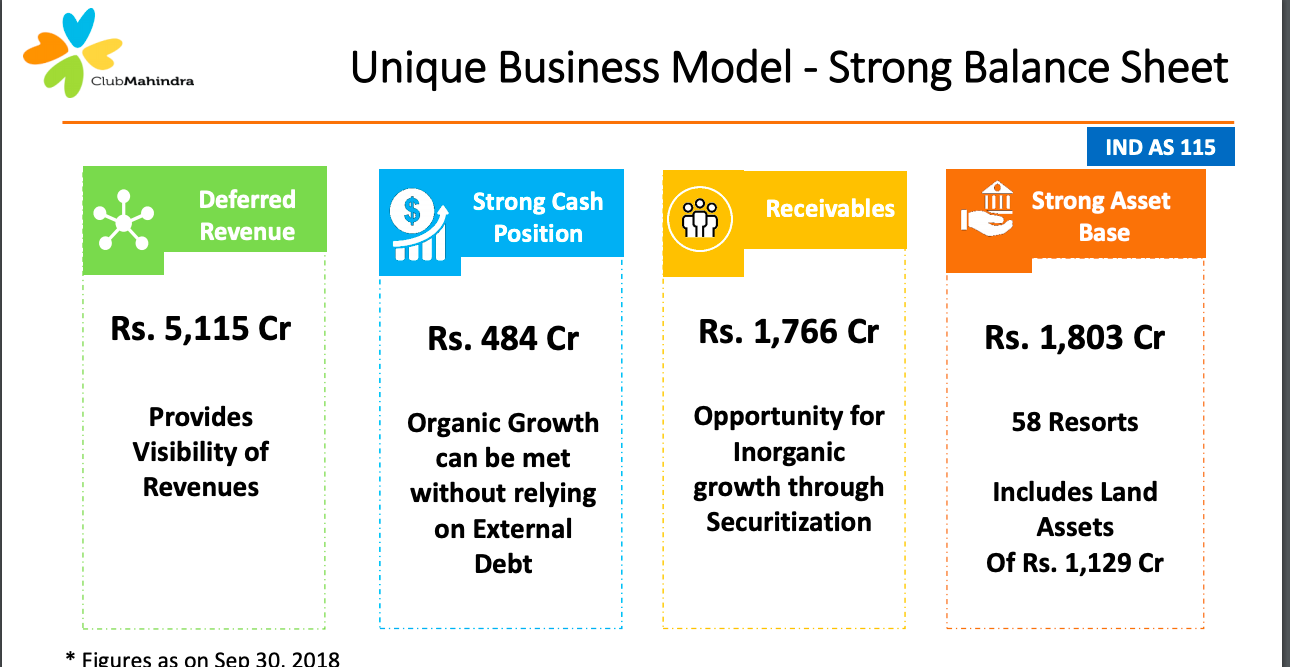

Mahindra Holidays seems to be attractive at current price. They have inventory of 3472 rooms at 55 resorts with no debt (Standalone). In fact they have cash surplus of ~470 Cr as on 31/03/2018 (Standalone)

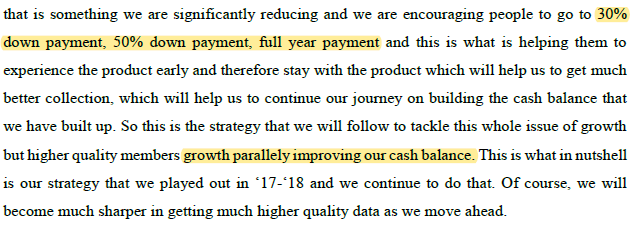

Since last year, they have adopted a strategy to add quality members who are willing to pay higher down payment (30-50% as against 10-15%) and lower tenure EMI’s (36 months vs. 60 months) . This is evident with the increase in cash balance which has gone up from 265 cr in FY17 to 470 cr. in FY18. The idea is that these members have capacity to pay and therefore will also be regular with their EMI and ASF charges. This will also result in lower provisioning in future. Also, they will use the resorts regularly which generate more resort revenue.

This cash balance helps them build more rooms / resorts without taking any debt. Presently they are adding 240 rooms in Goa in 2 phases, 100 rooms in Ashtamudi in 2 phases and 140 rooms in Kandaghat (pending approval). Planned CAPEX for this 480 rooms is approx. Rs.480-500 Cr.

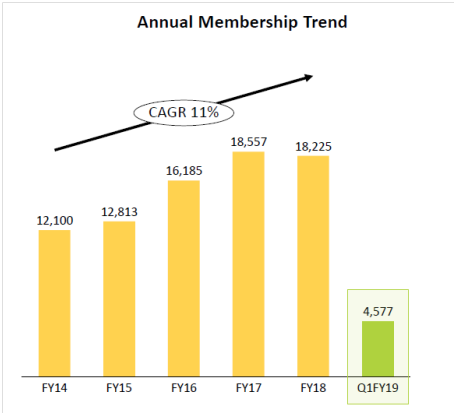

Company has been consistently adding new members. Average additions for last 3 years is ~16500+ members. The important point to note here is the payment mix that has changed where members are paying high down payment.

Last 6 years CAGR for total members is ~9%.

Room inventory has also seen similar increase in CAGR. This ensures that availability of rooms is in line with member additions.

Their occupancy level for last 2 years is ~85% with ARR of ~Rs.4,500 for FY18.

There has been lot of skepticism regarding club mahindra membership as members usually complain about non-availability of rooms. However, numbers clearly tell a different story. I am not a member but have stayed at 4 of their properties and experience has always been phenomenal. It’s a place for family (specially with kids) which offer unique holiday experience through various activities like cultural shows, traditional arts and crafts workshops, coffee, tea plantation tours, beach pool activities, summer camps for children, local culinary experiences etc.

Do you have any reference material to confirm this > “higher down payment (30-50%)”?

Their occupancy level for last 2 years is ~85% with ARR of ~Rs.4,500 for FY18.

Not sure what you will make out of it? This ARR is for 5-7% inventory which they sale in open market.

85% occupancy - 5-7% non-member sale = 75-77% member usages. So at any given year 20-25% members are not able to avail their holidays. Actually what may be happening … 50% members always utilize their all holidays. Rest 50% utilize only ~50% of their holidays. That’ the minus of their business model.

This business is hard to grow beyond 8-9%, if they try to they will land into same situation as it happened between 2004-2009 and spill over of same continued for long. But the environment in which it is operating gives it unique advantage so the cash, and return matrix.

( 1. No competition from timeshare, but Airbnb and likes will give them strong competition.

2. Weak regulatory environment wrt to timeshare ( get away with lower number of rooms vs members)

3. Not easy for any new business to build this kind of inventory quickly. Sterling is not able to provide any competition, so also the market hype which help increase the pie.)

Going forward with new accounting standard reported earning will be suppressed. It is still quoting at high (20+) PE. Some work is required to evaluate it on the basis on cashflow.

Do you have any reference material to confirm this > “higher down payment (30-50%)”?

Q4FY18 concall by the management.

Not sure what you will make out of it? This ARR is for 5-7% inventory which they sale in open market.

Agree. I was pointing more towards high occupancy of 85% which indicates regular demand.

Going forward with new accounting standard reported earning will be suppressed. It is still quoting at high (20+) PE. Some work is required to evaluate it on the basis on cashflow.

This is where I think the opportunity in terms of better price may arise. Change in accounting policy will not impact business fundamentals. Profitability and Operating cash flows will remain same over the tenure of membership. There will be a significant increase in deferred revenue in the balance sheet.

For quick reference:

MHRIL used to account nonrefundable admission fee of 60% as income in the year of sale and balance 40% which is the entitlement fee was deferred over the tenure of the membership (10 or 25 years). From 1st April 2018, AS115 is applicable, where income from vacation ownership contracts need to be recognized over the tenure of membership. Also only incremental costs incurred for obtaining the membership need to be deferred over the tenure of the contract. Other costs are to be charged to profit and loss account for the period.

This means that revenue will be suppressed, only part of the expenses (like commission, incentives, discounts, offers, directly linked to the acquisition of the member.) will be deferred and hence reported profitability will be lower.

I honestly don’t think Airbnb and likes will have any impact on such businesses. The customer base is completely different given the different experiences it offers.

This means that revenue will be suppressed, only part of the expenses (like commission, incentives, discounts, offers, directly linked to the acquisition of the member.) will be deferred and hence reported profitability will be lower.

Will it lead to batter price in market?

I honestly don’t think Airbnb and likes will have any impact on such businesses. The customer base is completely different given the different experiences it offers.

CM experience comes at a cost. If that cost is much higher then what other alternatives are then certainly there would be growth or membership price pressure or both.

In fact they have cash surplus of ~470 Cr as on 31/03/2018 (Standalone)

Challenge is how to value cash, this case is deferred room inventory+ retained profit. How it is divided between these two? First part allows to collect ASF + In resort expenditures. Second need to be invested to grow business.

Can some one point me to some references on luxury vacation resorts, business hotel development cost, acquisition deals (Only where all rooms are primarily self owned)? ( equivalent to Mahindra Holidays std)

One from Mahindra Holidays :

2012:: 106-room 5-star property, The Retreat, By Zuri, in Goa for Rs 112 crore.

…~…~…~…~…~…~.

2016:: Opened in 2012 within Weikfield IT Park, Hyatt Regency Pune is a five-star property with 222 rooms and 102 fully serviced luxury apartments. It will be SAMHI’s third property in Pune, after two Formule 1 branded hotels.

…~…~…~…~…~…~.

Yes, and I did try to raise this during their AGM. Answer simply was they like the business model ( clients money funding the capex ) and belive it will deliver.

Interesting, even i noticed this in PPFAS detailed portfolio report.

Scuttlebutt - I recently stayed in CM Cherai beach with family and had awesome experience. They have Courteous and friendly staff, well maintained premises, engaging customers with events, etc. My employer has tie-up with CM where employees can avail 3 days stay and am sure many corporates provide this benefitsto ees - this will be one constant source of demand IMO.

Will be good to see some valuation from VP members on this stock.

This problem is still there. Cumulative Rooms = 3472, that means around 1.80 lakh weeks while customer base is 2.35 lakh. I have not reduced 25% from 1.80 lakh weeks to take care of the fact that only 75% occupancy is members only (rest is vacant nights + sales promotions + outside sales) as they will take care of people upgrading and staying for a lesser number of nights.

I do not think there are many people who miss their week and still pay maintaince charges. One might look at OLX and Quickr for ads on club mahindra membership where such people sell their nights to recover such charges atleast.

I think this is a time bomb in the making. Bad customer experience, booking problems etc will be future concerns.

On Mathematical terms you are right that no of rooms seem to be far less than required . But what explain occupancy rates across quarter < 80% .

Gym, Vacation membership etc capacity are based on % certain number of people of who will avail the benefits . Not all member avail those benefits and hence occupancy rates are lower .

Lets say what you say is true that say 10 years down line no one will renew their membership … Still the company has created a asset base of 3500+ luxury resort rooms in exotic location with no debt and it is building capacity very fast . + it has some great international rooms capacity also …

The market cap of this company is 2800 cr and lets say “budget” hotel with 4000 rooms lemon tree with debt on books is valued at 5000 + crores .

Now you need to take call if you need to be hospitality industry which is better bet …

Second test ability of above asset to generate cash flow EV/ OCF is around 8.66 which is very reasonable .

Post that Trust god that market will too value the stock the way you do

Any way I use my own valuation software which is giving following range of value …

Absolute Pessimism in Bear market : Rs 160- Rs 240 : this is BUY ZONE for me

High level Optimism in Bull Market > Rs 1000 … This is sell zone for me …

Rest is Hold zone … or No action zone …