That’s my understanding initially but on a second thought I am just wondering if there are buyers for those many shares in open market? That’s almost 7.2% of total outstanding shares. It might be possible that some FIIs/MF might have bought from open market. I am wondering why BGAP just offloaded without properly getting the buyers.

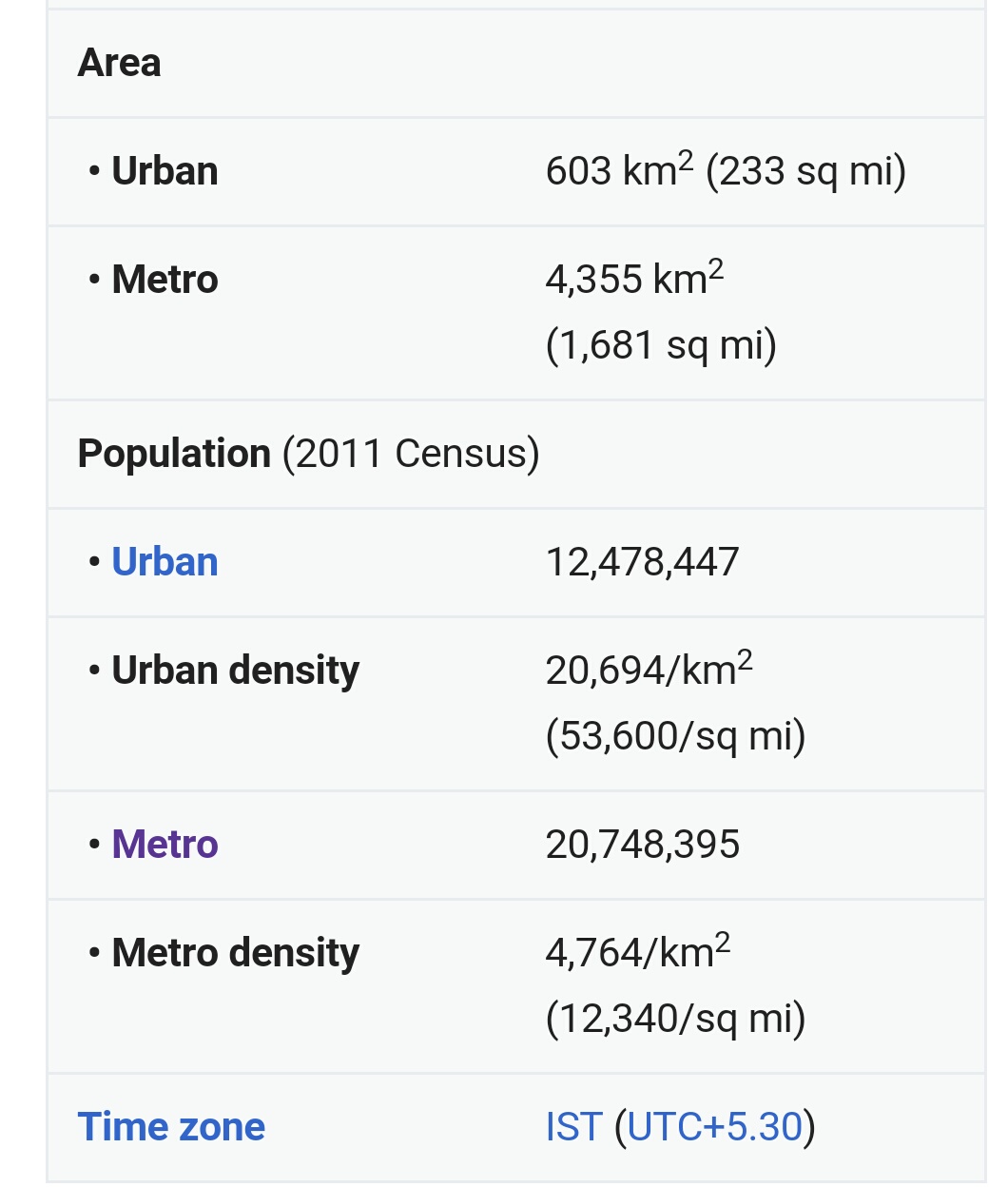

Dear @AKGupta Ji, Many thanks for presenting your queries. I’ll try to answer them to the best of my ability. Per the 2011 Census population of the Mumbai Metropolitan Region is 20748395.

I’ve considered a population of 3 crores in my calculation, implying a population growth of 50% over 7 years.

[Uploading…

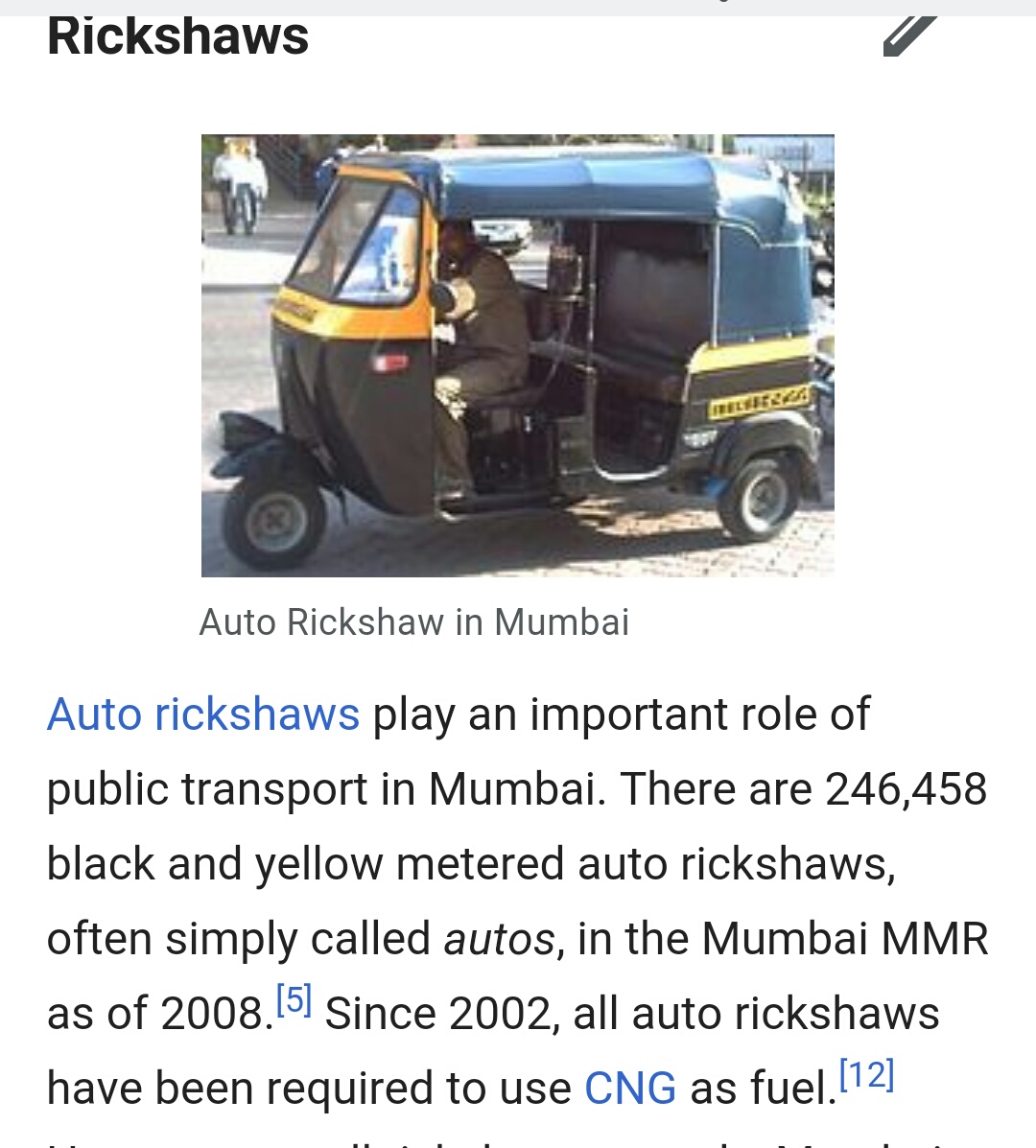

Now, the number of autos-

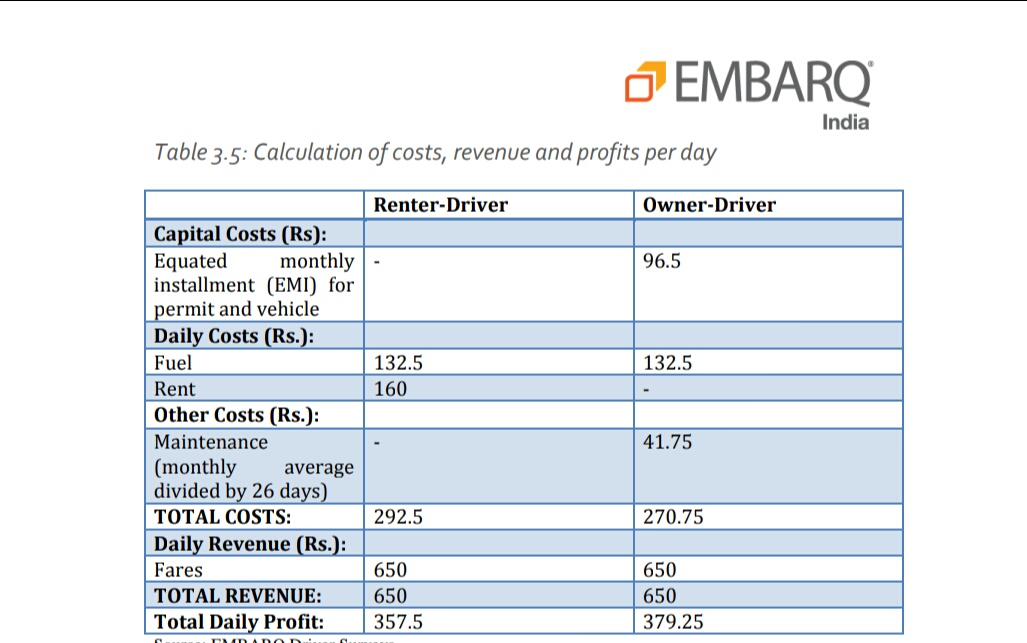

The per day fuel expenditure for autos-

The attached screenshot is from a 2012 report. I’m assuming a 100% increase in fuel consumption.

The numbers I’ve considered are much higher than actual estimates.

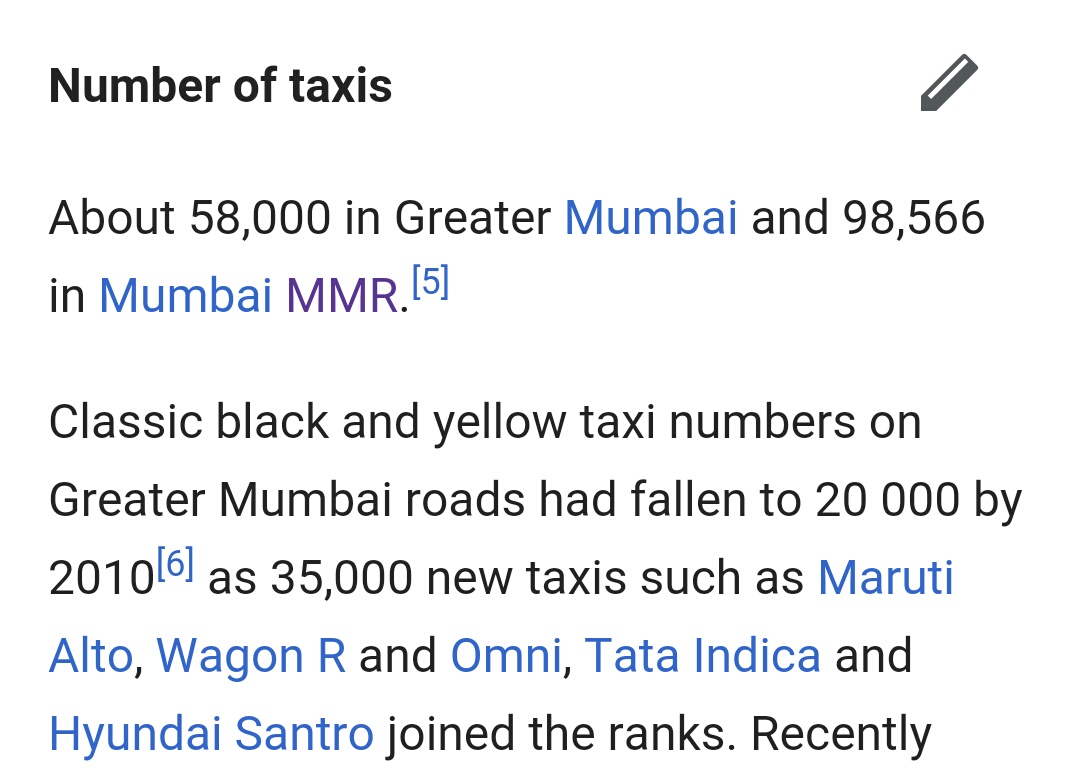

The number of taxis-

Yet again, I’ve considered a 100% rise in the number of taxis.

And, the information on fuel spending for taxis was anecdotal. But, I’m fairly certain that the actual spending is in this range.

Also, I’ve made an assumption that 80% taxis switch to CNG, which is unlikely.

And, sure, the company will bid for the opportunity to establish piped gas services in various cities. But, most cities in the top 25 list have companies that are joint ventures between much larger companies. It wouldn’t be wrong to expect bidding to be extremely competitive for lucrative circuits.

Listt of cities and gas suppliers:

1)Mumbai- Mahanagar Gas

2)Delhi- Indraprastha Gas

3)Hyderabad - Bhagyanagar Gas( GAIL and HPCL joint venture)

4)Ahmedabad- Gujarat Gas

Adani Gas

5)Chennai- BPCL

6)Surat- Gujarat Gas

7)Pune - MNGL

8)Lucknow-Green Gas ( GAIL and IOC joint venture)

9)Kanpur- CUPGL- Central UP Gas limited( Gail and BPCL joint venture)

10)Indore- Avantika Gas Limited (GAIL and HPCL joint venture)

11)Thane-MGL

12)Pimpri Chinchwad- MNGL

13)Vadodara- Vadodara Gas Limited ( GAIL and VMC joint venture)

14)Ghaziabad-IGL

15)Agra- Green Gas

7 Likes

Shell has a strategic program of $30B disinvestment out of which MGL stake is just $100mm+.

Don’t think Shell will wait for a buyer as they don’t seem to care about the price.(That’s why the discount sale!).

Perhaps this serves as an important lesson on how minority investors can get screwed by the major ones!

2 Likes

Thanks for sharing but I’ve my doubts about this calculation.

Also, if MGL achieves even half of what you have calculated, it’ll double it’s topline from current run rate. How fast it is able to do it will of course matter.

Could you please share your concerns about the calculation?

It’ll help me improve the estimates.

And, MGL will definitely bid for rights in various cities. But, GAIL and BPCL have formed joint ventures in multiple cities and will definitely be very tough competitors.

And, you’ve mentioned that I haven’t considered Raigad in my calculations. But, Raigad is a part of the Mumbai Metropolitan Region. Hence, separate assessment would be superfluous.

1 Like

is there any calculation done on the Industrial segment as @AKGupta has pointed out? if so please share that too

1 Like

I tried to search for industrial unit gas consumption in Maharashtra. But, couldn’t find it.

But, I found numbers for Gujarat. After making some adjustments we can arrive at a reasonable estimate.

Gujarat Gas supplies gas to industrial units in Gujarat.

Around 3000 industrial consumers are served.

The prices charged vary between Rs.25-28 per standard cubic meter. The prices are dynamic and amended depending on liquefied natural gas prices.

Gujarat Gas supplies a total of 4.3 million metric standard cubic meter per day to industrial units in various parts of Gujarat.

I’ll consider the higher price of Rs 28 per standard cubic meter for our calculations.

Total=4.3 million metric standard cubic meter per day × Rs 30 per standard cubic metre × 30 days × 12 months = Rs 4334 crores

Now,frankly I’m not aware of the total industrial units in Maharashtra. But, I’ll add 50% to the above figure to account for Maharashtra’s higher GDP.

Total= Rs 6500 crores.

And, this number is for the entire state. It’d be unreasonable to expect MGL to have a monopoly in the entire state. There are several other players who’ll keenly contest the business opportunity.

I’ve tried my best to ensure my calculations are correct.

If I’ve erred my apologies.

4 Likes

So finally where r your calculations and what is your assessment post this exercise on the stock

Hi @shreys

Sizing up the market is a crucial ingredient to a good investment process in my view and its great that you have an estimate. More often than not companies run out of new customers for their products and services so its important to have a sense of how large the customer base can possibly get before that happens. I like your thought process - keep it up!

Best

Bheeshma

3 Likes

Dear @bheeshma Sir,

My heartfelt gratitude for your encouraging comments. It means a lot to me.

Yet again, many thanks.

1 Like

@atul1082 Ji,

My apologies for the late reply.

I performed some more calculations and tried to arrive at a conclusion.

Population of Maharashtra: 12 crores

Assuming all residents use natural gas for cooking-

Per capita gas consumption- 2.5 Standard Cubic Metre per month

Total Gas consumption per annum- 360 crores Standard Cubic Metre

Tariff per Standard Cubic Metre- Rs 30( Blended average)

Total=Rs 10800 crores

Vehicular Gas Consumption-

Per the latest Economic Survey there are a total of 3.1 crore vehicles in Maharashtra.

Let’s assume a very high 25% migration to CNG.

That would mean around 77.5 lakh vehicles.

Yet again, assuming an average spending of Rs.4000 per month on fuel.

Some vehicles like buses, autos will spend much more while some private vehicles will spend a lot lesser.

Total spending- Rs 37200 crores

Industrial gas supply - Around Rs. 8000 crores

The total maximum potential for spending on CNG is possibly around Rs. 56000 crores.

The actual spending will be much lower because not all will migrate to piped gas for cooking purpose. But, I’ve tried to estimate numbers in the ideal case. We can then make requisite adjustments.

It’s amply clear that there’ll be a massive opportunity for CNG over the next few years.

But, I feel there’ll be quite a few big players involved.

For the entire state, I’m inclined to believe at least 6-7 companies will be major suppliers. There may be even more companies involved.

I performed a comparison with the residential gas utility companies in the US. Around 40% of the total revenue of the top 8 companies is generated by the first 2 companies.

Revenue of the 2 largest gas supplier- Around 20000 crores( at the most).

The rest, around 30000 crores will be generated by 5-6 companies.

Now, I don’t know which company will emerge at the top of this business.

The potential for growth, in theory is good.

But everything depends on execution.

It’ll help if we regularly monitor the progress.

The numbers I’ve considered are the ideal case.

In reality, I feel numbers will be much lower.

Please excuse if there’s any error.

2 Likes

Thanks for your reply.mgl is currently in and around Mumbai.Since there is

licensing area wise,a new company can not enter and compete with MGL under

current regulations.Same is true for IGl b ncr.Inaddiion, MGL has gas

dispensing stations at v important locations with laid down u/g pipeline

which no other company can replicate within economies of scale and

therefore MGL will grow and capture business as Ong as conversions in it’s

area, new license winning and also converting housing to png rather than

LPG use TC etc

1 Like

Certainly. There’s a tremendous opportunity for growth. But, in my humble opinion, it’s important that the company expand to other geographical areas as well.

And, in my limited understanding, it’ll be an uphill task.

In the latest PNGRB release, the following regions in Maharashtra have been selected for the City Gas Distribution project.

Ahmednagar

Aurangabad

Dhule

Nashik

Latur

Osmanabad

Sangli

Satara

Sindhudurg

Aurangabad is in close proximity of the East West pipeline. East West pipeline is owned by RGTIL- subsidiary of Reliance Industries

In 2008, Reliance Gas had expressed interest in operating a city gas distribution network.

Nashik is in close proximity of two major pipelines- a)Dahej Uran Dabhol Panvel pipeline which is owned by GAIL.

b) East West pipeline- RGTIL

If I’m not mistaken both of the above pipelines are common carriers - 25% of the capacity should be for third party transportation.

Latur and Osmanabad are located close to the East West pipeline.

Sangli and Satara are close to the Dahej Uran Dabhol Panvel pipeline which is owned by GAIL.

Sindhudurg is in close proximity of the Dabhol Bangalore pipeline which is owned by GAIL.

We can only wait and watch which regions MGL bids for.

2 Likes

Just because reliance gas or gail has a pipleline in proxmity to a city do they get a preference in allotment of that city?

I’m not aware of such a rule.

But, supply of gas could be a problem for other companies if pipeline owners refuse to accommodate them.

The common carrier capacity is 25%.

Beyond that they’re not obligated to transport gas.

In the situation of pipeline owners refusing transportation the resolution could be protracted.

There r cross holding in these companies.if I remember correctly, Gail holds some stake in MGL and probably hpcl too.Therefore MGL will HV their members on board and any bid, to the best of my knowledge, after discussion and agreement of all stake holders

1 Like

Some observations:

Population should be assumed to be a flow number rather than a static 3 crore number. MMR is one of the most densely populated regions in the country and accounted for 25% of the population of Maharashtra as per this old report.(https://timesofindia.indiatimes.com/city/mumbai/Mumbai-metro-region-has-a-fourth-of-states-population/articleshow/7839699.cms)

When a particular area is attracting so much migrants from other parts of the country, it’ll be safe to assume it’ll continue to do so and this creates an opportunity for MGL as new migrants will obviously need its services. I read another report that new migration is mostly happening in peripheral areas rather than Mumbai where real estate is very pricey. MGL has rights in Thane and Raigad.

Also, any sizing up of opportunity will have to take into account a very large period and assume that population, number of vehicles, number of taxis etc will grow over that period by a certain rate.

We cannot say that population will stop growing once it reaches 3 crores in MMR or the number of taxis or autos will stop growing after it reaches a certain number.

I was reading a lecture by Prof Sanjay Bakshi which explicitly denounced this very aspect of discounting the cash flows which are very far off into the future at a very high rate so that it doesn’t add value to the company (Just like that 9888 crore revenue number). But in reality it does. (I’ll share that article separately also but it’s already there on VP forum under “Good articles to read” thread). Definitely dynamics may change over 10, 20 or 30 years.

But I only wanted to point this out : I won’t assume variable factors like population or number of vehicles on the road to be some constant and then determine value.

That said, I don’t want to overly criticise your approach. It might turn out to be correct and I’d actually hope it turns out to be correct since you’re effectively saying MGL can do 5x current revenue potentially.

That’s a good thing for those of us who are invested !

Cheers

GAIL has a 32.5% stake. It’d be against its own interests to partner with someone else in MGL’s backyard. ~25% is with Shell after stake sale. If both these giants want to play in upcoming areas listed above, they could do that via MGL. Compete in areas where they don’t have proxies. This makes business sense to me. I don’t know what actually will happen.

1 Like

There is an another company named Maharasthra Natural Gas Limited which is a joint venture between GAIL and BPCL. This company supplies gas in Pune and around localities. I think this company will also compete for the distribution rights in Maharasthra. Further one quetion that needs to be answered is that GAIL has holdings mostly all the distribution companies but dont know which company will bid for which city and further does there exist a possibility that Mahanagar may bid against maharsthra gas.

Dear @AKGupta Ji,

My apologies for the delayed response. I completely agree with you that it’s very difficult, if not impossible to accurately project earnings of a company over the long term.

Regarding population growth, I politely disagree with you. There’s only so many people a region can accommodate. The past is seldom an indicator of the future. Just because the past had a massive influx of migrants doesn’t necessarily mean it’ll recur. Quite the contrary.

Usually, when a country’s economy develops it leads to growth of multiple regions of abundant opportunities.

Stimulation of economic activity in various regions of the country will improve the standard of living and also provide employment opportunities to residents. And, this will lead to reduced migration.

Agreed, population and vehicular growth won’t stop. But, to account for the growth I’ve considered very high adoption rates for natural gas.

I’ve considered 100% adoption of natural gas as cooking fuel. Not many countries have completely transitioned to natural gas for cooking. There will always be some who refuse to embrace change. MGL, currently has 9 lakh households as customers for cooking gas. The average Indian household size is 4.45. So, a total of around 40 lakh customers. I’ve considered 3 crore customers in my calculations. 7.5 times the current customer base. So, the population will without an iota of doubt increase. But, the numbers in the calculation are extremely optimistic. The actual adoption rate for CNG will be much lower than assumed in the calculation. Hence, in my humble opinion, lower CNG adoption rate combined with rising population should result in an outcome somewhere close to the projections. I think the same applies for vehicles.

I’m optimistic that CNG consumption will go up but I’ve no clue how long it’ll take for the transition to CNG to materialise. Hence, periodic monitoring of numbers could help us gauge the trend of switching from other fuels to gas.

1 Like