That is correct. They acquired 50% of MNGL for 190 crores pegging the total market cap of MNGL at 380 crores. MNGL generated a PAT of 74.68 crores in 2016, generating a cool ROI of 20% for IGL which is in line with the ROI for CGD’s in general.

After reading the post I was hooked as well. I mean we have a company that is nearly with 0 debts with ~1400 crore of reserves, natural monopoly through exclusivity and with government backing policies. However I see the following risks, nearly all of them are sectorial risks. I request views from other members on the following.

-

Domestically produced gas is currently priced based on the average of gas prices in gas-surplus countries like the US, Russia and Canada. With declining domestic production and a rapid rise in imports, the current price regime is not incentivizing enough for domestic capital expenditure as the cost of new deep-water discoveries ranges between 6–7 USD per MMBTU on account of higher costs and higher risks. Close to two dozen discoveries of ONGC, RIL and GSPC in the Krishna Godavari (KG) basin alone lie suspended for want of a feasible price. The current gas price in India, 3.83 USD per MMBTU, is much lower than that in some of the other countries: 9 USD per MMBTU in China, 10.5 USD per MMBTU in the Philippines, 6.5 USD per MMBTU in Indonesia and 8 USD per MMBTU in Thailand and Malaysia. So this is only a matter of time that the prices for NG will be revised to more balanced rate which will hike the prices of PNG.

-

As mentioned above the formula used to revise PNG prices is an weighted average of gas prices in countries like US, CAD, China. In the past two years NG prices continuously declined. Thus GoI reduced NG prices almost every six months. In the latest 4 revisal, the gas prices were continously reduced based on this indexed formula. But some reports (I do not know the truth of the report) like this one Why Natural Gas Prices Could Double From Here | OilPrice.com predicts that gas prices will go north from here. This will increase sourcing cost for CGD companies.

-

There is limited headroom between PNG and LPG cylinders typically in the range of 5 to 10% cheaper. This means if the sourcing cost for NG increases even by 5 – 10%, they will be at par with LPG cylinders which is not a big of an advantage. Seems like this has happened in the past. See here http://www.dnaindia.com/ahmedabad/report-png-price-rise-thousands-switch-back-to-lpg-in-ahmedabad-1870021 .

The following snippet explains this.

- I think PNGRB will eventually start regulating the prices of PNG as well to come up with a more transparent unified pricing approach to protect the consumers. It will not always be a free way for these companies that can just increase the price and never lower it when the NG prices are lowered which actually the last four times every six months so roughly for 2 years. The plight of a consumer is captured in this article The Pricing of Piped Gas Stinks in India . It is about IGL in Delhi and NCR region.

Although the profile seems good with almost 0 debt, free cash flows, natural monopoly, etc. as seen above the picture is not that rosy. Natural Gas sourcing cost for these companies might increase any moment (reviewed every six months by the government), how much of the increase these companies will be able to pass on to the consumer remains to be seen. There might be a point where in any higher increases in PNG might be non-justified for a domestic consumer since LPG cylinders might be comparatively cheaper and the conveniences offered by PNG will not justify the cost. But I do think the government will take measures to ease that a bit.

On the other hand, if government subsidizes PNG as it does for LPG cylinders and bare part of the import cost, and be able to keep off big companies like REL, ONGC for limiting sourcing cost, it is a screaming BUY.

But only time will tell this.

Inviting views from other members.

Disc: No holdings yet.

5 Likes

All valid points. However, here is an extract from the annual report of DHP India which manufactures LPG regulators, which would be a proxy for LPG usage. The part which says that the reduction in profit happened in part due to lower demand could be a result of customers moving away from LPG. My view is is that even if piped cooking gas were to cost more than LPG - a large swathe of NG customers wouldnt care because the time, effort and money involved in switching is just not worth it [ if it goes down would they switch back to CNG?]. Additonally, in any case, piped gas for domestic usage forms only 7% of the total gas consumption i.e. 93% of CNG is used for industrial use and automobiles where CNG is the undisputed heavyweight champ

5 Likes

Thanks @bheeshma for the quick reply. Could you point me to the source of “only 7% of PNG usage is domestic?”. Weather it is CNG or PNG, the source of funds will be impacted based on higher Gas prices and imports as I pointed. So I was under the impression that the prices of CNG will increase for the simple fact that the cost of source was higher. Correct me if I am wrong.

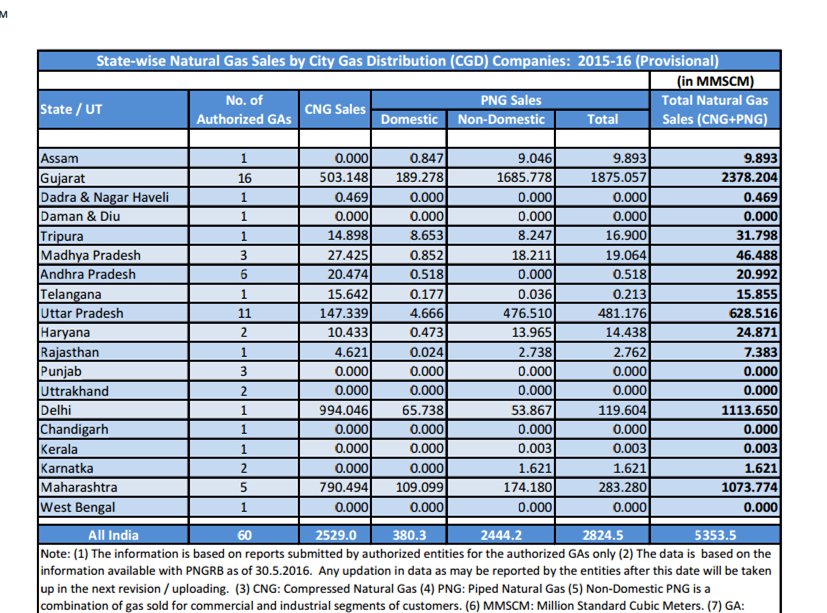

Out of the all india usage of 5353 MMSCM ( CNG + PNG ) in 2015-2016 , 380 MMSCM is attributable to domestic gas ( PNG Domestic ). I have pasted the image taken from the PNGRB website earlier on in this thread

{kind=link}

1 Like

Good to know. I missed it. But still industrial PNG, commercial PNG and even CNG prices are a function of NG price. So any hike in import costs or production costs will be cascaded to these as well. And NG prices will not always be lower as it is now due to reasons I documented in my post. It will invariably go up.

Even LPG prices are linked to natural gas/oil/petroleum prices. So if energy basket risks LPG price will too rise alongside PNG, I dont see demand destruction of PNG because it cannot be the case that only PNG price rises all other fuel too will see a rise along side PNG. and if diesel prices too continue too rise (like they have) switching to CNG will make all the more sense. My only fear: Is the NG underpriced in India as compared to other nation? will it be increased to achieved parity? Because this will mean PNG/CNG prices to rise unilaterally and so will so many other prices like power etc…

This is a super concall transcript. I would advise anyone with an interest in MGL to go through it. The questions are answered clearly and will address many of the doubts all of us have. One thing that caught my attention is they are soon going to launch two wheelers with CNG.

5 Likes

Thanks for sharing. Interesting insights, and what I like most is that the Management knows what they are up to

CNG Two wheelers launched in Mumbai

Why shouldn’t India, China, Philippines, Indonesia, Thailand and Malaysia import NG if price is 3.5 (currently) rather than going after high cost deep water discoveries ?

@csteja Why would they? NG prices are regulated by individual governments (although I hear it is going to change soon, not sure though) unlike oil prices which is a traded commodity at world market. So the prices like I said are set by Indian Government based on indexed average. It does not make sense for them to lower it and then import it. Although importing does happen as I understand from some reports. However that is only to fill in the required gap between production and consumption.

Thanks Ajith.

I wonder If avg of gas price in gas surplus countries like US, Russia is ~4 (indexed avg), then why would any country want to regulate NG price and make it 9USD (china for example). Is it to support the local industry ? Then currently are all domestic NG manufacturers able to make it below 4$ per MMBTU to be profitable ?

@csteja Precisely, because of this the NG manufacturers come under a lot of pressure. This is the very reason of my concern before the prices are set back to more realistic scenario. I extracted my original content for this specific point on Domestic Prices from this report by PwC. I recommend you to read this which has also some answers to your questions.

Disc: Have tracking position

Thanks for valuable discussion everyone, Seeing zero debt company, good ROI and monopoly in biz and plus a very good dividend paying company, I invested in @520 and continue to hold at least until 1050 when I will sell half of my holding to make it free ,have full faith in company growth for now

One need not worry about the monopoly status as any new player will have to pay the network tariff. Hence they will not be competitive. Also as MGL will be occupying most of the prime land, new player will find it difficult to build stations.

This is a structural story as in Mumbai UBER/ola still run on diesel unlike Delhi where in it is mandatory for cabs to ply on gas. So it is a trigger which is waiting to play our

1 Like

This is a good article which states that the share of natural gas in india’s fuel basket is b/w 6% - 7% while the global average is about 24%.

There is ample evidence of the govts push towards a natural gas economy and reports suggest that that share could be 15% going forward

I think its a great wave to catch early on

1 Like

Import duty on LNG halfed to 2.5 percent. This is expected to help CGD companies in terms of better sourcing cost.

http://m.economictimes.com/industry/energy/oil-gas/budget-2017-arun-jaitley-halves-import-duty-on-lng-to-2-5-per-cent/articleshow/56923207.cms

Some update, hope it will be useful : I stay in Vashi. MGL had started work on providing PNG in Vashi for some time but they stopped their further work for some reason. From our society we enquired with the Co few times, but never received any concrete answer. The update is that recently they started the work on full scale around my place and it seems they are now covering new areas in Vashi and shall provide connections in next 2-3 months. This will atleast give MGL some badly needed growth depending on scale of this activity. Anybody else on VP forum has some further update?

Interesting read… just one regulatory overhang remains - that of PNGRB - http://www.business-standard.com/content/b2b-chemicals/exclusivity-in-city-gas-distribution-network-to-affect-competition-117020800516_1.html?src=email