Since you highlighted SKR’s association with IIT … another fact is he is a close friend of AK as well and Subrato Saha (Independent director on Lycos board) is their common friend.

I am sorry to state these facts but Like AK has back fired on each and every promise, I am not surprised to see SKR following his close friend from IIT.

And please don’t think that all guys from IITs and IIMs are honest and value creators there are some toughs and value destroyers as well, apart from SKR you can count shantanu prakash of Educomp as well.

Exactly. The success (or failure) of Lycos Internet Ltd will not be tied to whether or not the promoter is an IIT or NIIT or IIM alum or how many grads from these institutes he employs. It will ultimately depend on the honesty and integrity of the promoter and his management and the quality of business decisions they take.

To me the entire upside (realistically) for this stock lies on the digital marketing side of their business. Everything else, is a shot in the dark (APLY, Lycos Life, Lycos Media). I have never counted the upside from any of these forays into my calculation. If even one of them turn out to be profitable and add meaningfully to the bottom line, then its a bonus.

If we just focus on Brightcom Media (their digital marketing division) for a moment and see if there is value, it might be a worthwhile exercise. Their website is (http://www.brightcom.com/blog/).

Its a very diff business, highly technical, with no comparable listed company in Indian markets. The industry is highly fragmented but a huge wallet size growing at the fastest pace within the Advertising space.

My concerns are not so much about the integrity of the promoters/management, but about their quality of decisions. For example, a lot of money has been invested in other fringe opportunities instead of focussing on their cash cow. Imagine the amount that has been spent to acquire what essentially is just the Lycos brand (everything else associated with Lycos website/search engine etc is worthless in today’s day and age). The Lycos brand is only being used today on Lycos Life products which I feel are not going to add anything meaningful to the bottom line. Their digital marketing business, which was earlier at least using the Lycos brand name is also renamed now as Brightcom.

Another point that needs to be investigated properly, is the capital intensity of the industry. On the surface, it looks like a high tech/software services industry, so one might end up thinking it could be a non linear model, which does not require regular capital infusion to grow. However, one interesting thing you will find if you look closely at their cash flow statement. They generate healthy Operating Cash flows (so, I tend to agree with the management when they claim that they are able to ultimately recover their dues from their debtors), but they regularly use all of this cash flow to invest back into the business (in the form of salaries, acquisitions etc. which ultimately are capitalized).

If this is the model of the business (requiring constant investment into development/upgrade) then how will they generate surplus for their shareholders? Will they need to gain a larger market share to be able to generate this surplus? If so, then is it the right strategy to go after multiple diverse forays?

Need to understand this in more detail. Then we can get more insights into the industry and business model.

Sorry to say brother, but if there is no integrity then one should not expect the quality (in business decisions). We as an investor can never get a sense where exactly all these capex investment are going on. May be it is pure fund diversion especially when 100% profit are made by overseas subsidiaries and capex too is in them only.

Just look at their S/w division, it is not making money (EBIDTA/EBIT/PBT/PAT whatever you consider) at all (even without negligible depreciation). Even LGS was not performing so badly.

Moreover, just look at there last 8 quarters concall transcripts and you will notice miscommunication from SKR be it related to messenger, crypto currency, ecommerce portal, lycos tv, lycos job, patents sale, lycos life (don’t forget launch of these products was not a soft launch but a full scale marketing and promotional event held in US as well as india) which failed badly but see SKR, he is still claiming that it was a soft launch to test market. He can’t make all the people fool all the time.

Finally, why can’t company pay mere Rs 5 cr (0.1 * approx 50 cr shares) as interim dividend instead of getting it approved in AGM in dec 2016 (hopefully another exception of extension would not be sought by too busy to work management) and then disbursing to investors in Jan 2016 (if approved).

Even if, all above reasons doesn’t stop an investor to resist greed to make money over here in LYCOS then amount allocated for LYCOS should be considered as a bet on a “call option” and not an investment in value pick.

Always remember, business may have up n down but intention of fraud and thughs can’t be changed it can only increase day by day.

Lycos Internet has not filed quarterly results with SEBI or NSE & BSE for Q1 & Q2 of FY 16-17.

It has not submitted Annual report of FY 15-16 till date with SEBI or RoC ( Registrar of Companies ).

It has changed its auditor in-between the year without taking proper consent of investors via Annual General Meeting (AGM).

It has postponed its AGM which was scheduled in Sep16 to date in next year ie, 2017. It also got approval for the same by RoC (Hyderabad).

Mr. M Suresh Kumar Reddy (Promoter) has pledged a significant amount of his shareholding in Q2 FY16-17 ie (Jul-Sep16) which means essentially he sold off his holding at avg. price of 8-10.

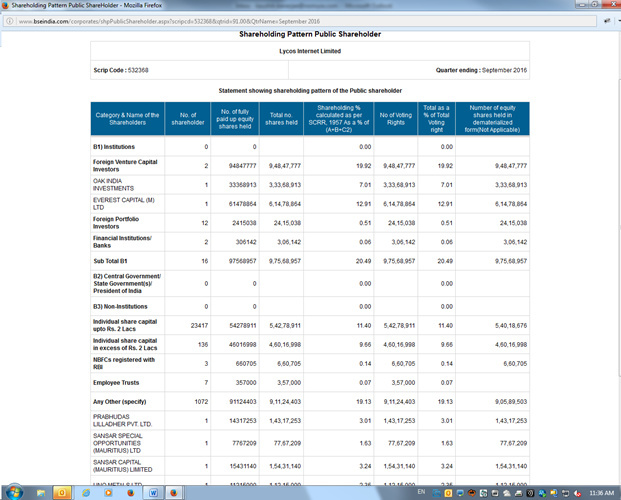

@amitanam all valid red flags, although not new information. However keep getting conflicting information on this company. For example, looks like Prabhudas Liladher has taken 3% stake in Lycos internet as per 30th Sep shareholding. Does this mean anything?

Prabhudas liladher has taken 3% stake shown in set. shareholding. Indeed it is great news. For first time indian broker has taken interest in lycos business. wait more will follow prabhudas liladher. By December almost all problems will be address by promoter.

All massive red flags enough to make any sane investor think 10 times before putting in their hard earned money here, but for some who are already invested, I can see why it is tough to see these red flags and act on them.

I am not sure you understand digital marketing. It is a simple trading business where the ad network like Brightcom buys ad inventory on its balance sheet from websites (publishers) and then sells them to brands who want to advertise there. It is capital intensive, dependent on balance sheet strength and minimum guarantees and has been among the most value destroying segments in tech investing over the last decade. It is easy to show growth here by giving minimum guarantees but no margins left to be made (20% gross margins typically). I dont think of this any differently than the listed rice traders or textile businesses

Even the much vaunted Inmobi committed to $200m from Softbank in 2011 and invested only $100m post which the company hasn’t been able to raise a single round of equity and is still massively loss making with no growth (they raised debt from some Chinese investor).

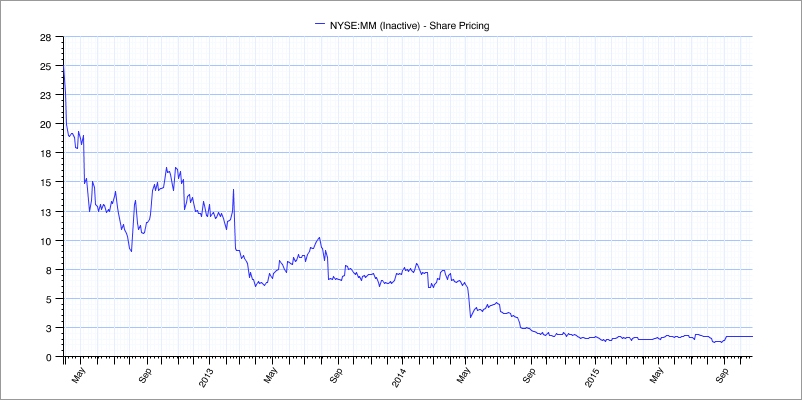

Millenial Media which was a darling of stock markets stock profile shown below. It eventually got acquired at less than 10% of IPO price. Bad business model + non trust worthy promoters make this an easy pass.

Niraj and Kaubaner-- looks good . Should get interesting from here especially if no more surprises in paying dividend , getting out annual report etc in December . And ofcourse settlement of daum issue .

@amitanam, please read company announcements carefully before making such statements sir! As it is this company has enough headwinds Just to clarify on your points :

Q1 standalone results are already out. Consolidated are not ready due to change from GAAP to Ind AS, will be available from Q2 as per company.

Auditor has not been changed, KPMG has only been appointed in an advisory role so far (I think engagement with Big4 to look at their books should be seen in a positive light!)

Pledging has gone up because share price has fallen which is expected - banks call for more shares when price falls, to keep the value of collateral same. Promoter has not sold any shares, SHP for Sep 30 is already out.

Well can some1 explain it to me except for brightcom what other part is generating impressions? We used to make 35 billion impressions per month. Now brightcom claims only 2 billion monthly impressions…where are the rest??? Aren’t they going to advertise it anymore???

Standard Indian retail investors mentality. Get bullish when the price is high or overvalued and write positive things about the company at overvalued prices. Get nervous and confused when you are getting the entire company for 1 years profits. Prabhudas Liladhar would have done some research before buying 1.43 crore share at a throw away price. There is value at the current prices, the value will increase if the price goes lower. If the company was not generating any cashflow at all then they wouldnt have reduced the debt from 150 crore to even 85 crore, there is some positive cashflow and they even invested some money in a new business which requires money the wearables business, which has a rating of almost 4 out of 5 in the reviews posted on Amazon india, the reviews are not bad in Amazon USA site either. Give the company some time, they are paying a small dividend expected in jan, after becoming debt free they will be able to pay a higher dividend and get rewarded with a higher stock price over time. The selling is over done at this price and this is the time to gradually start accumulating. Even if the company is only making 150 crore cashflow, the pe ratio is less than 3, the business is growing, the return on equity is reasonable. Overall it means this is the time to accumulate. Stock prices are rigged for long periods of time, you require patience to get returns gradually. At the current prices and lower, im a buyer and not a seller.

Just to clarify on your points :

Just to clarify on your points :